Stock MarketsEM FX was mixed Friday to cap off a mostly lower week. Obviously, we’re seeing a bit of a washout in EM after the hawkish FOMC. Market was overly complacent and very long EM going into the FOMC meeting. The big question is how deep this selloff gets. For the better part of this year, EM dips have been met with renewed buying. We remain cautious on EM and think that investors should avoid the high beta currencies like ZAR, TRY, BRL, MXN. |

Stock Markets Emerging Markets, June 14 Source: economist.com - Click to enlarge |

TaiwanTaiwan reports May export orders Tuesday, which are expected to rise 7.6% y/y vs. 7.4% in April. The central bank meets Thursday and is expected to keep rates steady at 1.375%. Taiwan reports May IP Friday, which is expected to rise 1.4% y/y vs. -0.6% in April. South AfricaSouth Africa reports Q1 current account data Tuesday. The deficit is expected to widen to -1.8% of GDP from -1.7% in Q4. It then reports May CPI Wednesday, which is expected to remain steady at 5.3% y/y. This would remain within the 3-6% target range. SARB next meets July 20, and rates are expected to be kept steady at 7.0%. HungaryHungary central bank meets Tuesday and is expected to keep rates steady at 0.9%. However, it may add stimulus via unconventional measures to offset recent forint strength. PolandPoland reports May industrial and construction output, PPI, and real retail sales Tuesday. Consensus y/y readings are 8.3%, 12.6%, 2.9%, and 7.6% y/y, respectively. The central bank releases its minutes Thursday. RussiaRussia reports May real retail sales Tuesday, which are expected to rise 0.5% y/y vs. flat in April. The central bank cut rates 25 bp to 9.0% on Friday, and signaled further cautious easing in H2. More important for Russian growth is the price of oil. MalaysiaMalaysia reports May CPI Wednesday, which is expected to rise 4.1% y/y vs. 4.4% in April. The central bank does not have an explicit inflation target. Next policy meeting is July 13, rates are expected to be kept steady at 3.0%. ArgentinaArgentina reports Q1 GDP Wednesday, which is expected to grow 0.2% y/y vs. -2.1% in Q4. If so, this would be the first positive reading since Q1 2016. The fundamentals are slowly improving, with CPI inflation easing to 24% y/y in May from the peak of 27.5% in April. PhilippinesPhilippines central bank meets Thursday and is expected to keep rates steady at 3.0%. CPI rose 3.1% y/y in May, close to the 3% target and well within the 2-4% target range. We see steady rates for now, but the bank has signaled a more hawkish stance if price pressures rise. BrazilBrazil central bank releases its quarterly inflation report Thursday. Brazil reports mid-June IPCA inflation Friday, which is expected to rise 3.48% y/y vs. 3.77% in mid-May. Petrobras just announced cuts to gas and diesel fuel prices, so price pressures are likely to move lower. COPOM next meets July 26, and a 75 bp cut to 9.5% is expected. MexicoMexico reports mid-June CPI Thursday, which is expected to rise 6.25% y/y vs. 6.17% in mid-May. This would be the highest rate since January 2009 and further above the 2-4% target range. Banco de Mexico meets that day and is expected to hike rates 25 bp to 7.0%. With the peso firming and inflation showing signs of topping out, this is likely to be the last hike in the cycle. SingaporeSingapore reports May CPI Friday, which is expected to rise 1.3% y/y vs. 0.4% in April. It also reports May IP that day, which is expected to rise 6.8% y/y vs. 6.7% in April. Despite firmer data, the MAS opted to keep its forward guidance intact at its April meeting, which suggests no move at the October meeting. |

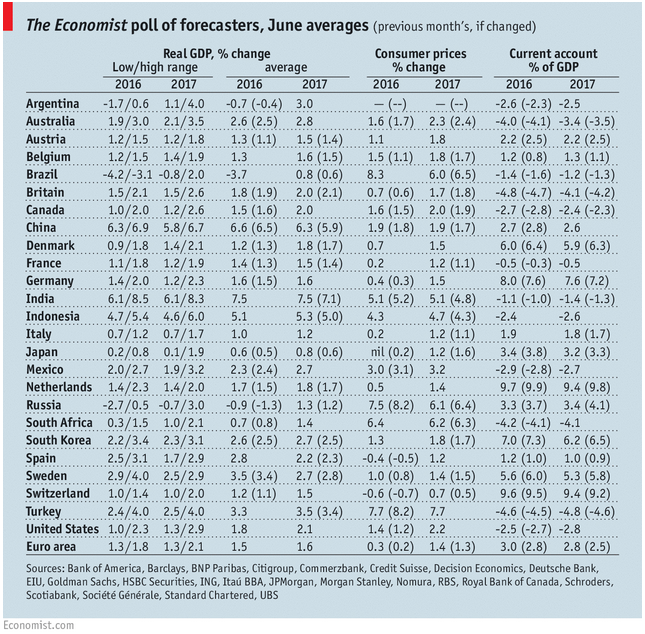

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, June 2017 Source: economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets,newslettersent