Stoked by ultra-loose monetary policy from the Federal Reserve, capital markets have been in a persistent bubble for several years. Printing trillions of new dollars and maintaining a zero-interest rate policy (“ZIRP”) was marketed by politicians and bureaucrats as supportive of the “main street economy,” but those trillions were directed primarily towards speculation in capital markets.

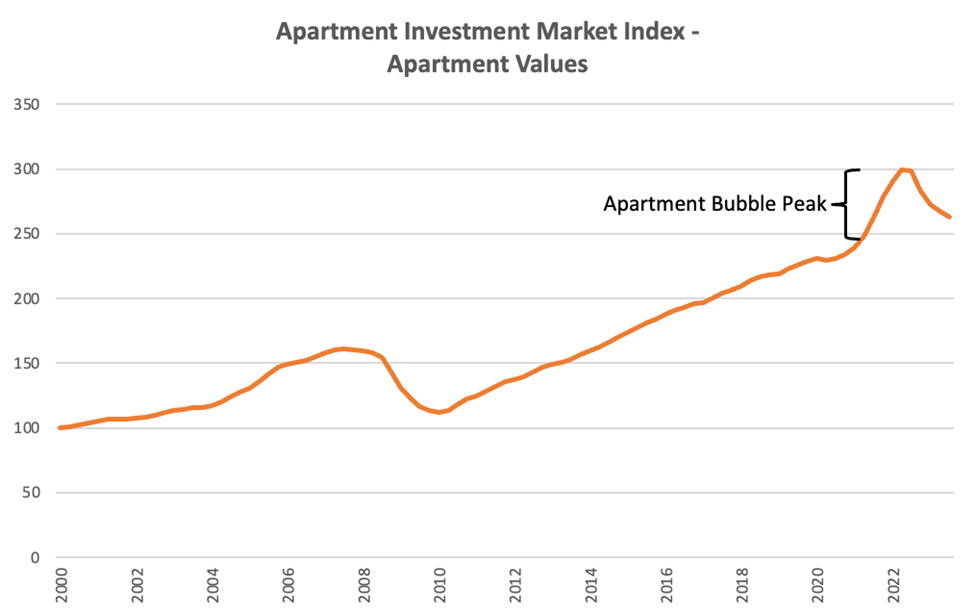

Nowhere was this malinvestment more apparent than in apartment investing. After rising consistently for several years during the Bernanke-Yellen era, valuations for apartment rental properties reached unthinkable levels in the wake of the covid panic and related monetary splurge of 2020-2021. During this time, syndicators with little or no prior experience in real estate investment aggregated small amounts of cash from eager but unsophisticated “investors” into larger pools of capital, with which they voraciously acquired apartments at increasing prices.

Nearly all of this peak bubble activity in apartments was funded with bridge loans. Another spawn of the ZIRP era, bridge loans comprised high leverage, short-term, floating rate loans with minimal credit standards. Just like their borrowers, lenders who provided such capital relied on the naïve presumption that low interest rates would last forever.

With the recent increase in interest rates in response to high consumer prices, the apartment bubble has begun to deflate. While syndicators and their investors have already seen significant distress as a result, recent reports show that bridge loan lenders are now also in deep trouble.

A Perversion of Standards

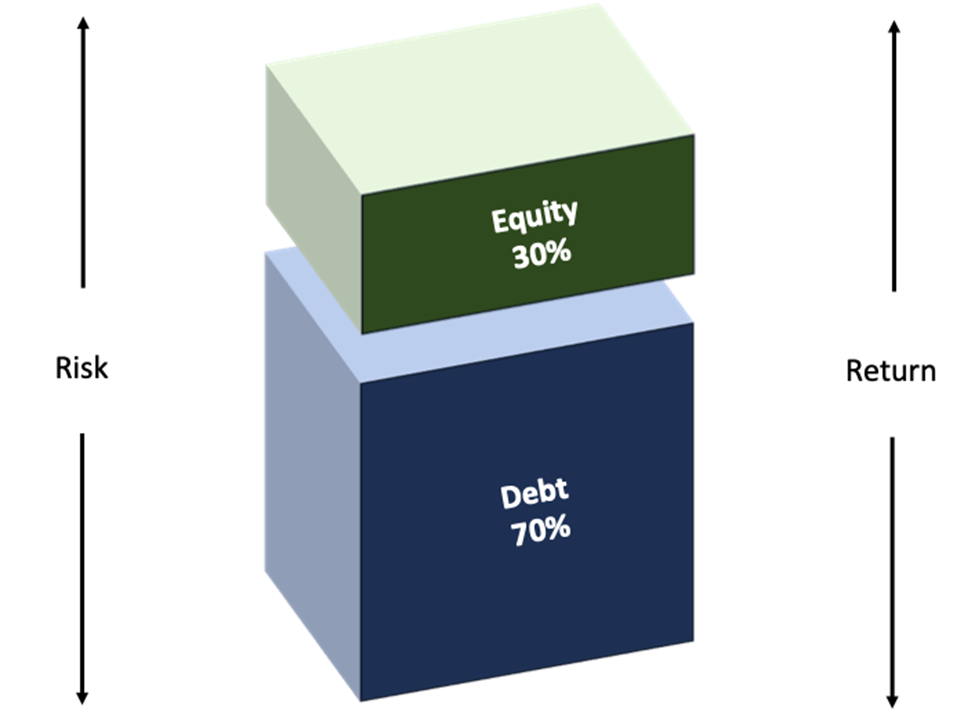

Generally, the structure of an apartment investment is straightforward. Investors obtain a loan (“debt”) to acquire a property and combine that debt with some of their own money (“equity”). The debt typically makes up 70 percent of total capital, with the equity filling in the rest. The capital stack looks like this:

The debt in the capital stack is protected from loss by the equity. In the illustration above, if the overall property value drops by 30 percent, the equity is wiped out, but the debt component retains its value, unimpaired. For taking less risk, lenders generally receive a fixed and fairly low return.

Also, traditionally, purchase prices and loan amounts for apartments were constrained by standard practices in risk management. The cash generated by the property’s operations (“Net Operating Income”) would have to exceed the interest and principal payments due on the loan (“debt service”) by at least 25 percent. In industry terms, a debt service coverage ratio (“DSCR”) of at least 1.25x was required.

In the recent apartment bubble, however, rational practices were discarded. Rather than providing 70 percent of the purchase price, bridge lenders went as high as 85 percent and provided additional lines of credit to fund future property renovations.

Critically, loan amounts and purchase prices were no longer constrained by the property’s proven ability to generate cash, as indicated by actual performance reports. Instead, buyers of these properties were encouraged by lenders to provide projections – literally numbers punched into a spreadsheet – of how the properties would perform once the proposed renovations were completed. As long as those projections resulted in DSCR of at least 1.0x, the bridge loan would be approved.

Superficial analysis would have concluded that these practices were doomed to failure.

Recent reporting from Viceroy Research shines a light on one of the most egregious bridge loan lenders and how their loans and underlying properties are currently performing. The carnage is apparent, and bound to get worse.

The Tide Goes Out

Arbor Realty Trust, a publicly traded firm (NYSE : ABR) based in New York and one of the most active apartment bridge lenders over the last few years, is the archetype for poor lending practices during the apartment bubble.

Viceroy’s reports collect data from Arbor’s collateralized loan obligation (“CLO”) portfolio – essentially, the bridge loans that Arbor packaged and sold into a bond market – which comprises a large part of Arbor’s total book of business.

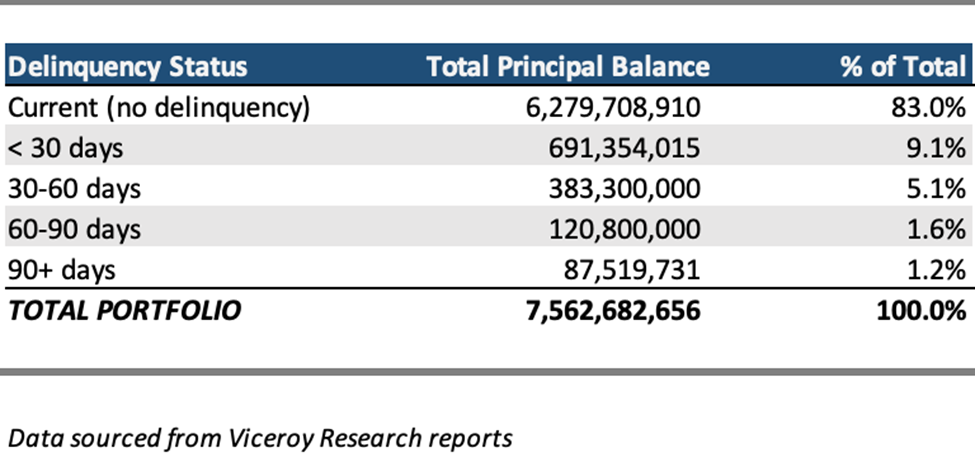

The table below summarizes the portion of delinquent loans, those that have past-due interest payments, in this portfolio as of February 2024.

An astounding 17 percent of loans in this portfolio are delinquent. Historically, apartment loan delinquency rates are below 1 percent.

Incidentally, Arbor’s January delinquency rate was a stunning 26.6 percent. This appears to have dropped in February as a result of borrowers being forced to dip into meager reserves to make outstanding interest payments – a temporary move that only kicks the can down the road, and not far.

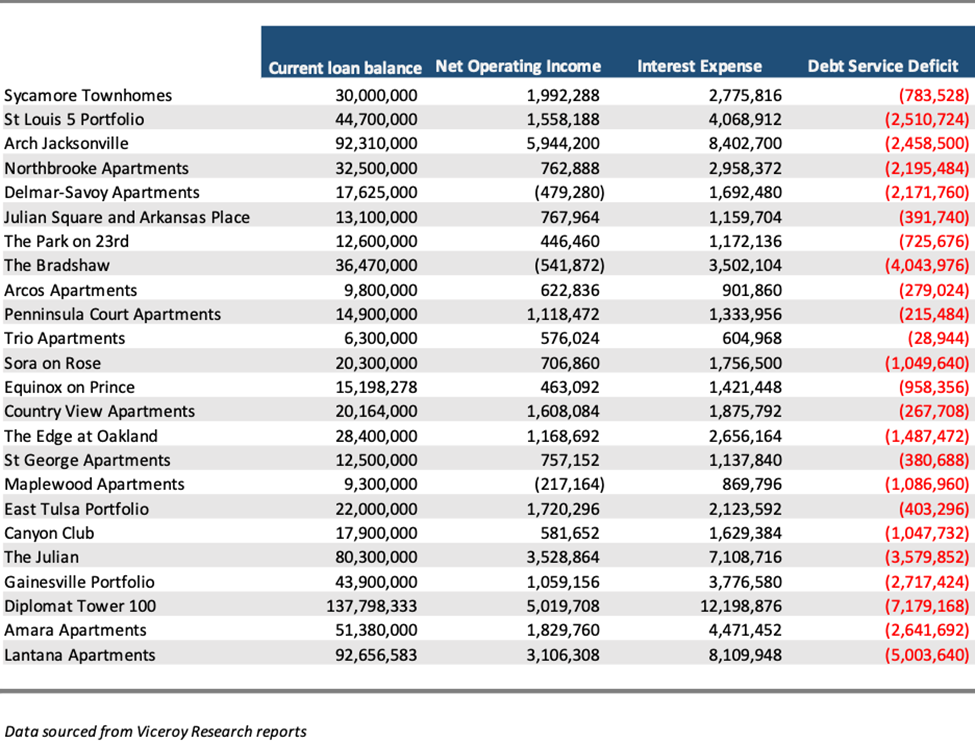

Looking further into the Viceroy data, one finds a subset of Arbor’s CLO portfolio with specific property-level details included.

At every one of the properties illustrated in the table above, representing roughly 12 percent of Arbor’s CLO portfolio, Net Operating Income is insufficient to pay interest expense on the loan.

Viceroy reports that across Arbor’s entire CLO portfolio, the average underlying property generates only $60 in Net Operating Income for every $100 in interest due on its loan.

Using the illustrated data, one arrives at the following conclusions about property values compared to outstanding loan balances within Arbor’s CLO portfolio.

- Of the 24 loans listed, 16 of them (66.7 percent) are under water – the underlying property has a market value less than the balance of the loan.

- Of those 16 loans under water, the average loss on principal is 42 percent. A hypothetical loan of $100 in this group could only recover $58 in the event of a sale at today’s market prices.

The remainder of Arbor’s CLO portfolio is reasonably expected to look similar.

So what’s next for Arbor’s bridge loans, and the vast number of bridge loans nationwide that are similarly situated?

Performing property renovations to improve profitability and meet debt service payments is not feasible. Those business plans have exploded as increasing interest rates consumed all of the cash available at the property level.

Refinancing these loans is also impossible. No lender today can support these loan amounts at current interest rates given the performance of the underlying properties.

Foreclosure is a possible outcome, but even in that case significant work and further capital investment is required just to bring property values up to the level of the loan balance. And a foreclosing party, like Arbor, is generally a financial firm not capable of such productive work.

Thus far, Arbor and other lenders have been unwilling to sell these loans at a loss, perhaps hoping for much-anticipated rate cuts from the Fed. But even that won’t save these loans, as the magnitude of rate cuts needed to reduce debt service to a manageable level is unrealistic. And with price levels in the economy still elevated, those cuts may not come at all.

With no strategies to employ that could increase profitability at the property level and therefore salvage loan values, Arbor’s CLO portfolio, and that of many other similarly situated lenders, is a ticking time bomb.

End Game

Looking at these bridge loans now, one wonders what lenders and borrowers were thinking. But that implies that they were thinking at all. Loose money from the Fed and decades spent reinforcing the notion that poor decisions will always be bailed out played on the minds of those participants with minimal talent and a gambling mentality. Betting on low rates forever, bridge loan lenders enabled a market that was economically implausible, displaying the very definition of irrational exuberance.

Full story here Are you the author?Tags: Featured,newsletter