Summary:

Stock MarketsIn the EM equity space as measured by MSCI, Brazil (+3.1%), Russia (+1.8%), and Colombia (+1.3%) have outperformed this week, while South Africa (-2.0%), Poland (-2.0%), and Turkey (-1.9%) have underperformed. To put this in better context, MSCI EM rose 0.1% this week while MSCI DM was flat. In the EM local currency bond space, Brazil (10-year yield -32 bp), Indonesia (-22 bp), and Russia (-18 bp) have outperformed this week, while India (10-year yield +5 bp), Argentina (flat), and Chile (flat) have underperformed. To put this in better context, the 10-year UST yield fell 10 bp to 2.06%. In the EM FX space, MYR (+1.8% vs. USD), BRL (+1.7% vs. USD), and ILS (+1.6% vs. USD) have outperformed this week, while KRW (-0.4% vs. USD), HUF (-0.3% vs. EUR), and CZK (-0.2% vs. EUR) have underperformed. |

Stock Markets Emerging Markets, September 11 Source: economist.com - Click to enlarge |

South KoreaSouth Korea completed installation of the THAAD missile shield. Four remaining missile launchers arrived at a military base in South Korea. Incoming President Moon Jae-in opposed the early installation of the shield and had suspended new deployment. However, North Korea’s recent actions have forced Moon’s hand. Moon claims THAAD deployment will be temporary.

IndonesiaIndonesia is considering issuing its first global IDR-denominated sovereign bonds. The Finance Ministry is reportedly in talks with the central bank to assess the potential impact of such debt issuance. Local currency bonds issued under New York law are considered more attractive than those subject to domestic law. TaiwanTaiwan is undergoing a cabinet shuffle. President Tsai Ing-wen named popular southern Taiwan Mayor William Lai as the new Prime Minister after the previous one Lin Chuan resigned. With the rest of the cabinet submitting resignations, Lai will oversee a reorganization of the government and its policy priorities. President Tsai’s popularity dropped to an all-time low of 29.8% in a survey last month. RussiaRussia’s central bank is likely to resume the easing cycle. Governor Nabiullina said the bank is likely to discuss 25 or 50 bp cuts at the next policy meeting on September 15. CPI rose a record low 3.3% y/y in August.

BrazilBrazil’s central bank signaled that the easing cycle is nearing an end and that the pace of easing will slow. This suggests a 75 bp cut at the October 25 meeting and perhaps a 50 bp cut at the December 6 meeting, which would take the policy rate to 7%. The latest weekly central bank survey sees an end-2017 SELIC rate of 7.25%, but IPCA inflation was reported at a lower than expected 2.46% y/y in August. Given the inflation trajectory, we think there are some risks of a sub-7% SELIC rate.

Brazil has seen some positive political developments. Former PT official Palocci told Carwash Judge Moro that former President Lula received bribes from Odebrecht. Former President Rousseff was also named. This could derail Lula’s efforts to run again next year. Elsewhere, President Temer’s hand may be strengthened by reports that the plea deal for JBS executives is being reviewed and may be revoked.

ChileChile’s central bank boosted its growth forecasts. In its latest quarterly report, the bank sees 2017 growth between 1.25-1.75%, up from 1.0-1.75% previously. Growth is seen picking up to 2.5-3.5% in 2018. It noted “Growth will gradually resume faster rates of expansion, supported by a more favorable external environment, the end of the mining downturn, the absence of macro-economic imbalances and a clearly expansionary monetary policy.” |

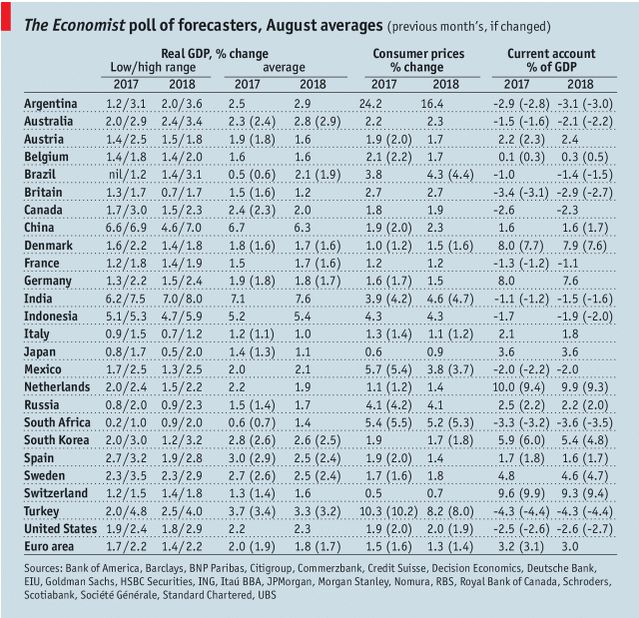

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, August 2017 Source: economist.com - Click to enlarge |

Are you the author?

Tags: newslettersent,win-thin