Another ECB meeting, another balanced message of confidence and prudence. Unsurprisingly, the statement mentioned the deterioration in the data flow since March, but our impression is that the ECB is largely brushing off concerns about a soft patch in the economy for the moment.

Indeed, Mario Draghi described the recent “moderation” in growth as the result of a pullback in sentiment from elevated levels, with economic expansion expected to remain solid and broad-based across countries and sectors. Moreover, “temporary factors” were said to go a long way in explaining the extent of the loss in momentum, including weather conditions, strikes, or the timing of Easter, all of which are expected to reverse. External risks were mentioned, including the threat to global trade and a stronger currency, although concerns eased on balance. In the end, Draghi described the ECB’s stance as one of “caution tempered by confidence in the convergence of inflation” towards the 2% target over the medium term.

| Draghi said that the Governing Council did not discuss monetary policy “per se”, waiting for more hard evidence before they update their assessment of the situation. He may have lied – it happened before – but the bottom line is that upcoming data releases will therefore receive greater scrutiny. We see downside risks to April inflation and May PMI indices, which may well be enough for the ECB to delay its next decision to the July meeting.

However, we expect the data to prove the ECB right eventually, and our scenario remains unchanged. We continue to expect the ECB to taper its asset purchases in Q4 2018 and to start hiking rates in Q3 2019. |

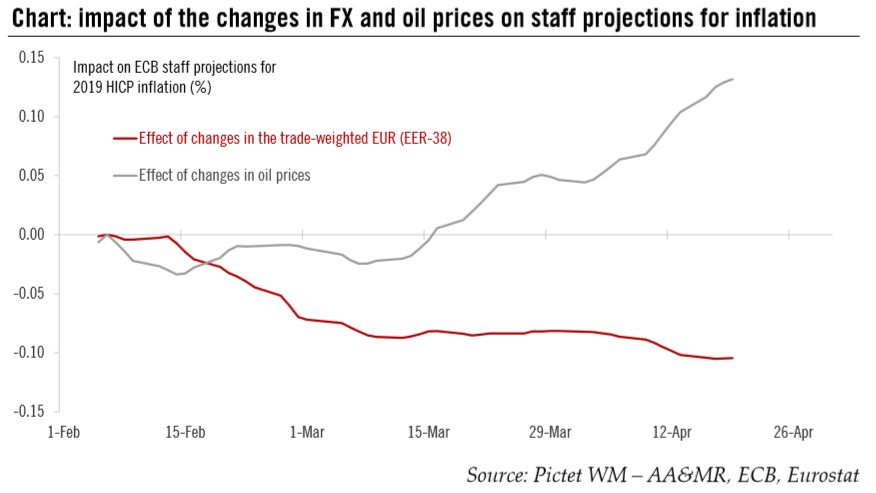

Impact of the Changes in FX and Oil Prices on Staff Projections for Inflation, Feb - Apr 2018 - Click to enlarge |

With this in mind, here are the most important deadlines to be monitored in the coming weeks:

- April flash HICP inflation (3 May): we expect euro area core inflation to drop from 1.0% to 0.8% y-o-y in April as the Easter effect on services disappears, only partly offset by a rebound in core goods inflation. Looking ahead, we forecast core inflation to rebound to above 1% before a large base effect pushes it higher in October.

- Q1 GDP first estimate (15 May): weak hard data look consistent with a sharp slowdown in Q1 GDP growth to around 0.1-0.2% q-o-q, down from 0.7% in the previous quarter, while soft data still point to around 0.6% growth. We expect Q1 GDP to come in somewhere in between those estimates, but in any case below the ECB staff projection of 0.7%.

- May PMI indices (23 May): our forecasts are consistent with business survey stabilising at around current levels, but forwardlooking PMI components point to downside risks in the near term.

- ECB staff projections: ahead of the 14 June meeting, the ECB staff will extract technical assumptions from market prices and expectations in the two-week period ending on the cut-off date which we expect to be 22 May. At this stage, the effect of higher oil prices on inflation has more than offset the drag from a slightly stronger currency in trade-weighted terms (see Chart).

- EU summit (28-29 June): the topics to be discussed at the dedicated Euro summit will be of critical importance to the medium-term outlook, including the banking union. The risk of a disappointing outcome has increased judging by recent comments from German officials (or lack thereof), which in turn could put more pressure on the ECB to be even more gradual.

In the end, the broad framework that will shape the upcoming normalisation of the ECB’s monetary stance has been described extensively in recent months, and in a very consistent way by the hawks and the doves alike. It should be no surprise that the hawks have been stressing the “confidence” part of the exit strategy while the doves have emphasised the “prudence, persistence, patience” parts. Today Draghi chose to stick with a very balanced message. The ECB might want to wait until July before they make a decision, but what matters is what happens in Q4 2018 and beyond, and we expect the data to prove them right eventually.

Full story here Are you the author?Tags: ECB policy,ECB staff forecasts,Macroview,newslettersent