Summary

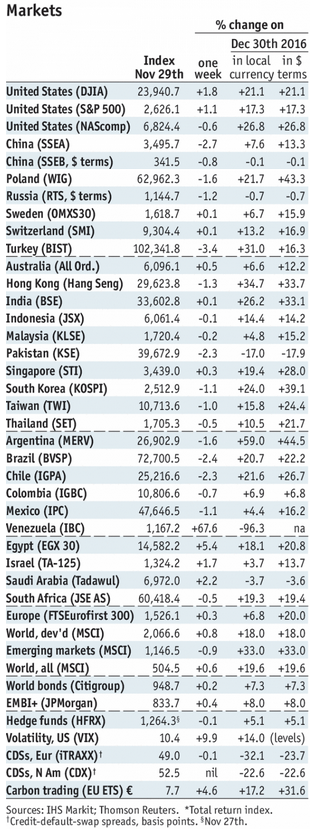

Stock MarketsIn the EM equity space as measured by MSCI, Egypt (+2.4%), Czech Republic (+1.1%), and Korea (+0.8%) have outperformed this week, while China (-4.8%), Hungary (-4.4%), and Brazil (-3.8%) have underperformed. To put this in better context, MSCI EM fell -3.2% this week while MSCI DM rose 0.4%. In the EM local currency bond space, Argentina (10-year yield -27 bp), Czech Republic (-21 bp), and Turkey (-17 bp) have outperformed this week, while Brazil (10-year yield +25 bp), South Africa (+11 bp), and Mexico (+5 bp) have underperformed. To put this in better context, the 10-year UST yield was flat at 2.34%. In the EM FX space, ZAR (+3.1% vs. USD), TRY (+0.9% vs. USD), and PHP (+0.8% vs. USD) have outperformed this week, while CLP (-1.9% vs. USD), BRL (-0.7% vs. USD), and COP (-0.5% vs. USD) have underperformed. |

Stock Markets Emerging Markets, November 29 Source: economist.com - Click to enlarge |

KoreaBank of Korea hiked rates by 25 bp to 1.50%, the first hike in six years. There was one dissenter, who expressed concern about low inflation. Korea reported November CPI today, and inflation fell sharply to 1.3% vs. 1.8% in October, further below the 2% target. Governor Lee said that policy will remain accommodative, so we do not see another hike until the inflation trajectory warrants it. EgyptEgypt central bank lifted the last remaining currency controls. It removed the limits imposed in 2015 on deposits and withdrawals by importers of non-essential goods. This follows a similar move in June, when the central bank ended the cap on FX transfers of $100,000. Senior official said that “We saw it as appropriate to remove the caps today because the market has strengthened [and] our foreign-currency resources have increased.” Note also that the central bank increased the cost of using its special FX window by adding a 1% surcharge to new inflows. South AfricaS&P cut South Africa’s foreign currency rating one notch to BB with stable outlook. More importantly, S&P cut the local currency rating to BB+, which will lead to ejection from the Barclays Aggregate index. That same day, Moody’s put South Africa’s Baa3 rating on review for possible downgraded, noting that “The review period may not conclude until the size and the composition of the 2018 budget is known next February.” If it is downgraded to Ba1 as we expect, South Africa would then be ejected from Citi’s WGBI. TurkeyTurkey President Erdogan was implicated in an alleged plot to help Iran evade US sanctions. Trader Reza Zarrab reportedly laundered billions of dollars on behalf of Iran and entered into a plea deal. Zarrab testified that senior Turkish officials told him that Erdogan personally agreed to a plan to involve two Turkish banks in the process. Afterwards, Erdogan claimed that Turkey did not break any embargoes on Iran as it hadn’t committed to the US sanctions. He added that there were no UN sanctions in place at the time. ArgentinaMoody’s upgraded Argentina one notch to B2 with stable outlook. Our own sovereign ratings model shows Argentina’s implied rating rose a notch to B+/B1/B+. This suggests further upgrade potential for actual ratings of B+/B2/B, as Macri’s reform program bears fruit. MexicoThe IMF approved a new $88 bln Flexible Credit Line (FCL) for Mexico. The new 2-year FCL replaces the old one, which was canceled at the same time. IMF Managing Director Christine Lagarde noted that “Mexican macroeconomic policies and policy framework remain very strong” but added that “Risk of an abrupt change in Mexico’s trade relations or a risk of market volatility and a sharp pull-back from emerging markets continues to be high.” Mexico shook up its economic team. Finance Minister Jose Antonio Meade resigned to become the PRI’s presidential candidate in the July 2018 election. Jose Antonio Gonzalez Anaya will step down as CEO of Pemex to become the new Finance Minister. Meade had been widely expected to either run or become the new Banxico Governor. In that regard, it was also announced that Deputy Governor Diaz de Leon will take up that post effective today. We see little impact from the moves on Mexico’s macroeconomic policies. BrazilBrazil press is reporting that the pension reform vote may be delayed to 2018 due to lack of support. Lower House Speaker Maia said he won’t schedule a vote until there is enough support to pass it. The government will reportedly try to win support for the reforms at a dinner scheduled for this Sunday with senior officials of its allied parties. |

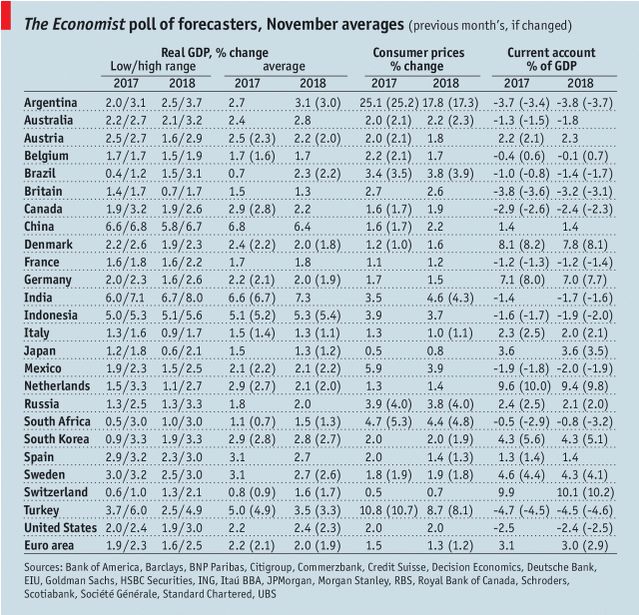

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, November 2017 Source: economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets,newslettersent