| Someone asked recently how many times I had “crossed the pond” to Europe. I really don’t know. Certainly dozens of times. It’s been several times a year for as long as I remember.

That makes me an extremely unusual American. Most of us never visit Europe, except maybe for a rare dream vacation. And that’s okay because our own country is wonderful and has a lifetime of sights to see. But it does affect our perspective on the world. Many of us don’t fully grasp how important Europe is to the US and global economy. We may soon get a lesson on that. I’ve talked about Italy’s ongoing debt crisis, which is not improving, but Europe has other problems, too. Worse, events are coalescing such that several potential crises—all major on their own—could strike at the same time, and not too long from now. As I’ve been saying for about three years, there is no reason for the US to have a recession on its own. I think events elsewhere will push us into it, and Europe is a really big current risk. I know from my visits to Europe and discussions with friends there, they see all sorts of problems with Trump and particularly his tariffs. |

APP Monthly Net Purchases by Program, 2015 - 2018 Source: European Central Bank - Click to enlarge |

However, another concern is that the various actors in Europe are not playing nice with each other. I tell my European friends the same forces that yielded Trump are coming to a European country near them. In some places, they already have.

So, in my never-ending quest to keep you ahead of the curve, I’ll review what’s happening “over there.” This may be a turnabout for European readers who rely on me to describe what’s happening over here. But as you’ll see, we are far more connected than separated by distance.

(Note: The link is to my favorite version of “Over There” written by George M. Cohan, here sung by James Cagney in 1942 for the film Yankee Doodle Dandy. It was written at the beginning of World War I and quickly became the number one song of not just that era but also the World War II era. Younger generations may not remember music with so much unbridled, enthusiastic patriotism. They can be excused for not quite understanding such feverish intensity. It was a different era.)

Monetary Drug Withdrawal

Last week my British friend Jim Mellon sent me a fascinating article with an alarming title: “News from Euroland—Recession Imminent.” I’m not certain when Jim sleeps, as I get a few emails from him every day at seemingly random times, always with pithy, on-target reading material. (Although I can usually figure out when he is in Great Britain by their timing.)

Now, I am not one who falls prey to click-bait headlines (nor is Jim) and I’m also well aware Europe’s economy is weakening. I would not have said recession was imminent but reading this article left me more than a little concerned. The author, economist Victor Hill, ties events together in ways many haven’t considered.

Hill begins the piece this way.

Across Europe, and particularly in the 18-member Eurozone, the economic news is sobering. It’s now clear that the credit crunch in emerging markets which has played out over most of this year, plus the slowdown in China, are having negative consequences in Europe. Yet, despite the ongoing trauma of Brexit, the UK is cruising along relatively smoothly—for now.

A number of critical events are about to coincide…

The first such event is the impending end of the European Central Bank’s quantitative easing “Asset Purchasing Programme,” which has been propping up asset prices with wholesale purchases of bonds, stocks, and anything else that isn’t nailed down.

Mario Draghi and his crew borrowed our Federal Reserve’s plan and, if possible, made it even crazier. You can see in the chart they have been stepping down purchases. The pace should reach zero in early 2019. But this doesn’t account for assorted other loan programs, which some would like to see continue or even expand. Germany opposes all such policies and I think will get its way, especially since Draghi will be leaving next year.

This means the Eurozone is about to lose a monetary drug on which it has grown highly dependent. But those 18 nations will not be the only ones affected. The larger EU needs a thriving core to stimulate growth for the whole continent.

Note that Draghi will finish his term as ECB president in October 2019. Economists (what do they know?) project he will make his first interest rate increase just one month before he leaves, in September. That means taking rates from -0.40 bps to -0.20, still below zero.

In all likelihood, his replacement will have to be approved by Germany. What will be the new president’s appetite for negative rates even in the face of recession? Will he listen to the Bundesbank? Will the ECB once again expand its balance sheet? What is left to buy? All good questions with no answers yet but potential market dangers.

And if Europe falls into recession earlier in 2019, will Draghi reverse himself and resume expanding the balance sheet, buying yet more assets that are not nailed down? The Italians would certainly like that.

European Disunion and Brexit

Hill’s second “critical event” is Brexit, the latest plan for which is set for a December 11 vote in the UK’s Parliament. As of now its prospects look dim, at least without changes that the EU sidesays it won’t accept. That may not be true because, as we have learned, European officials are masters at vowing inflexibility and then bending when forced.

But let’s have some sympathy for Prime Minister Theresa May. She is dealing with a rebellion in her own party, has lost numerous votes and it is not clear she can force her (let’s call it) Brexit-lite proposal through Parliament. You can read about her troubles here.

This deal has monster implications for economics and investments and you really need to pay attention. I think I would vote against, not that anyone in Great Britain will care, as it seems to me that her compromise leaves Europe with more control over what a “final” agreement would look like. It’s not exactly what the “leave” crowd originally wanted. But in reality there are no good choices. If this is voted down, I see real chances for problems everywhere.

Another national vote might seem sensible, except that would look like the elites keep taking votes until they get the outcome they want. It would make a large part of the country upset no matter what. As I said, no good choices…

Regardless, it is highly uncertain what happens next. The UK gave formal notice it would leave the EU on March 29, 2019, whether terms of separation are reached by then or not. A “hard Brexit” would be chaotic, to say the least, as it would leave businesses trying to operate in a legal vacuum. World Trade Organization rules might serve as a backstop in some matters but the massive trade volume between the UK and EU would certainly slow. Can they walk that notice back? Fudge a little bit on the date? This is the EU. They can do anything they bloody well like. Damn the rules and full speed ahead…

On the other hand, remaining in the EU would enrage the millions who voted to leave and probably bring down the May government. Where it would go from there is anyone’s guess. It is hard to even imagine “democratic socialist” Jeremy Corbin as Prime Minister. So both economies are probably in for a shock unless some miracle produces orderly separation terms in the next three months, which seems unlikely.

The third critical event, says Hill, is the growing Italian crisis, which I’ve been warning about for quite some time. That kettle is getting ready to boil over. Now banks in Italy are having trouble refinancing their bond issues, which is forcing them to curtail lending to an already-weak private sector. Rising mortgage rates are cutting into consumer spending. Italy is arguably already in recession but the situation looks likely to get worse—which is a big problem for its creditors, mainly Germany, which we will discuss in a bit.

| But Hill says, I think correctly, that the Italian crisis is no longer just economic, if it ever “just” was. It is emblematic of a culture war that is pitting anti-immigration populist movements against “elites” they believe are hostile to their interests. As happened elsewhere, unemployed and working-class people are losing faith in the system. We see this most recently in the violent gas-tax protests in France.

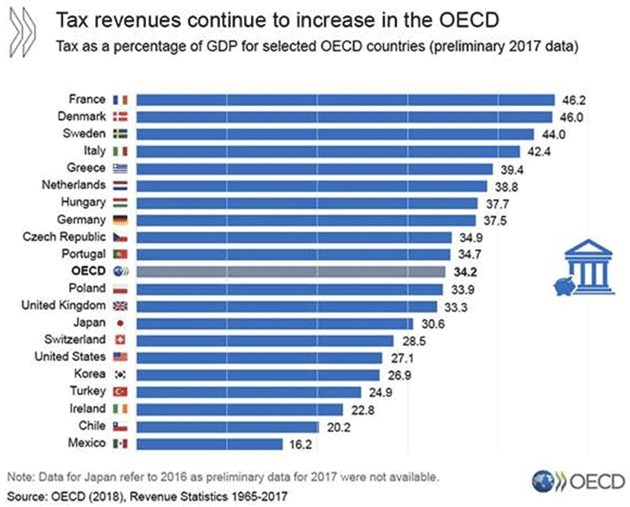

This protest movement has an altogether different feel when you pay close attention. It is not just about higher fuel taxes. It is about almost half the country being angry at the educated city-dwelling elite while the brunt of increased taxes falls on an increasingly burdened rural middle class. The French government now consumes 46.2% of GDP, making it the most-taxed OECD nation. Even a slight tax increase affects the working class disproportionately. And when it increases taxes on something like diesel fuel, which is critical in rural areas, it is particularly hard. |

Tax as a percentage of GDP for OECD selected Countries, 1965 - 2017 Source: Mish Shedlock - Click to enlarge |

In Europe and around the world, we see this pushback against what is seen as an elite group at the top (the “Protected”) which pays no attention to the problems of their less successful “Unprotected” brethren. And those brethren are demanding attention.

This “morality play” is spreading through Europe. We now see German political patriarch Wolfgang Schauble backing a candidate to replace Merkel as head of the CDU (Christian Democratic Union), who is openly courting the same voters that have left their party and gone to the anti-immigration and populist Alternative for Germany (AfD). That means a conservative push for Germany and a more populist approach for mainstream parties.

The common thread running through these events is the idea of a united Europe. This idea was a driving force in the foundation of the European Union and is common in the establishment and/or “elite.” Up until a few years ago, the idea was popular across the political spectrum but support has weakened as economic times changed. It was never particularly feasible, but the effort made sense for a continent so damaged by centuries of repeated wars. The problem is that the EU can’t achieve its goals unless it gets stronger and much of the public has had its fill of centralization. I don’t know how they can solve this. Brexit, if it happens, may turn out to have been the test case for a full dissolution.

How that will unfold is hard to predict. For now, there are more immediate problems. Victor Hill thinks “a disorderly Brexit will be the spark that sets the Eurozone tinderbox aflame in the first half of 2019.” The tinderbox is already full in Italy and France. It won’t take much heat for that kettle to boil over.

But that’s not all.

Trade Threats

Speaking of unity, last weekend’s Buenos Aires G20 summit was a chance for world leaders to forge common ground on important global issues. That’s not exactly what happened but President Trump’s trade discussion with Chinese president Xi Jinping looked initially like a bright spot. They agreed to stop making things worse for a few months, at least. Markets were more skeptical after digesting the news—rightly so, at least from my standpoint.

As I’ve said, there are real issues with China on intellectual property and more. It is not unreasonable to ask for an open and fair playing field. China is no longer an emerging market nation. It has emerged, at least the eastern half. Beijing should play by the same rules as the rest of the developed world. But getting agreement with China is going to be a hard slog.

One encouraging but little-reported G20 event: US Secretary of State Mike Pompeo and Treasury Secretary Steven Mnuchin gathered their peers from the smaller G7 group for an unscheduled dinner. According to Ian Bremmer, they made significant progress on working together to solve the China issues. This should be positive if it continues.

Meanwhile, however, Louis Gave explains why problems with China may be bad news for Europe at a time when Europe doesn’t need any more challenges (bold is mine).

It is no secret that Trump is surrounded by men who want to “take China down,” who have argued at length that China is a house of cards built on unsustainable credit, and that all the US needs to do is give a gentle nudge for the whole edifice to come crashing down. So far, this talk of China’s vulnerability has proved way off-target. For all of the dire predictions of an imminent debt crisis and financial meltdown, China is still standing very much upright.

So, if Trump wants a win, where should he look? If a long cold war of attrition with China doesn’t look promising, perhaps bashing Europe—specifically Europe’s auto industry and lack of defense spending—could prove more attractive, especially as Europe is now politically rudderless and economically slowing. My bet would be that in the coming weeks, Trump stops speaking about China, and instead starts bashing Europe. And doubtless his favorite targets will be France and Germany, perhaps as payback for the slights he endured at last month’s commemoration of the World War I armistice. If nothing else, Trump has shown that he is a firm believer in the old adage that revenge is a dish best served cold.

I pay attention when Louis speaks. He often sees events that happen “around the curve.” His premise is simple: The automotive industry drives the German economy. Germany, in turn, drives the European economy. So if Trump decides to follow through on the car tariffs he’s threatened, it could be a serious blow. German auto executives met with him in Washington this week but the threat is still alive.

Oh, and one more thing. Deutsche Bank, Germany’s financial crown jewel, seems to be in deep trouble. Its shares, which never recovered from the 2007–2008 ugliness, dropped to all-time lows this week after German police raided the bank’s offices in a money-laundering probe. We don’t know exactly what the fire is but there sure is a lot of smoke. Other European banks are not exactly thriving but DB seems to be in particular trouble.

It is hard for us in the US to realize how important European banks are. European businesses, particularly small ones, get almost all their financing from banks. When Italian banks have trouble funding their bonds, that means Italian businesses will suffer.

So add all this up. We could see Europe faced with monetary tightening, hard Brexit, an Italian breakdown, popular unrest not just in France but all over, a trade war and a German/Italian bank crisis all at the same time. Again, this is not a far-off possibility. It could all be happening in the next three or four months.

If some combination of these crises develops into a perfect storm, the pain won’t stay in Europe. US, Canadian, Latin American, and Asian companies that do business with Europe will lose sales and have to lay off workers. Lenders everywhere who own Euro debt will face losses. Highly leveraged derivatives could blow up, forcing bailouts and currency interventions. We don’t know where it would lead but certainly nowhere good.

And it will end up being played out in the equity markets all over the world. Stay tuned…

The markets have been quite volatile for the past few weeks. My preferred ETF trading strategy, called Mauldin Smart Core, has performed well in this environment. Full disclosure, I have recently closed my own personal investment advisory firm down and moved my registration to my longtime friend Steve Blumenthal of CMG. As a personal business strategy, he has all the infrastructure and team to support me, and it really does allow me to spend more time researching and reading and writing. I am co-portfolio manager for the Mauldin Smart Core strategies which is available as a mutual fund or managed accounts.

We have done a report called “Investing During the Great Reset,” which explains our strategy and rationale. If nothing else, it will show you how I want to deal with the risk of a coming potential bear market and give you ideas for doing it yourself or in your own firm. Of course, I hope that some of you will become clients. But I am perfectly willing to help you whether you do or not. I want as many people as possible to get from where we are today to the other side of The Great Reset.

Full article on Mauldin Economics

| Gold price, monthly chart |

Gold Price, Monthly Jan 2013 - Nov 2018(see more posts on gold price, ) Source: KingWorldNews - Click to enlarge |

| Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below |  |

Full story here Are you the author?

Tags: Daily Market Update,gold price,newsletter