Stock MarketsEM FX closed last week on a mixed note, with markets struggling to find a compelling investment theme. The US jobs data this week could provide some more clarity on Fed policy. We still think markets are still underestimating political risk in the big EM countries, including Brazil (Moody’s outlook moved to negative), Mexico (election in state of Mexico), South Africa (ANC debates Zuma’s fate), and Turkey (ongoing crackdown on opposition). |

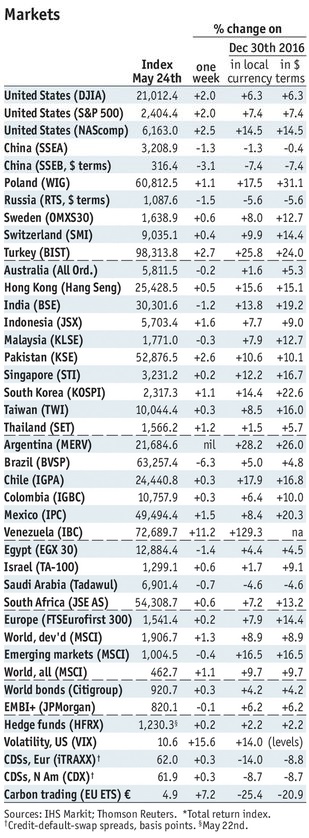

Stock Markets Emerging Markets, May 24 Source: economist.com - Click to enlarge |

IsraelBank of Israel meets Monday and is expected to keep rates steady at 0.10%. CPI rose 0.7% y/y in April, below the 1-3% target range. With the shekel remaining firm, the central bank is likely to keep rates steady whilst continuing to buy USD/ILS. South AfricaSouth Africa reports April money and private sector credit data Tuesday. Both are expected to pick up modestly from March. It reports April trade data Wednesday. Q1 unemployment will be reported Thursday, and is expected at 27.0% vs. 26.5% in Q4. SARB kept rates steady last week. Next policy meeting is July 20. If current trends persist, we think it will give a stronger signal that it could cut rates in H2. Results of the ANC meeting are not yet known as of this writing. ChileChile reports April IP Tuesday. Central bank releases its minutes Friday, while April retail sales will also be reported. The economy remains weak while price pressures remain low. While the bank signaled that the easing cycle is over for now, we do not see tightening until 2018. Next policy meeting is June 15, and rates are likely to remain steady at 2.5%. KoreaKorea reports April IP Wednesday, which is expected to rise 5.5% y/y vs. 3.0% in March. The economy remains sluggish, as the BOK kept rates steady last week. Korea reports May CPI and trade Thursday. Inflation is expected to remain steady at 1.9% y/y, just under the 2% target. Exports and imports are expected to rise y/y by 16.2% and 15.5%, respectively. ChinaChina reports official PMI readings for May Wednesday. Manufacturing PMI is expected to tick down to 51.0 from 51.2 in April. Caixin reports its China manufacturing PMI for May Thursday, which is expected to tick down to 50.2 from 50.3 in April. We wouldn’t make too much fuss about last week’s reports that PBOC will exert more influence on the daily CNY fix. TurkeyTurkey reports April trade Wednesday. The deficit is expected at -$4.9 bln, which would boost the 12-month total slightly to -$56.9 bln. The external accounts are not a problem, as exports recover and imports are restrained by sluggish growth and consumption. IndiaIndia reports Q1 GDP Wednesday. Growth is expected at 7.1% y/y vs. 7.0% in Q4. It turns out that the controversial decision to demonetize last year had little impact on the economy. Price pressures are picking up, so we expect the RBI to continue tightening at a modest pace. Next policy meeting is June 7, and no change is expected after it hiked its reverse repo rate unexpectedly at its last meeting on April 6. PolandPoland reports May CPI Wednesday, which is expected to rise 2.1% y/y vs. 2.0% in April. This would still be in the bottom half of the 1.5-3.5% target range. Central bank minutes will be released Thursday. The central bank continues to keep its forward guidance for the first hike in 2018. Next policy meeting is June 7, and rates are expected to be kept steady at 1.5%. MexicoBanco de Mexico releases its quarterly inflation report Wednesday. This will be followed by its minutes Thursday. At that meeting, the central bank surprised many in the markets by hiking 25 bp to 6.75%. Next meeting is June 22, and another hike then seems likely if the Fed hikes on June 14. The state of Mexico holds its gubernatorial election on Sunday, and polls show the race to close to call. That said, the PRI has held the post for over 80 years, and yet this stronghold may go to AMLO’s Morena party. COPOM meets Wednesday and is expected to cut rates 100 bp to 10.25%. However, a small minority expect a 75 bp cut. IPCA inflation was 4.1% y/y in April, in the bottom half of the 2.5-6.5% target range. However, political uncertainty and delays to fiscal reforms could lead COPOM to cut less aggressively. Moody’s cut the outlook on its Ba2 rating from stable to negative Friday, citing political risks to the reform agenda. Brazil reports Q1 GDP and May trade Thursday. The economy is expected to contract -0.1% y/y but rise 1.25 q/q. It then reports April IP Friday. ThailandThailand reports May CPI Thursday, which is expected to rise 0.25% y/y vs. 0.38% in April. This would be well below the 1-4% target range. With the economy sluggish and price pressures low, the BOT is likely to keep rates on hold for now. Next policy meeting is July 5, and rates are likely to be kept steady at 1.5%. PeruPeru reports May CPI Thursday, which rose 3.69% y/y in April. This was above the 1-3% target range, but that didn’t stop the central bank from starting the easing cycle. Further easing is likely to boost the weak economy. Next policy meeting is June 8, and another 25 bp cut to 3.75% is likely. IndonesiaIndonesia reports May CPI Friday, which is expected to rise 4.3% y/y vs. 4.2% in April. This would be the highest since March 2016 and still in the top half of the 3-5% target range. Price pressures are rising and so the bank is likely to keep rates on hold for now. Next policy meeting is June 15, no change in rates is expected. |

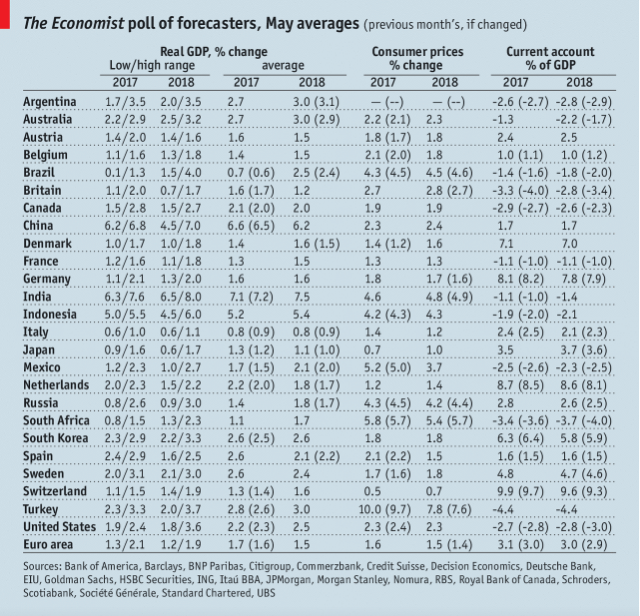

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, May 2017 Source: economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets,newslettersent,win-thin