Stock MarketsEM FX ended the week on a mixed note, as investors await fresh drivers. US jobs data on Friday could provide more clarity on Fed policy and the US economy. Within EM, many countries are expected to report lower inflation readings for June that support the view that most EM central banks will remain in dovish mode for now. We remain cautious on the EM asset class near-term. |

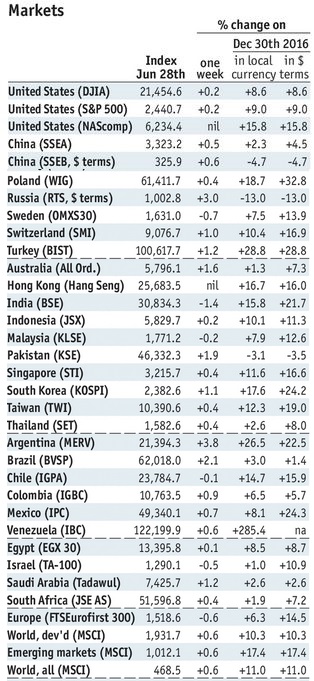

Stock Markets Emerging Markets, June 28 Source: economist.com - Click to enlarge |

ChinaCaixin reports June China manufacturing PMI Monday, which is expected at 49.8 vs. 49.6 in May. Official manufacturing PMI was already reported at 51.7 vs. 51.2 in May. While the two series often diverge, we warn of upside risk to the Caixin reading. For now, markets are comfortable with China’s macro outlook. ThailandThailand reports June CPI Monday, which is expected to remain flat y/y. This remains well below the 1-4% target range. Bank of Thailand meets Wednesday and is expected to keep rates steady at 1.5%. Indeed, with no price pressures to speak of, we believe rates will remain steady into 2018. IndonesiaIndonesia reports June CPI Monday, which is expected to remain steady at 4.3% y/y. This remains well within the 3-5% target range. Bank Indonesia next meets July 20 and is expected to keep rates steady at 4.75%. While the bank has signaled an end to the easing cycle, we do not see any tightening in 2017. TurkeyTurkey reports June CPI Monday, which is expected to rise 11.2% y/y vs. 11.7% in May. If so, this would be the lowest since February but still well above the 3-7% target range. Next policy meeting is July 27 and no change is expected then. Until inflation has fallen significantly more, we believe rates will be kept steady. ChileChile central bank releases minutes Monday. Chile also reports May retail sales Monday, which are expected to rise 2.8% y/y vs. -0.4% in April. Chile then reports June CPI and trade Friday. CPI is expected to rise 2.0% y/y vs. 2.6% in May. If so, this would be the lowest since October 2013 and would be right at the bottom of the 2-4% target range. Next policy meeting is July 13 and no change is expected then. MexicoMexico reports June PMI Monday. Banco de Mexico will release its minutes Thursday. At that meeting, the bank hiked 25 bp but signaled that the tightening cycle was over. Mexico then reports June CPI Friday, which is expected to rise 6.34% y/y vs. 6.16% in May. Next policy meeting is August 10 and no change is expected then. We think the easing cycle might start in Q4, but much will depend on global developments. BrazilBrazil reports June trade Monday. It then reports May IP Tuesday. Brazil reports June IPCA inflation Friday, which is expected to rise 3.1% y/y vs. 3.6% in May. If so, this would be the lowest since April 2007 and would be very close to the bottom of the 3-6% target range. Next COPOM meeting is July 26 and markets are split between a 75 bp and 100 bp cut. We lean towards 75 bp. KoreaKorea reports June CPI Tuesday, which is expected to remain steady at 2.0% y/y. This is right at the BOK’s target. The central bank next meets July 13 and is expected to keep rates steady at 1.25%. Korea then reports May current account data Wednesday. The external accounts remain in very good shape, which should help underpin the won. PhilippinesPhilippines reports June CPI Wednesday, which is expected to rise 3.0% y/y vs. 3.1% in May. If so, that would be right at the 3% target and within the 2-4% target range. The central bank next meets August 10 and is expected to keep rates steady at 3.0%. HungaryHungary reports May retail sales Wednesday, which are expected to rise 3.4% y/y vs. a revised 1.7% (was 2.0%) in April. The central bank also releases its minutes Wednesday. At that meeting, the bank added more stimulus via unconventional measures. Next policy meeting is July 18 and no change is expected. It then reports May IP Thursday, which is expected to rise 4.7% y/y. May trade will be reported Friday. TaiwanTaiwan reports June CPI Wednesday, which is expected to rise 0.9% y/y vs. 0.6% in May. The central bank does not have an explicit inflation target. However, low price pressures should allow it to keep rates steady at its next quarterly policy meeting in September. Taiwan then reports June trade Friday. Exports and imports are expected to rise y/y by 8.9% and 12.6%, respectively. PolandNational Bank of Poland meets Wednesday and is expected to keep rates steady at 1.5%. June CPI came in lower than expected at 1.5% y/y. This was the lowest since December, and is very close to the bottom of the 1.5-3.5% target range. Central bank officials continue to say no hikes until 2018, and the data for now supports this. ColombiaColombia reports June CPI Wednesday, which is expected to rise 4.08% y/y vs. 4.37% in May. If so, that would be the lowest since January 2015 and would be very close to the 2-4% target range. The central bank just cut rates 50 bp to 5.75% on Friday. It next meets July 21 and is expected to cut rates by another 50 bp to 5.25%. Czech RepublicCzech Republic reports May retail sales, industrial and construction output Friday. Sales are expected to rise 4.0% y/y and industrial output is expected to rise 3.3% y/y. The economy remains robust, which support the CNB’s forward guidance for the first rate hike in Q3. Next policy meeting is August 3, no change is expected then as we favor the September 27 meeting. However, much will depend on the exchange rate. |

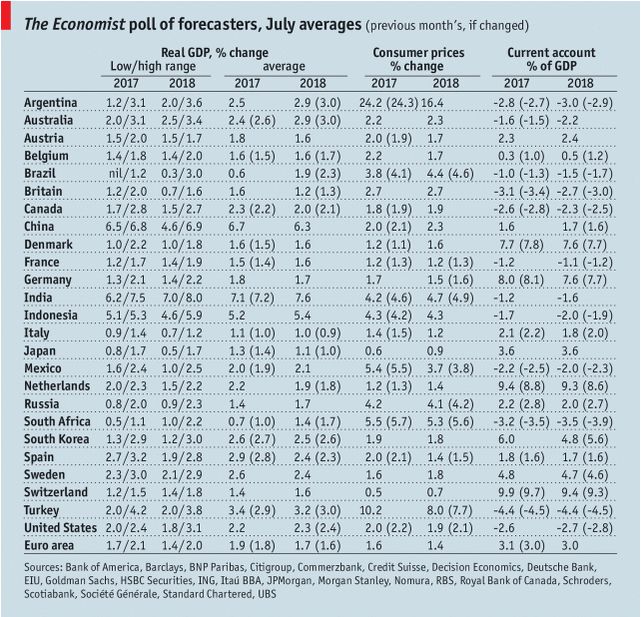

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, July 2017 Source: economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets