Do banks receive deposits and then loan some of that money out? Or do they first extend loans that turn into deposits in the banking system?

Some critics of Austrian economics and, most recently, of the Mises Institute’s new documentary, Playing with Fire, say that anyone who discusses the former is not up-to-date on modern banking practices.

Mike Shedlock at Mishtalk attempted to refute statements made by Joseph Salerno and me about fractional reserve banking in the documentary. Shedlock says:

Very Bad Start

At the 2:40 mark, Jonathan Newman, a Mises economist wrongly explains “Fractional reserve banking is the idea that banks keep a fraction of deposits in reserve so that somebody walks in and makes a deposit. What they [the banks] actually do is take that money and they use it to finance loans that they make to other people, business loans, mortgages.”

Continuing at the 2:58 mark, Joseph Salerno, Professor Emeritus at Pace University responds to Newman with “Let’s say they lend out 90 percent. They are comfortable keeping one dollar for every ten dollars that people will deposit. So you can write checks up to $1,000 on that checking deposit. At the same time there is 900 more dollars in circulation than there was before you made that deposit.

No Reserves on Deposits

The above paragraphs are shockingly bad, and outright false.

For starters, there are no reserve requirements on deposits. None.

…neither Salerno nor Newman understands how money is created.

Banks do not lend deposits. Rather, loans are the result of deposits. [I said banks never lent deposits. If you go back long enough they did.]

Those are his brackets, in which he was correcting something he wrote earlier. In 2020, he made this claim: “Deposits and reserves never played into lending decisions” (Shedlock’s italics). But in 2024 he accepts that once upon a time banks did lend from deposited money.

This is important because he pulled the quotes from the documentary out of context. As anyone can see, that section of the documentary is about what led to the creation of the Federal Reserve. We were describing what made the banking system unstable prior to the Fed. Regular bank crises, due to fractional reserves, created an incentive for banks to cartelize under a central bank, especially one with “lender of last resort” powers. So Shedlock and the documentary are in complete agreement regarding how banks used to operate.

Bank Reserves and Credit Expansion

But what about modern banking practices? Are Austrian economists clinging to an old-fashioned view of banking? In short, no.

Shedlock cites a BIS working paper from 2009 that disputes the idea that “an expansion of bank reserves endows banks with additional resources to extend loans.” He quotes the paper:

In fact, the level of reserves hardly figures in banks’ lending decisions. The amount of credit outstanding is determined by banks’ willingness to supply loans, based on perceived risk-return trade-offs, and by the demand for those loans.

The main exogenous constraint on the expansion of credit is minimum capital requirements.

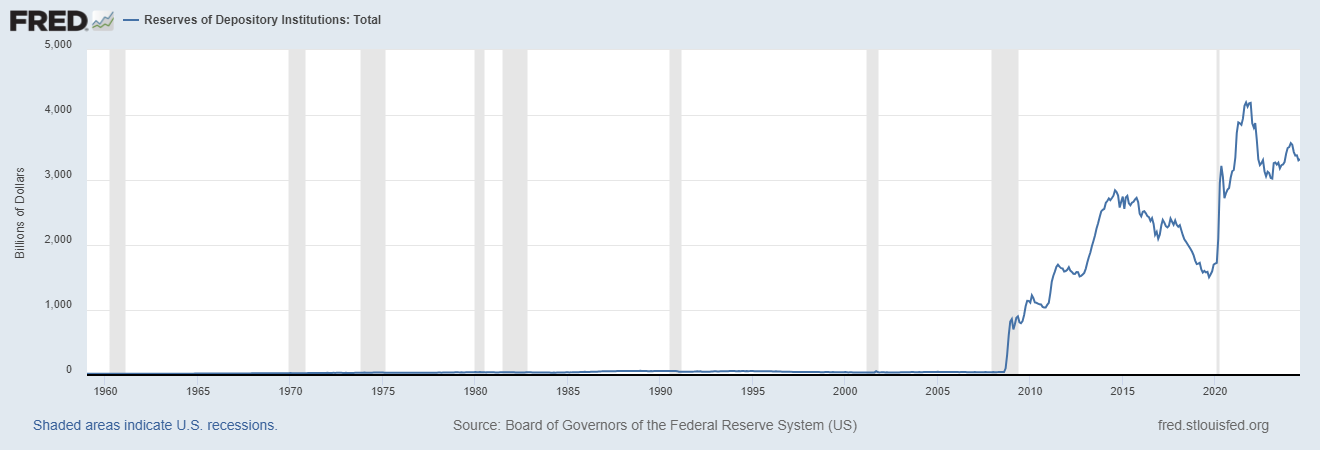

Indeed, if you look at bank reserves over time, you’ll notice that there was a dramatic change in 2008.

Source: Board of Governors of the Federal Reserve System (US), Reserves of Depository Institutions: Total [TOTRESNS], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/TOTRESNS, October 17, 2024.

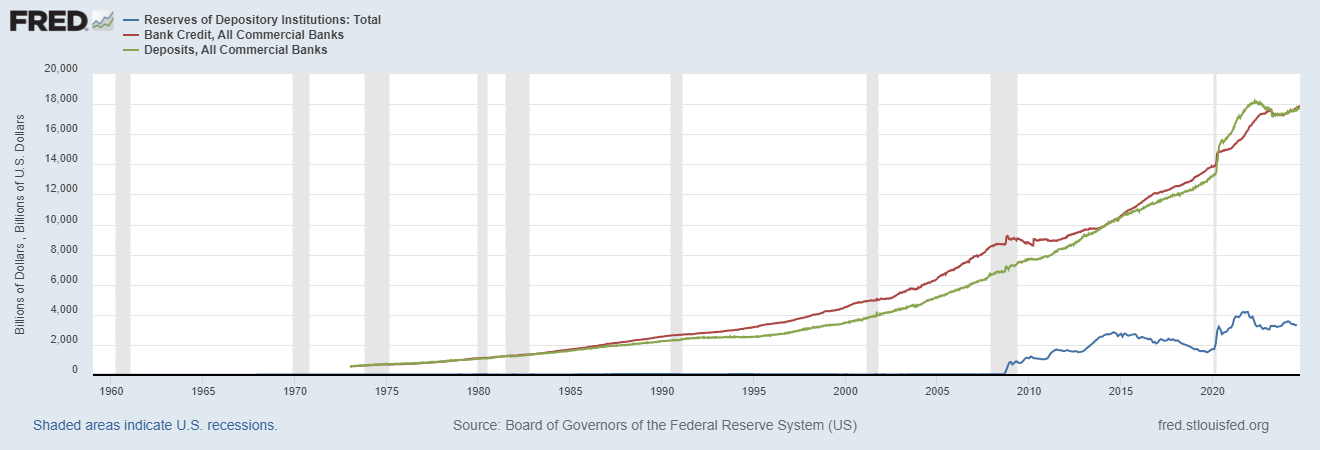

When you add bank credit and deposits, you’ll notice that even though reserves exploded, there was no explosion in bank credit or deposits, at least not in the way the classic money multiplier would suggest.

Source: Board of Governors of the Federal Reserve System (US). Deposits, All Commercial Banks [DPSACBW027SBOG]; Bank Credit, All Commercial Banks [TOTBKCR]; Reserves of Depository Institutions: Total [TOTRESNS]. Retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/graph/?g=1wdsv. October 17, 2024.

Why? In October of 2008, the Fed began paying interest on reserves (IOR) to regain tight control over the Federal Funds Rate amid heightened uncertainty and massive increases in the demand for reserves. IOR provides the added benefit to the Fed by providing a gate between bank reserves and bank credit such that a large increase in bank reserves would not necessarily result in banks expanding credit. Banks obviously took advantage of this opportunity, to the point that minimum reserve requirements, which had become nonbinding, were eliminated in 2020.

In short, the Fed has immobilized bank reserves to a large extent by paying (bribing?) banks to sit on the money.

So, Shedlock was correct when he said that US banks no longer have reserve requirements, but that is because the Fed has replaced the stick with a carrot. The Fed has “reserve incentives” now, instead of reserve requirements.

You’ll notice that in the quotes Shedlock pulled from the documentary, neither one of us said anything about reserve requirements. We were simply describing the fact that there is a mismatch between reserves and deposits with fractional reserve banking. This is true no matter what the order of operations is (deposit-loan or loan-deposit) and no matter how banks are required or incentivized to keep some reserves.

Have Austrians Ignored the Exogenous vs. Endogenous Money Debate?

Finally, I want to show that Austrian economists do not have their heads in the sand, as Shedlock suggests. There are many articles, videos, and books about the Fed’s new “policy tools,” unprecedented monetary policy since the Great Financial Crisis, and the implications for price inflation, business cycles, financial stability, and bank soundness.

For example, Arkadiusz Sieroń and I summarized the debate over endogenous money (of which Shedlock is convinced) and its implications for Austrian business cycle theory (ABCT) in our chapter in A Modern Guide to Austrian Economics, edited by Per Bylund. Here is the relevant passage (I’ve replaced the in-text citations with links):

The opposing view [endogenous money] is that the causation is the other way around: commercial banks extend loans based on expected profitability, these loans become deposits in the banking system, and finally the level of deposits determines the banks’ demand for reserves which are supplied by the central bank (“in normal times, supplied on demand”) ([Bank of England report,] p. 15). The two sides are ultimately debating whether money is exogenous (the central bank has ultimate control over the money supply) or endogenous (the central bank passively responds to banks’ demand for reserves). […]

If the endogenous money view is true, one potential implication for ABCT is that the central bank cannot be blamed (at least not directly) for artificial credit expansion and that monetary policy in general has a more uncertain effect on credit expansion and starting business cycles. However, even in Mises’s original exposition of ABCT, he identifies “credit-issuing banks” (p. 357) and their issuance of fiduciary media as the cause of a new discrepancy between the Wicksellian natural rate of interest and loan rates such that production is unsustainably lengthened beyond what the subsistence fund would allow. This mechanism of credit expansion (new issues of fiduciary media) operates in both the exogenous and endogenous money scenarios. Murphy also shows that Mises and Hayek pointed to fractional reserve banking per se as the primary cause of cycles. While Rothbard claims that inflations “may be effected either by the government or by private individuals and firms in their role as ‘banks’ or money-warehouses” (p. 990), in his main discussion of business cycles, unsustainable booms begin with commercial banks expanding credit (p. 995). Only later does Rothbard explain how a central bank can willfully expand reserves upon which commercial banks may extend new credit. In America’s Great Depression, Rothbard also begins his theoretical overview of ABCT with “what happens when banks print new money (whether as bank notes or bank deposits) and lend it to business” (p. 10), not with the actions of a central bank. Therefore, it cannot be said that Austrian economists have built and developed their business cycle theory upon a particular view of the money creation process and that ABCT only applies to environments in which money is exogenous. Whether money is endogenous, exogenous, or both has no bearing on ABCT per se, only in the historical analysis of cycles and how they were started.

So, it doesn’t matter if money is endogenous. Shedlock’s critique merely asserts that money is endogenous and that this is somehow a fatal blow to Austrians and their views on banking, inflation, and business cycles. But it’s not. If money is primarily generated within the banking system, it still results in unsound banks, price inflation, and business cycles. If the supply of money is primarily determined by central bank policy, the same applies. In the real world, both private banks and the central bank exert influence over the total stock of money and interest rates, though I would add that the banking system’s ability to engage in fractional reserve banking and expand credit is enabled by the central bank and the government. A free banking system would be constrained in its ability to expand credit due to bank competition.

Funnily enough, in the next paragraph, we actually cite and discuss the same BIS paper that Shedlock quoted. Shedlock may think that Austrian economists are stuck in the past, but it seems he is the one who needs to brush up on our literature, not the other way around.

Interested readers should also check out Bob Murphy’s excellent book Understanding Money Mechanics. He has a whole chapter dedicated to the endogenous money debate, in which he shows that much of the debate is over semantics and that sometimes the perspective of an individual bank is conflated with the perspective of the banking system as a whole.

Remote video URL

Tags: Featured,newsletter