The engineer and the gambler both face uncertainty, but only one can control the forces involved. Jonathan Newman explores the gap between plan and outcome that drives all economic life.

Read More »2026-05-11

2026-05-11

The engineer and the gambler both face uncertainty, but only one can control the forces involved. Jonathan Newman explores the gap between plan and outcome that drives all economic life.

Read More »2026-04-23

Our own Jonathan Newman had the opportunity to sit down with a Federal Reserve governor. The central banker’s answers to Newman’s questions were evasive and riddled with contradictions. It seems there is not much behind the Fed’s technocratic veneer.

Read More »

Our own Jonathan Newman had the opportunity to sit down with a Federal Reserve governor. The central banker’s answers to Newman’s questions were evasive and riddled with contradictions. It seems there is not much behind the Fed’s technocratic veneer.

Read More »2026-04-17

On VRIC Media, Darrell Thomas talks with Jonathan Newman about the real problem behind debt and deficits.

Read More »2026-04-15

While Tax Freedom Day is mid-April, Rothbard’s measure of the government’s fiscal burden reveals that Americans don’t truly start working for themselves until June 5, over seven weeks later.

Read More »

While Tax Freedom Day is mid-April, Rothbard’s measure of the government’s fiscal burden reveals that Americans don’t truly start working for themselves until June 5, over seven weeks later.

Read More »2026-04-06

On the Investment News Network with Charlotte McLeod, Dr. Jonathan Newman presents a primer on Austrian economics.

Read More »2026-03-27

Drawing on Man, Economy, and State, Dr. Jonathan Newman walks through Rothbard’s theory of price formation and competition, showing that prices reflect subjective preferences, not seller greed, and that the only consumer-harming monopolies are those created by the state.

Read More »2026-03-18

Generations of scholars come and go; a few, including Roger Garrison, make their mark on the field and inspire future generations to do the same.

Read More »

Generations of scholars come and go; a few, including Roger Garrison, make their mark on the field and inspire future generations to do the same.

Read More »2026-03-10

Forcing AI companies to provide their own power doesn’t get at the root of the issue, which is that the resources we use to generate electricity are scarce.

Read More »2026-02-24

Jonathan Newman tackles the new “Federal Reserve Simulator” game in which players try to match wits against the Fed. As Newman found out, however, the same outcomes occur no matter what information one feeds the simulator. In short, it’s rigged.

Read More »2026-02-10

2026-01-15

The Fed’s cost overruns in its building renovation project supposedly are not borne by taxpayers because, as the myth goes, the Fed is “self-financing.” However, the Fed’s “earnings” come from interest payments from the government, payments made by…taxpayers.

Read More »2025-12-16

Dr. Jonathan Newman joins Cheryl Daley on The Homeschool How To Podcast.

Read More »2025-12-12

2025-11-21

Equilibrium is an imaginary construct that should be used only for analytical purposes. Unfortunately, mainstream economists have claimed it should represent a desired state of economic affairs. Austrian Economists know better.

Read More »2025-11-12

Dr. Jonathan Newman explains why we don’t need a central bank, and lays out a concrete, Rothbard-inspired plan for actually ending the Fed.

Read More »2025-09-23

Mainstream economists have justified the creation of the Federal Reserve because they claim that a growing economy—especially the banking system—needs an “elastic” currency. In other words, the economy “needs” at least some inflation. Austrian economists know better.

Read More »2025-08-21

The Fed by design feeds the political machine in DC by concealing the costs of government spending. The Fed serves the government, not the American people.

Read More »2025-08-14

Werner’s experiment is dubious at best. He strawmaned the alternative theories and set up the experiment in such a way that only his preferred theory would be confirmed.

Read More »2025-07-31

Not only are modern monetary theory (MMT) cultists dishonest about the role of money, they also are dishonest about money‘s history. By taking issue with Carl Menger‘s historical version, they expose their own ignorance of how money came about.

Read More »2025-07-25

If education and career skills are what you want, a college or university may be a waste of your time and money.

Read More »

If New Yorkers wanted to help students by paying for their tuition, they would have already done so on their own.

Read More »2025-07-14

Reich, Elizabeth Warren, and other leftists never address the root cause of what they correctly diagnose as excessive corporate power: the Federal Reserve.

Read More »2025-06-23

Ted Cruz’s politics aren’t just conservative, they’re theological. Jonathan Newman explores how dispensationalism shapes US loyalty to the state of Israel.

Read More »2025-06-20

Ted Cruz’s politics aren’t just conservative, they’re theological. Jonathan Newman explores how dispensationalism shapes US loyalty to the state of Israel.

Read More »2025-05-29

Rumor has it that the Federal Reserve was able to resist the president‘s demands to enable funding of the Korean War. However, a look at the record demonstrates conclusively that the Fed bowed to Harry Truman‘s wishes to do what it has done for a century: finance America‘s wars.

Read More »2025-05-28

Rumor has it that the Federal Reserve was able to resist the president‘s demands to enable funding of the Korean War. However, a look at the record demonstrates conclusively that the Fed bowed to Harry Truman‘s wishes to do what it has done for a century: finance America‘s wars.

Read More »2025-05-17

Is the Federal Reserve truly independent? Jonathan Newman uncovers the myths behind the 1951 Treasury-Fed Accord.

Read More »2025-05-07

Not only are Modern Monetary Theory (MMT) cultists dishonest about the role of money, they also are dishonest about money‘s history. By taking issue with Carl Menger‘s historical version, they expose their own ignorance of how money came about.

Read More »2025-02-26

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-11-04

As of this morning, ABC’s Project FiveThirtyEight says that Donald Trump wins 53 times out of 100 and Kamala Harris wins 47 times out of 100. How can we make sense of this statement?To do so, we have to understand the difference between case probability and class probability.Presidential elections are unique events that are determined by the actions of humans, and so belong to the case probability category. The nature of such events is that numerical probabilities cannot be assigned in a scientific way to the possible outcomes. All we can do is guess, based on our own judgment of the circumstances and how we think the people who participate in determining the outcome will act. But this guess is a qualitative judgment and can only be articulated with numbers by recourse to metaphorical

Read More »2024-10-30

What is the Mises Institute? The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order.

Read More »2024-10-25

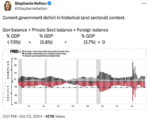

Modern Monetary Theory (MMT) posits that booms and busts can be explained by private versus public sectoral balances and the inherent instability of private financial markets. Stephanie Kelton frequently points to this graph of public and private surpluses and deficits:The red bars show the government’s budget as a percent of GDP. When the government spends more than it collects in taxes, it runs a deficit and sells debt. The government’s debt is sold domestically and to foreign buyers. These groups become net lenders to the government to the extent they purchase government debt, and this is shown with the black and gray bars.When the government (rarely) runs a surplus, it means that the government is collecting more in taxes than it is spending, and so the non-government sectors must

Read More »2024-10-23

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »

On October 17, 2024, Jonathan Newman appeared on Wake-Up Call with Bill Lundun to discuss Austrian economics, Donald Trump, and mainstream economists.The original episode is available at News Radio 1120 KPNW.Bill Lundun (BL): News Radio 1120 KPNW, thanks for being with us this morning. We have like two different things that we keep hearing when it comes to this particular election period. And it is that Americans overall trust Trump more on the economy. And that’s we’re talking about voters, whereas the so-called experts don’t. Who to believe to discuss it this morning? It is Dr. Jonathan Newman. He is a fellow at the Mises Institute, which is a nonprofit that promotes the teaching and research in the Austrian School of Economics. And it’s in the tradition of Ludwig von Mises and Murray

Read More »2024-10-22

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-10-18

Do banks receive deposits and then loan some of that money out? Or do they first extend loans that turn into deposits in the banking system?Some critics of Austrian economics and, most recently, of the Mises Institute’s new documentary, Playing with Fire, say that anyone who discusses the former is not up-to-date on modern banking practices.Mike Shedlock at Mishtalk attempted to refute statements made by Joseph Salerno and me about fractional reserve banking in the documentary. Shedlock says:Very Bad StartAt the 2:40 mark, Jonathan Newman, a Mises economist wrongly explains “Fractional reserve banking is the idea that banks keep a fraction of deposits in reserve so that somebody walks in and makes a deposit. What they [the banks] actually do is take that money and they use it to finance

Read More »2024-10-16

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-10-02

In the final stretch of any presidential campaign, the goal is to attract any remaining undecided voters. This usually means that candidates moderate and soften their messaging, especially in comparison to the proposals and rhetoric used to attain the nomination of their respective parties earlier in the campaign. This was on full display in last night’s vice-presidential debate between J.D. Vance and Tim Walz.I also want to discuss a few important things that weren’t said on the debate stage last night, like whether the government should be involved at all in the areas discussed, the true cause of price inflation, the war in Ukraine, and the momentous political realignment signified by Dick Cheney and other neocons endorsing the Harris-Walz ticket.Bipartisanship and “we gotta do

Read More »2024-09-20

Paul Krugman’s latest column is all over the place. He was trying to provide commentary on the Fed’s half-point cut in the Federal Funds Rate, but he was juggling too many contradictory narratives.The contradictions start at the beginning. The Fed’s decision “was of minimal importance” but also a “momentous move.” It wasn’t important because it just a small change in the overnight interbank interest rate. It was very important because of its effect on other interest rates and because the Fed has “declared its belief that the war on inflation has been won.” Maybe Krugman was going for the antithesis literary device, like Neil Armstrong’s “small step for man, giant leap for mankind.” Maybe he wanted to downplay any immediate suspicions that such a large cut a few weeks before the

Read More »2024-09-09

The Mises Institute is taking back economics education. In public schools, students learn that FDR’s New Deal and World War II got the US out of the Great Depression. They learn that total government control over an economy has its downsides, but so does pure laissez-faire, so the best system is a mixed economy with government intervention. The role of the entrepreneur is minimized or even completely ignored while the role of the state is emphasized and praised.Public education indoctrinates students so that they become unquestioning citizens who will embrace price controls, taxes, inflation, and regulations.To fight back, we’re producing a series of short lectures corresponding to Robert P. Murphy’s excellent textbook, Lessons for the Young Economist. The text is already widely used in

Read More »2024-09-04

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »

“It says here in this history book that, luckily, the good guys have won every single time. What are the odds?” – ~Norm MacDonaldA segment of Tucker Carlson’s recent interview with Darryl Cooper is making the rounds on social media. Cooper questioned Winston Churchill’s hero status, which is a big no-no, especially among conservatives. The accepted view is that World War II can be reduced to the good guys versus the bad guys and that Churchill is the one who bravely convinced the good guys to go to war against the bad guys.Cooper suggests that Churchill’s legacy is more complicated. According to Cooper, Churchill “kept this war going, and he had no way to go back and fight this war. All he had were bombers. He was literally, by 1940, sending firebombing fleets to go firebomb the Black

Read More »2024-08-26

You would think that the growing popularity of homeschooling in the United States would be in more news headlines. Estimates from the National Home Education Research Institute (NHERI) reveal a staggering increase in the number of homeschool students since the 1970s—by a factor of 238. Of course, there was a surge in homeschooling during the Covid lockdowns, when many public schools either went completely virtual or implemented harsh measures that severely limited both learning and student satisfaction. But the NHERI data shows that there was already a long, pre-Covid trend of growth in homeschooling, from 13,000 students in 1973 to 2.5 million in 2019. The homeschool population exploded above the trend to 3.7 million in 2021, but in 2022 it fell to 3.1 million, which is above the trend as

Read More »2024-08-23

In 301 AD, Roman emperor Diocletian implemented price ceilings on over 1,200 goods. The silver coinage had been debased over the past 250 years, and the citizens were understandably unhappy about high prices. In 50 AD, each denarius had about 3.9 grams of silver, but then the empire debased the coins, sometimes in dramatic steps and sometimes more slowly. By 125 AD, the coins had less than 3 grams of silver. By 200 AD, it was less than 2 grams. There was another precipitous drop in silver content between 250 and 275 AD, and in short order there was only a “neglible coating of silver” on each coin.Image source: Visual Capitalist.The English translation of Diocletian’s edict is fun to read. It shows that not much has changed in politics over the millennia. Diocletian is introduced as

Read More »2024-08-20

In Paul Krugman’s latest column, he claims that Kamala Harris hasn’t advocated for price controls, only a ban on price gouging on groceries. Of course, these are the same thing. Krugman’s own principles text defines price controls as “legal restrictions on how high or low a market price may go.” A ban on price gouging is a legal restriction on how high a market price may go. Therefore, even Krugman-the-textbook-author admits that a ban on price gouging is the same as a price ceiling.In his column, he gives examples of price gouging: “Texas prohibits many businesses from ‘demanding an exorbitant or excessive price’ on things including food and fuel during disasters,” “voters hate it when businesses take advantage of shortages to charge very high prices,” and “some of us still remember the

Read More »2024-08-12

The Libertarian Party candidate for governor of North Carolina posed this question on Twitter a few days ago:The question is poorly worded, but that is mainly the fault of the way the term “inflation” has fared in common parlance. Ross probably got the poll results he desired – he was trying to reinforce the idea that increasing the supply of money results in higher prices. The issue, however, is that those who understand that relationship are also usually the ones who think inflation ought to refer to increases in the money supply. For them, the question reads, “Does increasing the money supply create increases in the money supply?” The answer to the question now depends on how one interprets “create” instead of one’s understanding of economic cause-and-effect. Indeed, many of the

Read More »2024-08-07

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-07-30

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-07-26

Mandate for Leadership 2025 is an unofficial blueprint for a potential conservative administration, published by the Heritage Foundation’s Project 2025. Donald Trump has distanced himself from the project, even though many people associated with his first term as president contributed to the document.It’s billed as “The comprehensive policy guide for a new conservative president, offering specific reforms and proposals for Cabinet departments and federal agencies, pulled from the expertise of the entire conservative movement.” Paul Dans, the Project 2025 Director, says that the project aims “to deconstruct the Administrative State.”Chapter 24 of the 922-page document is on the Federal Reserve. It was authored by Paul Winfree, Distinguished Fellow in Economic Policy and Public Leadership at

Read More »2024-07-10

One of the silver linings of the covid regime is the fact that the state overplayed its hand and turned many people into skeptics of the State and its pawns in the media and academia. This wave of healthy skepticism has led to a surge of interest in the work of Murray Rothbard, the State’s greatest enemy.Dr. Robert Malone, whose Wikipedia entry tells you everything you need to know about what the establishment thinks of him, followed this path. He recently wrote on his discovery of Rothbard through What Has Government Done To Our Money? and Anatomy of the State. Here are a couple snippets — you can read it in full here.—–…I read and attempt to comprehend comments and essays from important economists, but it all sounds like insider babble to me—Keynesian stimulation, supply-side Laffer

Read More »2024-07-01

Robert Reich is on his fifth myth, but so far, he has just been recycling the same progressive talking points in each one. The overall message is that big corporations and the super wealthy wield too much political power and that they shape the law in their own favor, contributing to terrible economic inequality. For Reich, the U.S. economy is a zero-sum game and the people at the top have rigged it so they win and everybody else loses.His solution is strong labor unions, high taxes on the rich, a high minimum wage, more trust-busting, and government wealth redistribution. He sees the economy through the lens of political power, and so the only solutions he can think of are ones that exploit the power of government to channel more of the fixed pie of wealth to a different group of people.

Read More »2024-06-26

Alexander Salter argues that “there’s no good reason to raise the inflation target,” and while he makes some valid points, his analysis goes awry because it is based on the faulty quantity theory of money. He says that the proponents of a higher inflation target erroneously believe that it would “give the Fed more wiggle room to ease policy, should recessionary pressures emerge.” Salter says that the Fed can still stimulate nominal spending even when interest rates hit the zero lower bound, a boundary that the Fed is more likely to bump into with a lower inflation target.Salter correctly notes that inflation hinders economic growth, which means that, from the Fed’s perspective, there are tradeoffs in their monetary policy choices, including their choice in an inflation target. A higher

Read More »2024-06-18

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-06-07

Robert Reich’s second myth is “Government Obstructs the Free Market.” (See my response to his first myth here.) He says that what we call the “free market” can only exist with a government enforcing rules about property, monopoly, contracts, and bankruptcy.

Read More »2024-06-04

“Additional units of a homogeneous good must go toward less important ends.” Is this an ethical claim? Does it fall under political science? Or is it an economic law?According to Robert Reich, economics, properly considered, is in a mush with politics and morality. He has started a new ten-week series debunking economic myths, and the first one is “Economics is Objective.” I wouldn’t say he is off to a good start.Reich asserts that economics ought to be all about one question: “What sort of society do we want?” He says that economics used to be called “political economy” back in the nineteenth century and that Adam Smith referred to himself as a moral philosopher. These two tidbits are the only substance of his video, which is less than three minutes long.He lists some silly questions like

Read More »2024-06-03

Tucker Carlson is apparently warming up to Austrian economics and the work of the Mises Institute. In 2019, when he was still on Fox News, he made a quick dig at Austrian economics, and he was critical of “libertarian economics” as recently as December of last year.But Austrian economics and the Mises Institute have come up in his interviews with three different guests over the past few months, and instead of being critical or dismissive, Carlson was open to the ideas.He posts some of his interviews on Twitter, where the view counts are in the millions. Austrian economics came up in these episodes:March 19 – Ron Paul – 3.9 million views (15-minute clip – full interview behind paywall)May 16 – Dave Smith – 4.8 million viewsMay 21 – Erik Prince – 4.2 million views(For comparison, as of April

Read More »2024-05-18

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-05-03

“Why do we borrow our own currency in the first place?”Stephanie Kelton posed this question in her new documentary, Finding the Money, and a clip of Jared Berstein’s fumbled response to the question has gone viral on social media. Bernstein is the Chair of the Council of Economic Advisers to Biden, and so we would expect that he would have an articulate answer to Kelton’s question, but he did not.Instead of trying to parse his response or explain why he fumbled, I want to provide an answer: the State borrows to expropriate real resources from the private, productive part of society. When I made this claim on Twitter, one MMTer responded (somewhat) approvingly: “We all agree on this part. The question is how they do it and what the effect is. MMT gets that part right [and] Austrians get it

Read More »2024-04-24

Jordan Klepper: You need to– you know what you need to do? You need to take some– some THC or some DMT and let the MMT just wash over you. Let the paradigm shift come to you, Ronny Chieng.Ronny Chieng : Yeah, I think I’m in it right now.Klepper: I think you’re in it.Stephanie Kelton appeared on The Daily Show to promote her documentary, “Finding the Money,” which is set to be released on May 3. The documentary promises to take viewers on a “journey through Modern Money Theory or ‘MMT’, to unveil a deeper story about money, injecting new hope and empowering democracies around the world to tackle the biggest challenges of the 21st century: from climate change to inequality.”Two comedians, Jordan Klepper and Ronny Chieng, interviewed Kelton about money and government finance, but the most

Read More »2024-04-17

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »

Ludwig von Mises’s Economic Policy: Thoughts for Today and Tomorrow has become quite popular recently. The Mises Book Store has sold out of its physical copies, and the PDF, which is available online for free, has seen over 50,000 downloads in the past few days.This surge in interest in Mises’s ideas was started by UFC fighter Renato Moicano, who declared in a short post-fight victory speech, “I love America, I love the Constitution…I want to carry…guns. I love private property. Let me tell you something. If you care about your…country, read Ludwig von Mises and the six lessons of the Austrian economic school.”The “six lessons” he is referring to is Mises’s book, Economic Policy: Thoughts for Today and Tomorrow, which was republished by our friends in Brazil under the title “As Seis

Read More »2024-03-07

When Nvidia reported high fourth quarter earnings for 2023 in February 2024, it sparked a general rally in stock markets. Stock markets in the United States, Japan, and Europe jumped to all-time highs after a few days of slight declines.

Read More »2024-02-29

The Bureau of Economic Analysis released January figures for Personal Consumption Expenditures (PCE) today, including the price index based on that data.News headlines report the year-over-year percent change in the PCE price index: 2.4%.

Read More »2024-02-12

Silvergate Bank, Silicon Valley Bank, Signature Bank, and First Republic Bank fell like dominos in March–April 2023. The United States Treasury, Federal Reserve, and Federal Deposit Insurance Corporation (FDIC) intervened in an unprecedented way to stall the domino effect. They waived the FDIC’s $250,000 cap on insured deposits at the failed banks, and the Fed instituted the Bank Term Funding Program to bail out any and all banks that run into trouble meeting depositors’ redemption demands.

The interventions saved the banking system, for a while. However, the inherent problem is rearing its ugly head once again.

When Signature Bank was liquidated and put into FDIC receivership, New York Community Bank bought $38.4 billion worth of Signature’s assets. Less than a year later, Moody’s

2024-02-06

One doesn’t need to search modern economic literature to take on the MMT crowd. Just read Bastiat.

Original Article: Bastiat versus MMT

2024-02-01

Murray Rothbard called Richard Cantillon the “father of modern economics.” While that title is often given to Adam Smith, Rothbard suggested that all the good things in Smith were first discovered by Cantillon or other pre-Smithian economists and that virtually all of Smith’s original ideas were “a significant deterioration of economic thought.”

One of Cantillon’s greatest insights involved the uneven effects of monetary expansion. New money enters the economy at a particular point—the first spender of new money acquires goods from the market, and those sellers may now use the money to increase their demands for goods, and so on. The money ripples out from its origin, providing real benefits to those closest to the center. As the new money is spent, prices rise, meaning those whose incomes

2024-01-20

Proponents of modern monetary theory (MMT) are back in action after a quiet spell during the embarrassing (for them) record price inflation of 2021–23. They are here to tell us that the mountain of government spending and debt is nothing to worry about; the government’s red ink is the private sector’s black ink, they say. Private sector growth emanates from public sector deficits, and since the US government has a gigantic money printer, there’s no reason to ever fear a default or debt crisis.

Frédéric Bastiat, the great proto-Austrian French economist, provided an excellent framework for us to evaluate this claim about the consequences of government spending.

In the department of economy, an act, a habit, an institution, a law, gives birth not only to an effect, but to a series of

2024-01-04

Price inflation statistics were a hot topic in 2023. Official measures, like the Personal Consumption Expenditures Price Index (PCE) and the Consumer Price Index (CPI), rose to levels not seen in over four decades.

These measures were under commentators’ microscopes as recently as last week. The FRED Blog (run by the St. Louis Fed) briefly discussed how these two measures are constructed and how they differ. Paul Krugman compared the change in the “core” versions of the PCE and CPI (which remove components like food and energy) over six- and twelve-month time intervals, respectively. The consensus view is that these measures have unique applications. According to Krugman, “which one you should choose depends on what question you’re trying to answer.”

But if you read Mises, you’ll see a

2023-12-14

With US government debt skyrocketing past $33 trillion and possible recession looming, the Treasury faces the prospect of running out of suckers. Finding buyers for US debt will become much more difficult.

Original Article: As the US Treasury Runs Out of Creditors, Its Options Dwindle

2023-12-04

Paul Krugman can’t figure out why everybody is so bummed about the economy. From his perspective, we should all be jumping for joy, praising Joe Biden, and publicly signing fifty-year commitments to vote Democrat. Official statistics show that “unemployment is still near a 50-year low, yet inflation has been falling fast.” But the ignorant masses simply won’t get with the picture. Krugman admits “surveys of consumer sentiment and political polls continue to show that Americans have a very negative view of the Biden economy.”

He concludes that it is partisanship and media bias driving a wedge between consumer sentiment and economic reality. He found a study that shows that 30 percent of the disparity can be explained by Republicans who are doing fine economically but are just mad that Biden

2023-11-29

Are the chickens coming home to roost for the US Treasury? As Ryan McMaken noted in a recent Mises Wire article, the United States is in a debt spiral and there’s no easy way out.

The problem is multifaceted, but the origin is profligate government spending. While it typically spikes during crises, spending is increasing at an alarming rate even outside of crisis periods. And tax revenues are not keeping up, which means ever-deepening deficits. Government expenditures spiked during the 2020 crisis, but even ignoring those spikes, annual spending has increased by about $1.6 trillion since 2019, while tax receipts have only increased by about $600 billion.

The government must borrow to make up the difference, which has led to a mountain of debt. Total public debt has ballooned to over $32

2023-11-14

As war rages in the Middle East, we are reminded of what Mises wrote in 1949 on warfare and its awful effects.

Original Article: Mises on the History of Warfare

2023-11-08

Recorded at the Mises Circle in Fort Myers, Florida, 4 November 2023. Includes audience question and answer period.

Special thanks to Murray and Florence M. Sabrin for making this event possible.

The Radical Uncertainty of a Polymorphic Fed | Jonathan Newman

Video of The Radical Uncertainty of a Polymorphic Fed | Jonathan Newman

Read More »2023-10-27

“The market economy involves peaceful cooperation. It bursts asunder when the citizens turn into warriors and, instead of exchanging commodities and services, fight one another.”

So Ludwig von Mises begins a short chapter in Human Action called “The Economics of War.”

While brief, the eleven pages (pages 817–28 in the scholar’s edition) are densely packed with Mises’s take on the history of warfare, what leads to total war, how wars are won, the costs of war, and the ideological conditions for war and peace. As is his modus operandi, Mises frequently contrasts war with the peaceful cooperation of the international division of labor.

The History of Warfare

In his short history of warfare, Mises describes the wars of primitive times as total wars, in which both sides sought the complete

2023-10-22

Forget Vegas sports betting for reckless speculation. When the Fed officials make projections, the markets assume they are accurate. However, as Jerome Powell himself admits, forecasts are speculative at best.

Original Article: Fed Forecasts: Financial Sport or Costly Distraction?

2023-10-19

Recorded at the Mises Institute Supporters Summit in Auburn, Alabama, 12-14 October 2023. Sponsored by Dan Johnson and Randee Laskewitz.

Central Bank Digital Currencies: The Last Battle in the War on Cash | Jonathan Newman

Video of Central Bank Digital Currencies: The Last Battle in the War on Cash | Jonathan Newman

Read More »2023-09-30

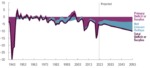

When Silicon Valley Bank and other banks failed earlier this year, the debate over the sustainability of fractional reserve banking resurfaced. Under fractional reserve banking, banks keep only a fraction of customers’ deposits in reserve. The difference is bank credit, such as government debt, mortgages, business loans, and many other kinds of loans. This practice leaves the bank open to a run, in which panicky depositors attempt to withdraw their funds from the bank en masse but the bank doesn’t have the cash on hand. The following FRED graph gives an idea of the extent of the mismatch between deposits and reserves.

[embedded content]

But we shouldn’t worry about bank runs because the government is here to help. In the US, the Federal Deposit Insurance Corporation (FDIC) insures checking

2023-09-28

The call for "price stabilization" was part of the recent Republican debate. Despite its attractive appearance, having the Fed try to "stabilize prices" is a very bad idea.

Original Article: Why Stabilization Policy is Destabilizing

Read More »2023-09-27

Recorded in Nashville, Tennessee, on September 23, 2023.

Limitless Money and the Limitless Fed | Jonathan Newman

Video of Limitless Money and the Limitless Fed | Jonathan Newman

Read More »2023-09-11

Many people believe that the board game Monopoly, developed during the Great Depression, mimics a real-world capitalist economy. Monopoly is a game, not real life.

Original Article: "Is the Monopoly Board Game Like Real Markets?"

2023-09-02

U.S. presidential candidate Vivek Ramaswamy took aim at the Federal Reserve recently:

The reality is, if the dollar is volatile, it’s as bad as if the number of minutes in an hour fluctuated. None of us would be here at the same time. […] When the number of dollars [in relation] to a unit of gold or an agricultural commodity is wildly fluctuating, money doesn’t go to the right projects. It’s just wild—it doesn’t make any sense. That’s been an impediment to economic growth…

So, what we need to do as the next-step—of course I’d like to end it [the Fed]—is at least get rid of the dual mandate. We’re done managing inflation and unemployment. It’s like trying to hit two targets with one arrow, dramatically missing on both. And restore a single mandate: stabilize the US dollar as a unit of

2023-09-01

While the government promotes CBDCs as tools for "inclusion," it is more likely that they will be another vehicle for federal intrusion.

Original Article: "CBDCs: The Ultimate Tool of Financial Intrusion"

Read More »2023-08-30

The "2 percent" inflation target is purely arbitrary, and mainstream economists can’t agree on the "right" level. It’s all folly, and Austrian economics explains why.

Original Article: "What Is the Right Inflation Target for Central Banks?"

Read More »2023-08-17

It feels like a silly thing to say, but board games are not real life. Playing a few rounds of Operation does not make you a surgeon. Unlike in Battleship, real-world battleships do not sit still on a ten-by-ten grid.

Similarly, Monopoly does not correlate to “free-market capitalism,” despite anticapitalist claims like this tweet with over a million views:

There’s literally a children’s board game that demonstrates that “free-market capitalism” always leads to one person controlling everything.— Nina Turner (@ninaturner) July 26, 2023 The rhetorical strategy is obvious: anticapitalists want people to associate capitalism with Monopoly, the game that results in extreme wealth inequality as players bankrupt each other through zero-sum exchanges and often ends with family members storming

2023-08-08

“Experts” at the Federal Reserve and other central banks proudly broadcast the potential “financial inclusion” that could be achieved with a central bank digital currency (CBDC). In the Fed’s main CBDC paper, “Money and Payments: The U.S. Dollar in the Age of Digital Transformation,” they make it clear: “Promoting financial inclusion—particularly for economically vulnerable households and communities—is a high priority for the Federal Reserve . . . a CBDC could reduce common barriers to financial inclusion.”

The term has a ring to it that signals support for progressive goals. “Inclusion” is part of the Orwellian trio of terms “diversity, inclusion, and equity,” which, as Dr. Michael Rectenwald writes, means “surveillance, punishment of the ‘privileged,’ sacrifice of national citizens to

2023-08-07

Government statistics on inflation in the food sector have failed to account for skimpflation and shrinkflation.

Original Article: "Shrinkflation and Skimpflation Are Eating Our Lunch"

Read More »2023-08-05

Why have central banks settled on a 2 percent price inflation target? Project Syndicate asked four economists about this target and whether it is still appropriate. I’ll summarize their answers and then consider Mises’s position on “stabilization policy.”

Four Economists’ Answers to “Is 2 Percent Really the Right Inflation Target for Central Banks?”

Michael Boskin, Stanford University professor, Hoover Institution senior fellow, and former chair of the Council of Economic Advisers to George H.W. Bush, concludes that 2 percent is probably about right, mainly due to the negative consequences of a higher target. He considers whether a higher target could be maintained in a stable way as it comes with more variations in the returns to capital, less credibility regarding the price stability

2023-07-26

The differences between the Austrian school and the mainstream begin at the most fundamental level: method (logic vs. empiricism) and the goal of economic science (understanding vs. prediction).

Download lecture slides at Mises.org/MU23_PPT_19.

Recorded at the Mises Institute in Auburn, Alabama, on 26 July 2023.

Critique of Neoclassical Economics | Jonathan Newman

Video of Critique of Neoclassical Economics | Jonathan Newman

Read More »2023-07-25

What is a business cycle?

Download lectures slides at Mises.org/MU23_PPT_14.

Recorded at the Mises Institute in Auburn, Alabama, on 25 July 2023.

The Austrian Theory of the Business Cycle | Jonathan Newman

Video of The Austrian Theory of the Business Cycle | Jonathan Newman

Read More »2023-04-26

Recorded in Birmingham, Alabama on April 22, 2023.

From the Mises Institute’s recent event in Birmingham, Alabama dedicated to the global threat of "The Great Reset".

[embedded content]

Read More »2023-04-01

Suppose an addict had the ability to magically create, ex nihilo, his own stimulating drug, as fractional reserve banks can do with money and credit. Would you expect moderation?

Original Article: "Why Fractional Reserve Banking Is behind Bank Failures"

This Audio Mises Wire is generously sponsored by Christopher Condon.

2023-03-27

Drug addicts suffer major withdrawal symptoms when they go cold turkey. In the case of high-tech startups and their banks (like Silicon Valley Bank), the super-low-interest-rate stimulant has been taken away by the drug dealer (the Fed) via interest rate hikes. With cheap credit drying up, firms switched to pulling cash out of SVB, all while the same interest rate increases caused the value of SVB’s assets to fall. SVB’s balance sheet couldn’t handle the fast withdrawals, which became a classic, self-propagating, panicky bank run, and the simultaneous fall in value of its liquid assets.

When banks practice this kind of maturity mismatch—potentially immediate-term liabilities (deposits) backed by long-term assets (loans and Treasury securities), it is called “fractional reserve banking.”

2021-05-19

“Every change in the money relation alters … the conditions of the individual members of society. Some become richer, some poorer.” – Mises, Human Action, p. 414. New money enters the economy at a particular point. It does not enter in the form of a proportional and simultaneous increase in everybody’s incomes.

Read More » On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info