Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

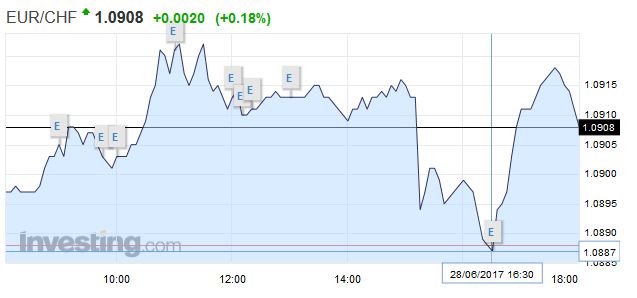

Swiss FrancThe euro is higher at 1.0908 CHF (+0.18%). |

EUR/CHF - Euro Swiss Franc, June 28(see more posts on EUR/CHF, ) - Click to enlarge |

GBP/CHFIn the past many of my clients that are not experienced within the currency markets have asked why the Swiss Franc is incredibly strong against all of the major currencies when interest rates are currently in minus territory (-0.75%). Higher interest rates tend to strengthen the currency as investors can receive higher interest on their assets. Switzerland is known as a safe haven currency which means international investors want to leave their assets (normal large amounts) within the country as they believe the value will not depreciate, even thought Banks essentially charge their clients to hold their money. The currency company I work for is based in the UK therefore I assist lots of clients that are trading GBPCHF or CHFGBP. Looking further ahead I expect the fantastic rates for buying GBP will continue and clients purchasing CHF with GBP to continue to struggle on. The pound is under severe pressure at present due to Theresa May not winning the General election by a majority and Brexit negotiations that started over 7 days ago. Theresa May’s government should be approved by the end of the week which could lead to a period of sterling strength, however I wouldn’t be surprised to see further pressure mount on the Prime Minister for her resignation in the upcoming months which you would think would lead to further sterling weakness. As for Brexit negotiations it is very difficult to predict when a deal will be struck or if a deal will be struck. However this story has the potential to have a substantial impact on exchange rates therefore receiving regular updates when converting pounds and Swiss franc’s will help you to achieve better rates which will in turn make you a saving. |

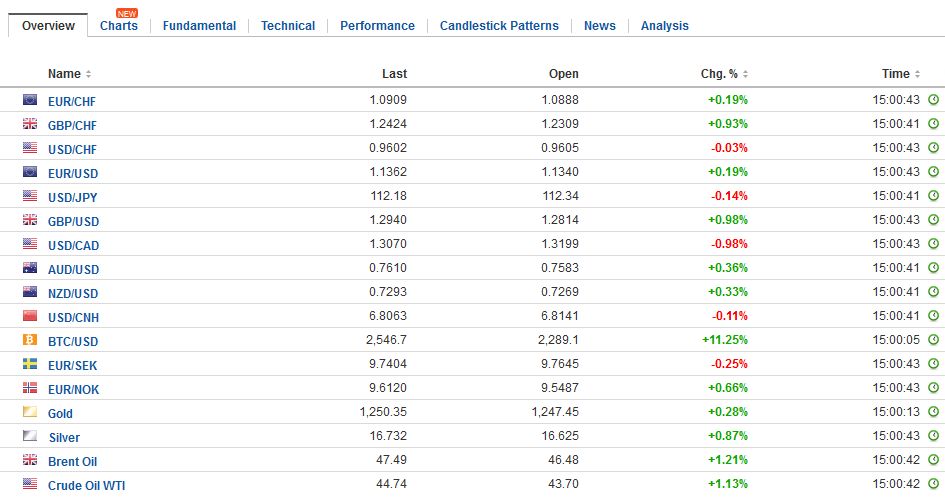

GBP/CHF - British Pound Swiss Franc, June 28(see more posts on GBP/CHF, ) - Click to enlarge |

FX RatesSounding confident, ECB President Draghi seemed prepared to reduce the asset purchases, and this overshadowed his explicit recognition that substantial accommodation is still necessary. This is very much in line with what many, including ourselves, anticipate: At the September ECB meeting, an extension of the asset purchases into the first part of next year, coupled with a reduction in the amounts being purchased. The yield on the German 10-year Bund finished last week near 25 bp. Today it briefly traded as high as 40 bp. Peripheral European bonds got crushed yesterday, but seemingly, the quest for yield brought in buyers today, and Spain, Italy and Portuguese yields are lower today, while the core is firmer. The Canadian dollar is the strongest of the major currencies today, gaining almost 0.5% against the US dollar. It is trading at its best level in four months and is approaching congestion near CAD1.3100. The driving force continues to be a reassessment of the trajectory of policy. Bank of Canada Governor Poloz noted that interest rates have down their job and are extraordinarily low. The Bank of Canada meets July 12. |

FX Daily Rates, June 28 - Click to enlarge |

| The Canadian dollar is resisting the pull of oil prices. The four-day rally is at risk today, following news late yesterday from API that showed an 850k barrel build in oil inventories, and news that OPEC output appears to be increasing. Initial support is seen near $43.50 basis the August light sweet crude futures contract.

We also suspect that many observers exaggerate the impact on yields of central bank buying. Numerous studies find that more important channel is the signaling effect, not the purchasing. The reason the price of money is low, we suggest, is not simply because the ECB and BOJ are buying bonds, but also, and more importantly, the supply of capital outstrips its demand. Capital is subject to the same laws of supply and demand as other commodities. Low inflation, low growth, excess capacity in numerous industries, all serve to dampen the price of capital. Also, consider other elements of the news stream. The French cabinet is expected to approve Macon’s new labor code, which is hoped to be approved by parliament in September. Consensus thinking is that the rigidities in the labor market are undermining French competitiveness. Macron proposes limiting severance pay and the costs of dismissing employees, simplify worker representation, and make companies, not industries the key bargaining unit. There are two risks here. First, that Macron does not get what he wants. After all, he is not the first French President to push for labor reforms. Sarkozy and Hollande both tried, but unions and others successfully resisted. Second, Macron can get what he wants but finds that the reforms were oversold and that the key to French competitive is not so much about cutting labor costs, but in the flexibility of capital; incentives for entrepreneurship, innovation, and incentives for profit-seeking instead of rent-seeking behavior. |

FX Performance, June 28 - Click to enlarge |

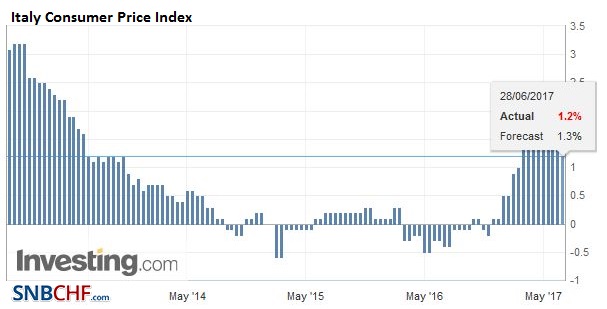

Italy |

Italy Consumer Price Index (CPI) YoY, June 2017(see more posts on Italy Consumer Price Index, ) Source: Investing.com - Click to enlarge |

United States

|

U.S. Crude Oil Inventories, May 2017(see more posts on U.S. Crude Oil Inventories, ) Source: Investing.com - Click to enlarge |

At the same time, the news stream from the US has deteriorated. The delay in the healthcare vote in the Senate sours the outlook, many suspect, of the other parts of the Republican agenda of tax reform and infrastructure spending. The Republican strategy of bypassing the Democrats, which some suggest is an exercise in realpolitik and the power of the majority, appears to have the same problem in the Senate as it did in the House of Representative: namely that the Republican Party, like all modern parties, is a coalition, not a homogeneous group. What appears to the moderates alienates the conservatives.

In this vein, the IMF revised down its growth forecasts for the US economy this year and next. Like the market, it is skeptical about the US ability to enact tax reform and infrastructure spending. It is skeptical that the Trump Administration will be able to boost growth. The market is skeptical about the Fed’s ability to hike rates again this year. Interpolating from the OIS, the market appears to have discounted a 40% chance of a hike before the end of the year. Moreover, looking at the curve, the odds of a hike (to bring Fed funds to 1.25-1.50%) peak in March next year (~41%) and then ease.

Yellen’s claim that there may not be another crisis in our lives was ridiculed. It may seem overly optimistic, but she is not talking about a cyclical downturn as in a recession, but a crisis of the magnitude of the Great Depression or the Great Financial Crisis. There seem to be 40-50 years between such crisis since at least the middle of the 19th century, though, of course, some cycle work (see Kondratieff Wave) would project it much further into the past).

The US economic diary includes the advance report on merchandise trade (look for a slightly smaller deficit), wholesale and retail inventories (for GDP calculation, look for a small boost), and pending home sales ( an improvement over April likely). There continues to be headline risk from the ECB conference that ends today. Draghi, Carney, Kuroda, and Bernanke are on tap. Investors also will continue to digest the seeming campaign by the Fed’s leadership, Yellen, Fischer, and Dudley, as well as some other Fed officials, expressing concern over either the US financial conditions or the elevated stock market.

Eurozone

Eurozone money supply and lending figures were published. M3 growth improved to a 5% pace. It has averaged 5% over the past six months. Lending to non-financial businesses was steady rising 1.6% year-over-year, roughly in line with GDP growth. Lending to households improved a 2.7% pace from 2.6%.

Still, we suspect the market is getting ahead of itself. The key to ECB policy is not growth but inflation. Italy is the first to report the flash June figures. The EMU figure will be released at the end of the week. Italy’s harmonized measure of CPI was weaker than expected. It fell 0.2% for the second consecutive month, which brings the year-over-year figure to 1.2%. The lowest since January.

Also, even if market sentiment looks at the money supply growth and credit expansion through rose tinted glasses, the sharp decline in the credit impulse–the second difference of the stock of credit. It was especially weak in Italy, and this may have been a reflection of its simmering banking woes that came to a head in recent days.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CAD,$EUR,$TLT,ECB,EUR/CHF,FX Daily,gbp-chf,Italy Consumer Price Index,newslettersent,U.S. Crude Oil Inventories