Stock MarketsEM FX ended the week under pressure, as US data points to a rate hike in December and perhaps more in 2018. FOMC minutes this Wednesday will be closely studied for clues. US retail sales and CPI data Friday will also be important. We believe the most vulnerable currencies in this environment are ZAR and TRY, but one could also add MXN and perhaps RUB to that mix too. |

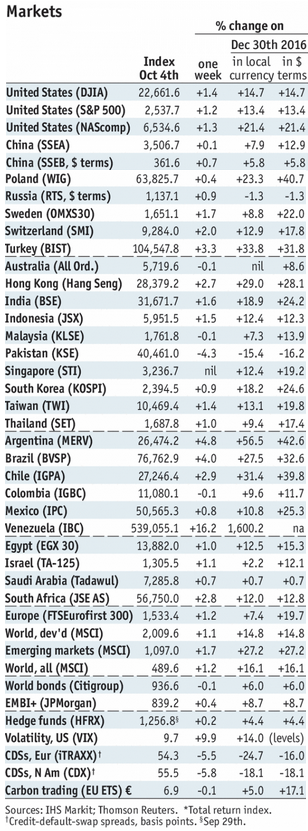

Stock Markets Emerging Markets, October 07 Source: economist.com - Click to enlarge |

ChinaChina reports September foreign reserves Monday, which are expected to tick up to $3.1 trln. Money and new loan data could come out this week, but no date has been set. Trade data will be reported Friday. Exports are expected to rise 9.8% y/y and imports by 15.2% y/y. TurkeyTurkey reports August IP Monday, which is expected to rise 5.1% y/y vs. 14.5% in July. Turkey then reports current account data Wednesday, where a -$1.35 bln deficit is expected. If so, the 12-month total will remain steady at -$37.1 bln. Overall, the external balances are still deteriorating. Czech RepublicCzech Republic reports August industrial and construction output and September CPI Monday. IP is seen rising 4.2% y/y vs. 3.3% in July, while CPI is seen rising 2.7% y/y vs. 2.5% in August. Rising inflation and a fairly stable exchange rate should lead the central bank to hike rates at the next meeting November 2. HungaryHungary reports August trade Monday, where a EUR480 mln surplus is expected. It then reports September CPI Tuesday, which is expected to rise 2.7% y/y vs. 2.6% in August. If so, it would still be within the 2-4% target range. The central bank just eased at the September meeting, and so no changes are expected at the next policy meeting October 24. MexicoMexico reports September CPI Monday, which is expected to rise 6.46% y/y vs. 6.66% in August. If so, this would be the first deceleration since June 2016. Still, inflation would still be well above the 2-4% target range and so Banxico is likely to keep rates steady until it comes down further. Mexico then reports August IP Thursday, which is expected to contract -0.5% y/y vs. -1.6% in July. RussiaRussia reports Q2 current account Tuesday, where a deficit of -$2.8 bln is expected. If so, this would be the first deficit since Q3 2013, and the 4-quarter total would fall to $32.9 bln from $36.1 bln in Q2. Russia then reports August trade Thursday, where a surplus of $5 bln is expected vs. $4 bln in July. ChileChile reports September trade Tuesday. Export growth has been robust in recent months, helped by higher copper prices. However, import growth remains restrained due to the sluggish economy, and so the 12-month total surplus has been rising. The external accounts should remain in solid shape. TaiwanTaiwan reports September trade Wednesday. Exports are expected to rise 13.4% y/y and imports by 8.2% y/y. The external accounts remain in good shape, and export orders remain strong enough to suggest that this trend will continue. BrazilBrazil reports August retail sales Wednesday, which are expected to rise 4.4% y/y vs. 3.1% in July. The economy is finally picking up, as is inflation. This supports the central bank’s intent to slow the pace of easing. We look for a 75 bp cut to 7.5% on October 25 followed by a 50 bp cut to 7% on December 6 that should effectively end the easing cycle. MalaysiaMalaysia reports August IP Thursday, which is expected to rise 5.6% y/y vs. 6.1% in July. The economy remains fairly robust, but policymakers are likely to err on the side of cautions. CPI rose 3.7% y/y. Bank Negara does not have an explicit inflation target, and so can keep rates on hold for now. Next policy meeting is November 9, and no change is expected then. South AfricaSouth Africa reports August manufacturing production Thursday, which is expected to rise 0.1% y/y vs. -1.4% in July. The economy remains very weak, which is why we think the SARB will resume cutting rates at the November 23 meeting. IndiaIndia reports September CPI and August IP Thursday. The RBI is looking for inflation to continue accelerating this year, which would justify its decision to remain on hold this month. The next policy meeting is December 6, and we do not expect any change then. PeruPeru central bank meets Thursday and is expected to keep rates steady at 3.5%. CPI rose 2.94% y/y in September, just within the 1-3% target range. The bank has been cutting rates at every other meeting since it started the easing cycle in May. As such, we look for the next 25 bp cut to 3.25% at the November 9 meeting. SingaporeSingapore reports August retail sales Thursday. Singapore then reports Q3 advance GDP Friday, which grew 2.9% y/y in Q2. The MAS holds its semiannual policy meeting on the same day. While the economy is picking up, we do not expect a change in policy then. However, there is a chance that the MAS changes its forward guidance to set up possible tightening in April. |

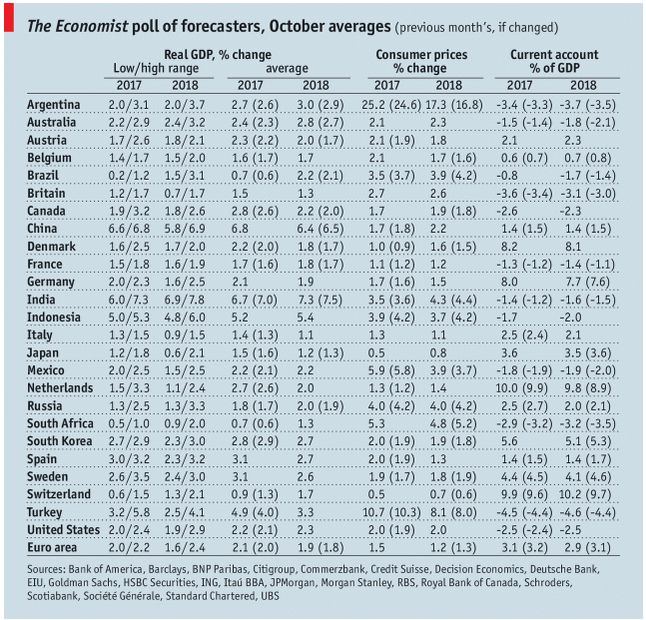

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, October 2017 Source: economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets,newslettersent,win-thin