| The Chinese economy ended 2017 on a strong note. In Q4 2017, China’s GDP amounted to Rmb23.4 trillion (about USD3.7 trillion), rising 1.6% over the previous quarter and 6.8% year-over-year (y-o-y) in real terms. Full-year GDP came in at Rmb82.7 trillion (about USD12.9 trillion), growing by 6.9% in real terms and beating the consensus forecast as well as our own estimate (both at 6.8%).

The strong 2017 growth number marks the first full-year acceleration in the Chinese economy since 2010, thanks to the synchronised global economic expansion and a booming domestic consumer sector. In light of the continued strength of external demand and signs of stabilisation in fixed asset investment, we have decided to revise up our Chinese GDP forecast for 2018 to 6.5% from 6.3% previously. |

China Real GDP Growth, 2001 - 2018(see more posts on China Gross Domestic Product, ) - Click to enlarge |

| Below we summarise some details about China’s latest GDP report.

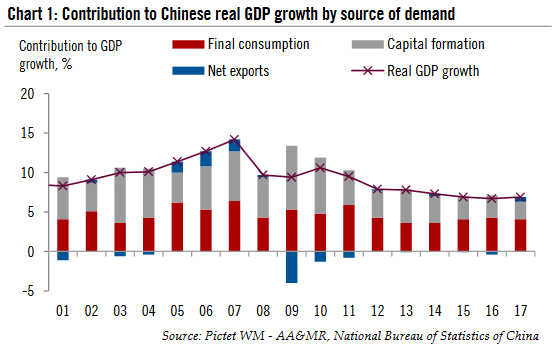

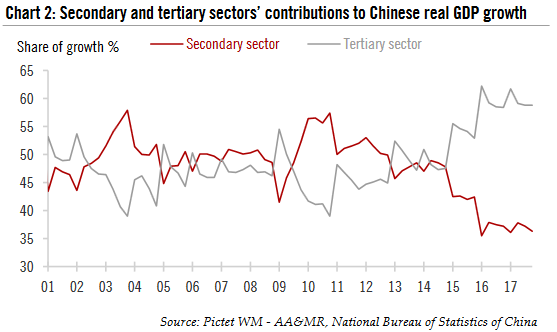

First, the transition of China from an investment-driven economy towards a consumption-and service-driven one is well underway. In 2017, consumption contributed 4.1 percentage points to the 6.9% headline growth (59.4%). While this represents a slight decline from 2016 (64.1%), it is significantly higher than consumption’s average contribution during 2001-2015 (49.5%). In contrast, capital formation’s contribution to the headline GDP growth figure was 2.2 percentage points in 2017, or 31.9% of the total, down from 41.8% in 2016 and an average of 53.0% in the 15 years since 2001 (Chart 1). By sector, the tertiary sector (mainly services) continues to be the key driving force of the economy, accounting for 59.6% of the headline growth in 2017, the same as in 2016, while the secondary sector’s contribution (mainly manufacturing) was 40.4% (Chart 2). Services began to outstrip manufacturing around 2010, with the growth differential accelerating in 2015. |

Chinese Real GDP Growth, 2001 - 2018(see more posts on China Gross Domestic Product, ) - Click to enlarge |

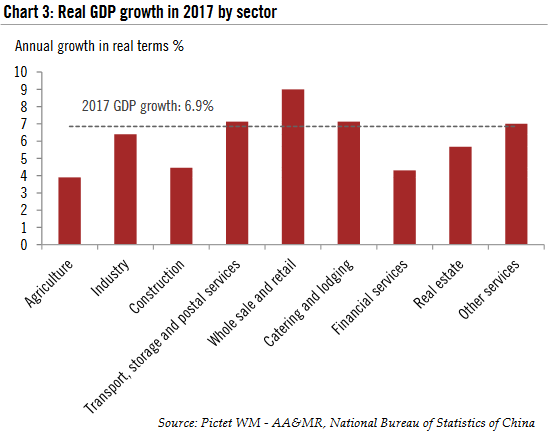

| In more detail, whole sale and retail, catering and lodging and transport, storage and postal services were the sectors that showed the highest growth in 2017 (Chart 3). The first two are obviously related to household consumption, while the strong growth in the logstics sectors was likely due to the surge of online shopping in China, which is growing at a much higher speed than retail sales in general. |

Real GDP Growth, 2017(see more posts on China Gross Domestic Product, ) - Click to enlarge |

| Second, net exports turned out to be the biggest positive surprise in Chinese growth in 2017, contributing 0.6 percentage points to the headline GDP figure, compared to a drag of 0.4 percentage points in 2016 (Chart 1). This represents the large st contribution of the external sector to Chinese growth in a decade. The rise in net exports more than offset the slight decline in the growth in consumption and the deceleration in fixed asset investment (FAI) in 2017.

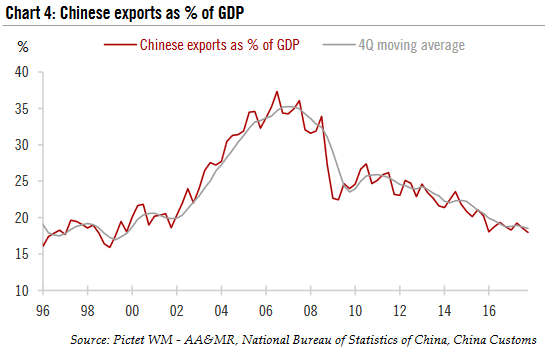

Despite the strong growth in export s in 2017, the Chinese economy’s dependance on exports continues to decline. The export-to-GDP ratio was at 18.0% in Q4 2017, the lowest since Q3 1997. Domestic demand, especially from household consumption, is becoming increasingly important in driving Chinese growth. |

Chinese Exports, 1996 - 2018 - Click to enlarge |

| Looking ahead, we expect China’s growth momentum to moderate somewhat in 2018, mainly on the FAI front, but exports and consumption will likely continue to provide solid support to the economy. But even for FAI, the potential downside may be less than what we had been expecting as the property sector is beginning to show more resilience on declining inventory. The government’s efforts to deleverage the economy and clean up the environment will likely create some short-term headwinds to growth, but they will also help generate higher-quality growth with lower financial risks.

In short, the upward revion of our outlook for the Chinese economy in 2018 is mainly based on the stronger-than-expected global economy and potentially less downside in fixed investment. On the external front, our global macro research team recently upgraded its GDP forecast for Europe. Under the new scenario, we expect the euro zone economy to expand by 2.3% in 2018 (vs.1.7% in the previous forecast). And our forecast for the US GDP growth for 2018 will be revised up soon. In Asia, the Japanese economy will likely grow by 1.3% in 2018 and is on track to record the longest continuous economic expansion in more than three decades. The ASEAN economies, led by Indonesia, Thailand and Malaysia, may also see their growth rate pick up further in 2018 after a solid 2017. Combined, these four countries and regions account for over half of Chinese total exports. In light of the upward revisions to the outlook for major economies, the Chinese export sector may see continued support from external demand (Chart 5). |

Chinese Export Growth and Global Manufacturing PMI, 2011 - 2018 - Click to enlarge |

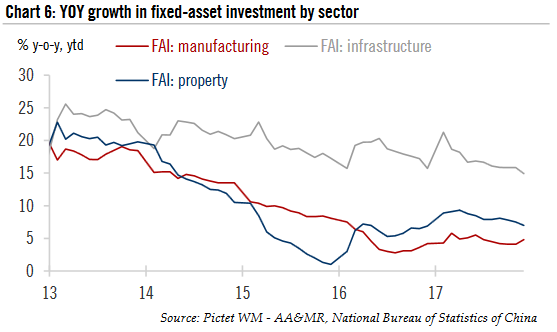

| In fixed investment , it appears that the government has eased back on the pedal in terms of infrastructure investment, applying greater scrutiny to projects to avoid excessive fiscal burdens on local governments. On the other hand, investment in the manufacturing sector is showing signs of stabilisation, possibly due to the improving profitability of industrial companies and the upgrade demand from Chinese manufacturers, which are increasingly turning to automation and moving up the value chain (Chart 6). |

Growth in Fixed-asset Investment, 2013 - 2018 - Click to enlarge |

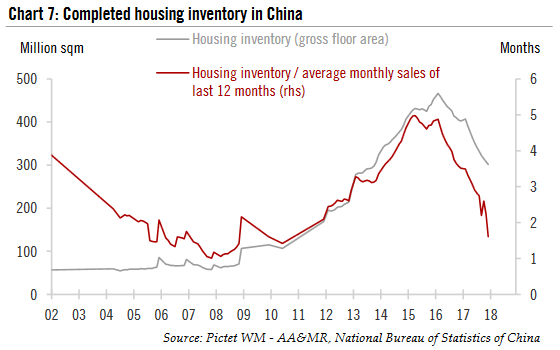

| It’s especially worth mentioning that some recent data release s have led us to believe that the potential downside to investment in the property sector may be less than we previously expected. While many Chinese local governments will likely continue to enforce home purchase restrictions to curb housing speculation, real demand remains strong, especially in lower-tier cities. In the last two months of 2017, housing prices in tier-3 cities in China started to pick up again on a month-over-month basis, along with transaction volumes.

More importantly, after strong sales in 2016-17, housing inventory has declined dramatically. In absoluate terms, the inventory of completed housing units fell to 302 million square metres at end-2017, roughly equivalent to where it was at end-2013. But if measured by the average monthly sales over the past 12 months, the current inventory has dropped to similar levels as in end-2011, which is close to the lowest since records began in 2002 (Chart 7). In our view, the very low housining inventory will provide support to housing construction in 2018, so that any further downside to property investment might be fairly limited. |

China Housing Inventory, 2002 - 2018 - Click to enlarge |

The risks to our more bullish view of the Chinese economy in 2018 include increasing trade protectionism, especially from the Trump administration, and the possibility that the headwinds caused by the Chinese government’s efforts to deleverage the economy and to reduce pollution are more than expected.

Although we do not believe a full-scale trade war between the US and China is likely, there are signs that the Trump ad ministration is starting to apply more protectionist measures against the US’s trading partners. So far, these measures have only target ted specific products and thus are limited in scope (e.g., punitative tariffs on imported washing machines and solar panels) . On the domestic policy front, we believe the downside risks of any turn in government policies are likely to be manageable, although the possibility of policy mistakes cannot be ruled out. We will continue to monitor future development s closely and will re-evaluate our scenarios accordingly.

Full story here Are you the author?Tags: China Gross Domestic Product,Macroview,newslettersent