Stock MarketsEM FX firmed Friday, but capped off a bad week overall. US jobs data this Friday is unlikely to provide much clarity on Fed policy, though we think it remains on track to hike again in December. The Fed’s balance sheet reduction will start this month. We remain negative on EM, and believe selling pressures are likely to persist in Q4. |

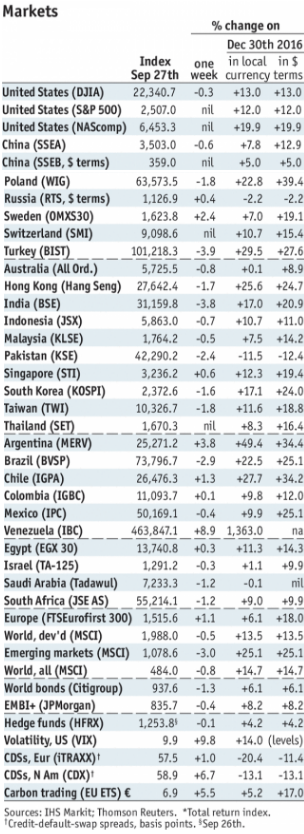

Stock Markets Emerging Markets, October 02 Source: economist.com - Click to enlarge |

ThailandThailand reports September CPI Monday, which is expected to rise 0.5% y/y vs. 0.3% in August. If so, it would still be well below the 1-4% target range. Some analysts are calling for an eventual rate cut, but we believe steady rates will be seen for the foreseeable future. Next policy meeting is November 8, and rates are likely to be kept steady then. IndonesiaIndonesia reports September CPI Monday, which is expected to rise 3.7% y/y vs. 3.8% in August. If so, it would still be in the bottom half of the 3-5% target range. Next policy meeting is October 19. BI just cut rates 25 bp two meetings in a row, and both were dovish surprises. Three cuts in a row seem too aggressive and so for now, we expect steady rates this month. BrazilBrazil reports September trade Monday. It then reports August IP Tuesday, which is expected to rise 5.1% y/y vs. 2.5% in July. Brazil reports September IPCA inflation Friday, which is expected to remain steady at 2.46% y/y. If so, it would remain below the 3-7% target range. Next COPOM meeting is October 25, and rates are likely to be cut 75 bp to 7.5% then. TurkeyTurkey reports September CPI Tuesday, which is expected to rise 11.1% y/y vs. 10.7% in August. If so, it would move further above the 3-7% target range. Next policy meeting is October 26, and rates are likely to be kept steady then. Whilst the central bank has said it could tighten more, we think it will be under pressure from the government not to. ChileChile reports August retail sales Tuesday, which is expected to rise 5.0% y/y vs. 4.2% in July. Chile then reports September CPI Friday, which is expected to remain steady at 1.9% y/y. If so, it would still be below the 2-4% target range. However, the bank has signaled that rate cuts are over, at least for now. Next policy meeting is October 19, and rates are likely to be kept steady then. HungaryHungary reports August retail sales Wednesday, which are expected to rise 4.4% y/y vs. 4.2% in July. The central bank will also release its minutes that same day. Hungary then reports August IP Friday, which is expected to rise 2.9% y/y WDA vs. 0.2% in July. The economy remains robust, and yet the central bank eased again at its September meeting. Next policy meeting is October 24, and no change is expected then. IndiaReserve Bank of India meets Wednesday and is expected to keep rates steady. CPI rose 3.4% y/y in August, which is up from the trough of 1.5% y/y in June but still in the bottom half of the 2-6% target range. The RBI sees inflation rising further in the coming months, and so we see steady rates for the time being. PolandNational Bank of Poland meets Wednesday and is expected to keep rates steady at 1.5%. CPI rose 2.2% y/y in September, higher than expected but still in the bottom half of the 1.5-3.5% target range. The economy remains robust, but many central bank officials believe steady rates are warranted through next year. PhilippinesThe Philippines reports September CPI Thursday, which is expected to rise 3.2% y/y vs. 3.1% in August. If so, it would still be well within the 2-4% target range. Next policy meeting is November 9, and rates are likely to be kept steady then. The bank sees inflation remaining near the 3% target in both 2017 and 2018. ColumbiaColombia reports September CPI Thursday, which is expected to rise 4.11% y/y vs. 3.87% in August. If so, it would move back above the 2-4% target range for the first time since May and explains the central bank’s recent cautiousness. The central bank just kept rates steady Friday. The 5-2 vote supports my view that the easing cycle is not over yet. Next policy meeting is October 27, and rates could be cut then. MalaysiaMalaysia reports August trade Friday. Exports are seen rising 23.6% y/y and imports by 20.8% y/y. The economy is picking up, with Bank Negara recently saying growth is coming in stronger than expected. However, with an election looming next year, we believe rates will be kept steady for the time being. Next policy meeting is November 9, and no change is expected then. Czech RepublicCzech Republic reports August retail sales and trade Friday. Sales are expected to rise 4.6% y/y, while the trade surplus is expected at CZK5 bln. The economy remains robust, but the central bank wants to wait until its November 2 meeting before deciding to hike again. At that meeting, new staff forecasts will be available. The vote in September was 4-3 in favor of steady rates. TaiwanTaiwan reports September CPI Friday, which is expected to rise 0.90% y/y vs. 0.96% in August. The central bank does not have an explicit inflation target. However, low price pressures allowed it to keep rates steady at 1.375% at its quarterly policy meeting in September. The central bank cut its 2017 inflation forecast then to 0.8% from 1.07% in June. RussiaRussia reports September CPI Friday, which is expected to rise 3.2% y/y vs. 3.3% in August. If so, inflation would move further below the 4% target. Next policy meeting is October 27, and rates are likely to be cut 25 bp to 8.25%. After it cut 50 bp in September, Governor Nabiullina said rates were likely to go lower. However, she noted that its cautious stance could result in pauses as well as cuts of 25-50 bp, depending the situation. |

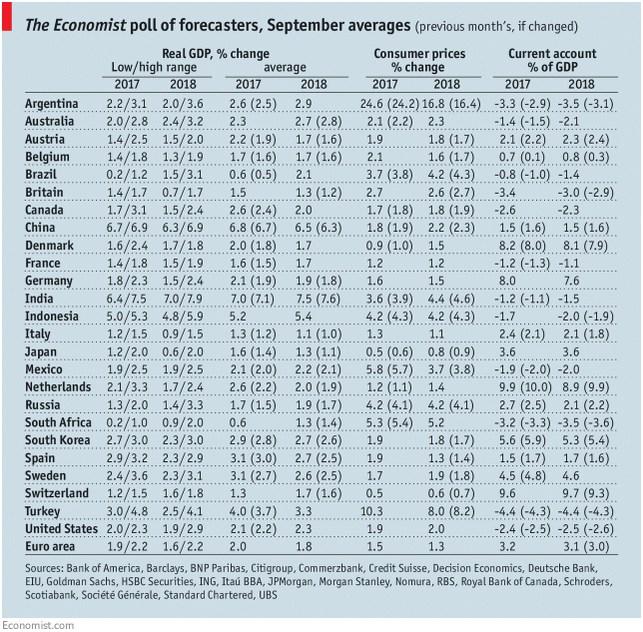

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, September 2017 Source: economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets,newslettersent,win-thin