Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The week ahead sees three major central bank meetings and the US employment report. It will likely be the most important work before a hiatus that runs through the end of August. Of course, and perhaps more than ever, market participants are well aware that the US President’s communication and penchant for disruption is a bit of a wild card. That said, the equity market has learned to take individual company references in stride. The fed funds market quickly judged that the President’s criticism of the Fed’s course would not alter it. The dollar, on the other hand, hasn’t been able to resume the climb that Trump’s comments arrested.

The Bank of Japan, the Federal Reserve, and the Bank of England meet in the week ahead. The outlook for the Federal Reserve is the most certain. It will stand pat and not say anything in the statement that would undermine expectations for continued gradual normalization of policy. Indeed the statement itself needs only minor adjustments. The general assessment of the economy it provided in June won’t have to be tweaked much to keep it relevant. Its judgment that the risks to the outlook of roughly balanced will likely be retained.

Fed officials do recognize the risks posed by the rising trade tensions, and this could find a way into the statement. Since the FOMC will wait until the late-September meeting to hike rates again, when there will be updated forecasts and a press conference, there is little to dissent about. However, there is some precedent for dissents from a regional president over an economic characterization. Atlanta Fed’s Bostic, who appears to be the most concerned among voting FOMC members of the risk of an inverted curve, could be such a potential candidate.

The outcomes of the central bank meetings either side of the FOMC meeting are less clear-cut. The Bank of England meets on August 2, the day after the Fed. The market is fairly confident that the BOE will approve a 25 bp rate hike, even though as of July 23, one of the central bank’s Deputy Governors, Broadbent, was still undecided about his vote. Separately Broadbent is regarded as one of the leading candidates to replace Carney who will stem down toward the middle of next year.

While the market is comfortable with a few more hikes by the Fed, investors are less convinced about the BOE. Consider that the two-year Gilt yields 75 bp, which would be the same as the base rate if assuming a 25 bp increase on August 2. The US two-year premium over the UK continues to widen on a trend basis. It is approaching 200 bp, Since at least the early 1990s, it had not been above 40 bp before the end of 2016. It is up about 45 bp since the end of 2017.

A steady FOMC, with nothing to dissuade expectations for a September hike, a hawkish hold may characterize it. BOE Governor Carney may indicate that rates will still likely need to increase over the medium-term, the market is skeptical that the conditions will allow another hike this year. Brexit risks remain substantial, and preparations for no deal are increasing. In fact, households and businesses were to have begun receiving weekly information updates from the government about how to prepare for a disorderly Brexit, but the anxiety that would have spurred made official cancel this initiative.

United KingdomEven if the UK’s two main parties favor leaving the EU, there is no agreement either within the Tory Party or between it and Labour for any specific form of Brexit. This has produced a muddle of a negotiating position. Regardless of how one evaluates Prime Minister May’s political acumen, reconciling the internal differences and the EU demands may be too much for any politician, which, in part, may explain why May has yet to face a leadership challenge. Investors are confident that the Fed will stand pat, after all since it began hiking rates at the end of 2015, it has only moved on meetings with pre-scheduled press conferences. Starting next year, there will be a press conference after every meeting. There is no reason to expect Powell to lead to deviation from this pattern in H2. Investors are also confident that the BOE will raise rates. If it does not, sterling will immediately sell-off. The outcome of the Bank of Japan meeting is the least clear. |

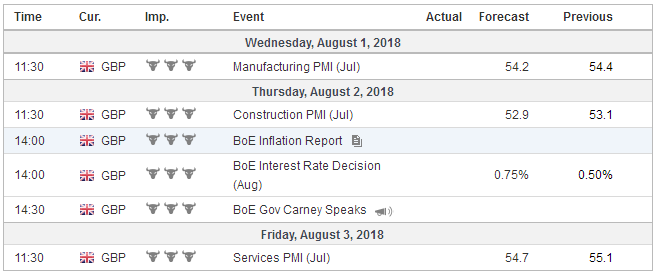

Economic Events: United Kingdom, Week July 30 - Click to enlarge |

JapanThe BOJ has slowly reduced the amount of government bonds that it buys. Its Yield Curve Control initiative of targetting 10-year yield near zero (+/- 10 bp) required it to purchase fewer bonds than the Quantitive and Qualitative Easing program. In April, the BOJ dropped from its formal statement any reference to meeting its inflation target in FY19. Most of the rise in consumer prices Japan reports is due to fresh food and energy. Excluding these, CPI rose 0.2% year-over-year in June and ticked lower every month of Q2 after rising at a 0.5% pace in March. There is some speculation that the BOJ could lower its inflation target to 1.5%. We suspect that too much political significance has become attached to the 2% target no matter how unrealistic it may be. Indeed, the BOJ shares what arguably has become a fetish among major central banks of two percent inflation more or less regardless of precisely how it is measured. Corporate earnings have been poor, and the economic data shows no sign of turning. BOJ officials seem to recognize that its unorthodox efforts will need to continue to the foreseeable future and need to be put on more sustainable footing. The unintended consequences need to be minimized. It appears that officials are engaged in a comprehensive review, and it is not clear if a decision will be made at this week’s meeting or let for the September or even October meetings. A range of action is possible. There could be an attempt to steepen the yield curve, and this would likely entail a higher target for the 10-year bond yield. Last week, the BOJ offered to buy unlimited bonds, first at 11 bp (and there were no sellers) and at 10 bp ahead of the week (less than $100 mln of bonds were reportedly sold). There are other ways to steepen the curve, like reducing the yield at the shorter-end, if not a more negative deposit rate, capping short-dated coupon yields. The BOJ may reconsider buying negative yielding corporate bonds. It may also re-direct its equity purchases from ETFs tied to the Nikkei toward ETFs linked to the Topix. Other measures may also be considered. However, one thing that we do not think is on the table is buying foreign bonds. From time to time, this idea resurfaces. The Swiss National Bank offers precedent. However, such an initiative by the BOJ would look too much like intervention in the currency market, which would likely incur the wrath of the easy-to-anger Trump Administration, which Prime Minister Abe, like many others, are trying to minimize. |

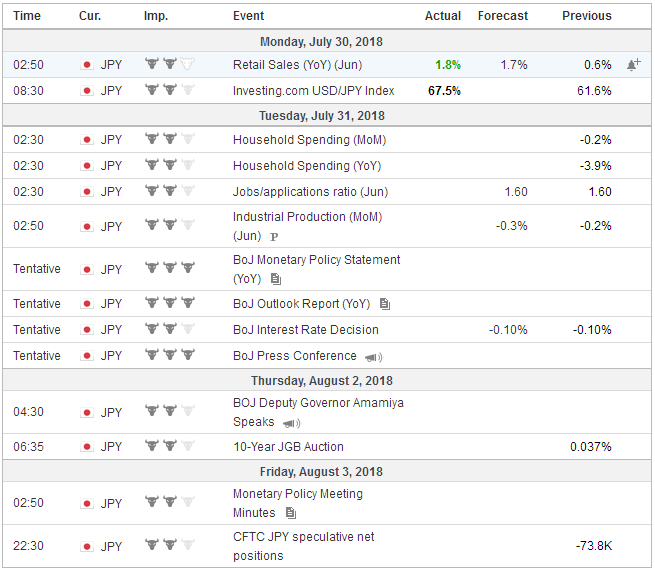

Economic Events: Japan, Week July 30 - Click to enlarge |

United StatesWhile the central bank meetings will be the chief focus, the most important high-frequency economic data will be the US jobs report. US job growth has accelerated this year. Non-farm payrolls rose by an average of 215k in the first half compared to a 182k average in 2017 and 195k in 2018. There are not many inputs economists can use to forecast the monthly figure. What we do know is that the regional Fed surveys and the preliminary Markit PMI were narrowly mixed. We also know that weekly initial jobless claims fell to a new cyclical low in the same week that the national employment survey is conducted, though the four-week moving average did not change very much. Economists also recognize that Q2 GDP (4.1%) was flattered by several one-off considerations and growth in Q3 is expected to return closer to the recent average closer to 2.5%. The net consequence is that most economists look for job growth to have cooled in July to a little below 200k. In June, the metals industry gained employment, and this seemed to have been related to the import-substitution effect of the steel and aluminum tariffs. We are concerned that the negative impact on metal consumers may be slower to bleed into the data. This would suggest the risk of slower manufacturing job growth. Keener interest than a largely in line net job growth will be on the hourly earnings. A 0.3% monthly increase is needed to keep the year-over-year rate steady at 2.7%. The firming of nominal earnings may have helped pull people back into the labor market. The participation rate rose from 62.7% to 62.9%. It has not been above 63.0% since March 2014. Hourly earnings are only one of several measures of compensation. The Employment Cost Index is another. It is a quarterly release and includes not only wages, bonuses, and in-kind payment, but also indirect costs, like taxes and health care. The ECI is slowly rising. Over the past 20 quarters, it has increased at an average rate of 0.57%, and over the past eight quarters, the average rose to 0.64%. In the four quarters through March 2018, the average pace ticked up to 0.65%. A 0.7% increase in Q2, which is what the median forecast projects, would lift the four-quarter average to 0.7% as well. That would be the fastest pace in a decade. Although the jobs report often injects volatility in the foreign exchange market, we suspect barring a significant surprise, outside of the knee-jerk reaction, views on the dollar and the trajectory of Fed policy are unlikely to change. The chances of a fourth Fed hike this year, which would most likely be delivered in December, will not be altered by the data from the start of Q3. Meanwhile, trade tensions with Europe have de-escalated, and there seems to be a window of opportunity before the US midterm campaigns are ramped up to get a NAFTA deal. Meanwhile, trade the next set of tariffs and counter-tariffs ($16 bln) with China could be announced shortly. |

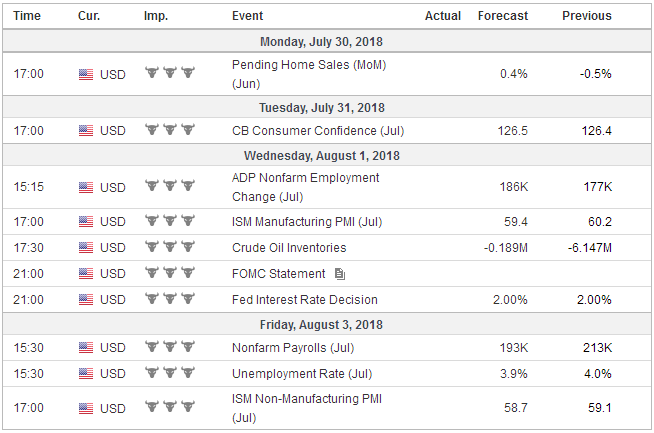

Economic Events: United States, Week July 30 - Click to enlarge |

Switzerland |

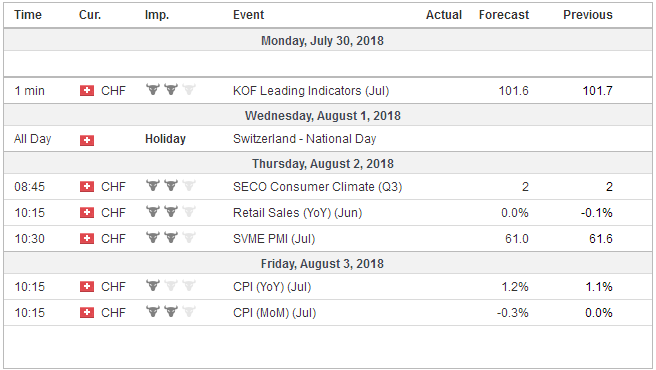

Economic Events: Switzerland, Week July 30 - Click to enlarge |

Tags: Bank of England,Bank of Japan,Federal Reserve,jobs,newslettersent