Andréa M. Maechler, Member of the Governing Board of the Swiss National Bank

News conference of the Swiss National Bank, Berne, 14.12.2017

Complete text: PDF (478 KB)

I will begin my remarks with a review of the situation on the financial markets, before going on to discuss the progress made in reference interest rate reform.

Situation on the financial marketsLet me start with developments on the financial markets.

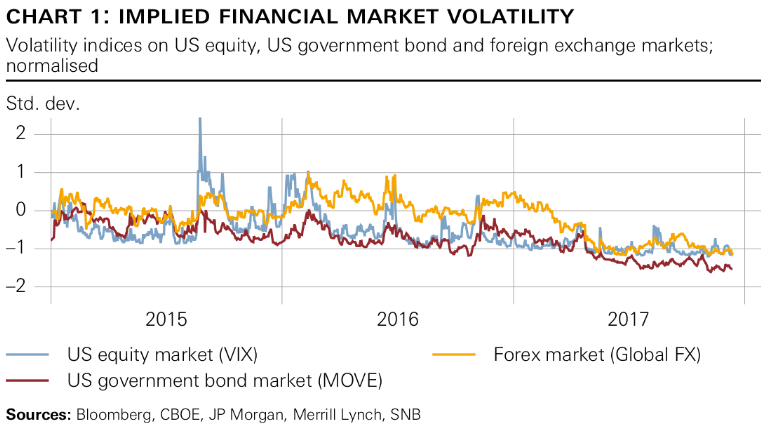

The monetary policy pursued by the large central banks was once again the focus of attention for the financial markets in the second half of the year. Given moderate inflation growth, financial market participants are expecting only a very gradual normalisation of monetary policy across the world. Against this backdrop, government bond yields have remained persistently low. Muted expectations regarding a move away from expansionary monetary policy, coupled with favourable economic data and good corporate results, have contributed to largely positive risk sentiment on the financial markets. This has been reflected, for instance, in a stock market rally, lower yield spreads on corporate bonds and reduced demand for safe-haven assets such as the Swiss franc. In this positive market environment, volatility has remained low and volatility for the US equity and bond markets, calculated using option

prices, has dropped to record lows.

|

Implied Financial Market Volatility, 2015 - 2017 Source: www.snb.ch - Click to enlarge |

Stock MarketsDespite positive economic data in Europe, European stock indices have risen only moderately. The Stoxx Europe 600 has climbed some 3% since mid

-year. One reason for the modest stock market performance in Europe is the strengthening of the euro, which impaired corporate earnings growth somewhat. By contrast, US companies recorded a strong increase in profits. Furthermore, the prospect of lower corporate tax rates raised expectations of higher profits in the future. Against this background, US stock indices reached record highs. The S&P 500 has risen by about 10% since mid-year. Swiss companies have benefited from stronger demand from Europe and the weaker Swiss franc. The Swiss stock market (SMI) also made substantial gains, up some 5%.

|

Global Equity Markets, Jul - Dec 2017 Source: www.snb.ch - Click to enlarge

|

Bond RatesThe low yields on ten-year government bonds from advanced economies have remained virtually unchanged since mid-year. In the US too, although key rate normalisation is underway and the Federal Reserve has initiated balance sheet reduction, longer-term yields have risen only marginally until now.

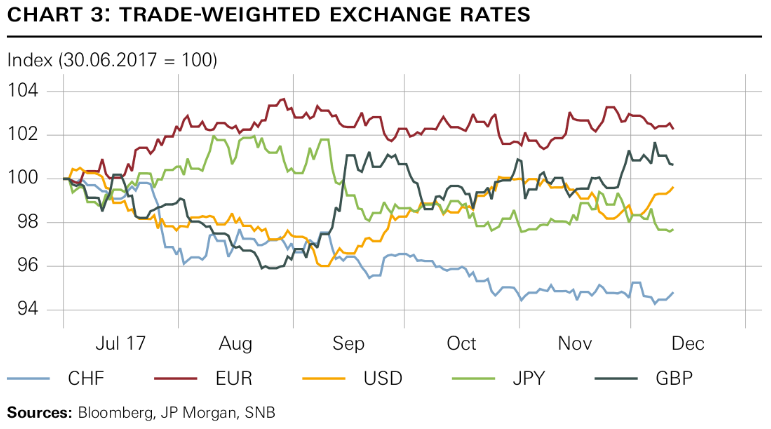

Exchange RatesOn the foreign exchange market, the US dollar initially continued on the downward path it had been following since the beginning of the year. The dollar then strengthened again somewhat from autumn onwards against the backdrop of the Federal Reserve’s ongoing monetary policy normalisation and the prospect of tax reform. As Thomas Jordan already mentioned, reduced political uncertainty and favourable economic developments in the euro area contributed to the appreciation of the euro. In this environment, the Swiss franc has lost some 5% of its trade-weighted value since mid-year. The depreciation largely occurred over a few days at the end of July, but the downward trend – broad-based across the market and founded on good market quality – continued over the following months.

|

Trade-Weighted Exchange Rates, Jul - Dec 2017 Source: www.snb.ch - Click to enlarge |

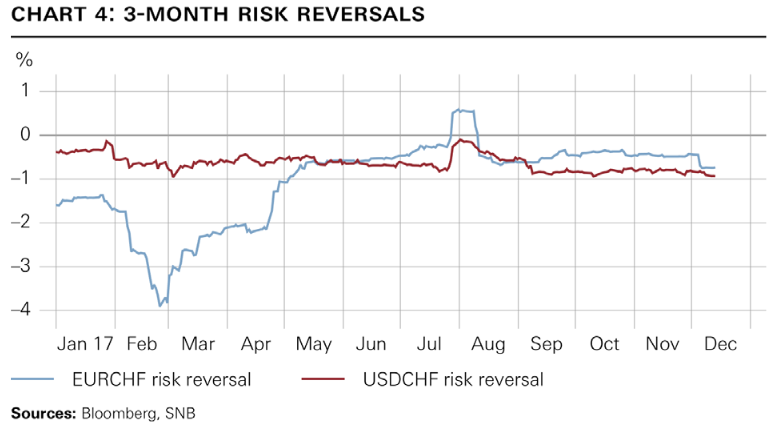

Option MarketsOverall, the situation on the foreign exchange market remains fragile, however. Despite the positive market environment, the Swiss franc has not weakened any further in recent weeks. The risk of renewed Swiss franc appreciation remains, particularly if there is a return to risk aversion in the market. A look at the option markets shows that investors are still prepared to pay a higher premium to hedge against Swiss franc appreciation than against its depreciation.

|

3-Month Risk Reversals, Jan - Dec 2017 Source: www.snb.ch - Click to enlarge |

Progress made in reforming reference interest rates.

Let me turn now to reference interest rate reform.

The Financial Conduct Authority (FCA) in the UK announced in July of this year that it would not guarantee the continuation of Libor beyond 2021. The reason for this is that the volume of money market transactions underlying Libor – unsecured interbank loans – has been low for a number of years. The FCA will exercise its power to compel panel banks to take part in the Libor panel only until the end of 2021. After that, the possibility of Libor disappearing fairly quickly due to the withdrawal of panel banks can no longer be excluded. The period until the end of 2021 should now be used by market participants to ensure an orderly transition from Libor.

As one of the key global reference interest rates, Libor continues to be used in a wide variety of credit agreements and derivatives contracts. The Libor-based interest rate swap curve

(‘swap curve’) plays a particularly important role. Interest rate swaps are derivatives transactions involving the exchange of long-term, fixed-rate and short-term, variable-rate interest payments. The variable interest rates are usually linked to Libor. These swap contracts can involve maturities of several years or decades. The swap curve thus extends over the full

maturity spectrum of financial transactions.

In Switzerland too, Libor – the Swiss franc Libor, to be specific – is extensively used as a benchmark. According to an SNB survey on lending, Libor and its swap curve are applied as

the base rate for determining interest rates in a major portion of Swiss franc lending business. The swap curve also plays a key role in price-setting on the Swiss franc capital market.

Given its significance, the shift away from Libor poses major challenges for financial market participants. The process is being coordinated and supported, internationally and nationally, by various committees on which both market participants and authorities are represented.

Faced with the likely demise of the Swiss franc Libor, the national working group on reference interest rates has recommended using SARON (Swiss Average Rate Overnight) as an alternative. SARON reflects the interest rate conditions for collateralised money market transactions with one-day maturity. It is based on actual transactions and binding quotes from

a large number of market participants and is calculated according to a standard and transparent process. It thus accurately represents market conditions. Since April of this year, prices for interest rate swaps have been set on the basis of SARON. Although this market is not yet fully established, a SARON-based swap curve may indeed one day be used as the basis for pricing bonds and loans.

Whether SARON finds widespread use and a planned and orderly transition away from Libor does take place is ultimately in the hands of financial market participants. They should be

prepared for a possible discontinuation of the Libor benchmark from 2021, for instance by agreeing how existing Libor-linked contracts are to be handled.

As you know, the Swiss franc Libor is also used by the SNB – as the reference rate for its monetary policy. There is one thing we can say for sure today: a move away from the Swiss franc Libor would have no impact on the SNB’s monetary policy stance. Any adjustments necessitated by such a transition will be announced in due course.

She was born in Geneva in 1969. She studied economics at the University of Toronto, and then at the Graduate Institute of International Studies in Geneva, where she obtained her Master's in International Economics. Following a period of study at the Institute of Advanced Studies in Public Administration in Lausanne, she obtained her PhD in International Economics from the University of California, Santa Cruz in 2000.

Tags: newslettersent