Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The week ahead is the busiest week of the first quarter. It sees four major central meetings, including the Federal Reserve which is likely to raise rates for the second time in four months. The Dutch hold the first European election of the year, and the populist-nationalist party remains in contention for the top slot. The week concludes with the G20 meeting, the first that the Trump Administration’s presence will be felt.

Since the events are well known, we may be able to add the most value by sharing our expectation of the outcomes and significance for the capital markets. The immediate backdrop is solid US jobs growth, heightened expectations of a hike, firm eurozone data, stabilization of the Chinese economy, capex and export-led expansion of the Japanese economy, and a pullback in commodity prices, including oil, after a run-up that carried over from last year. Interest rates are mostly moving higher, and equity markets have been trading heavier after a strong start to the year.

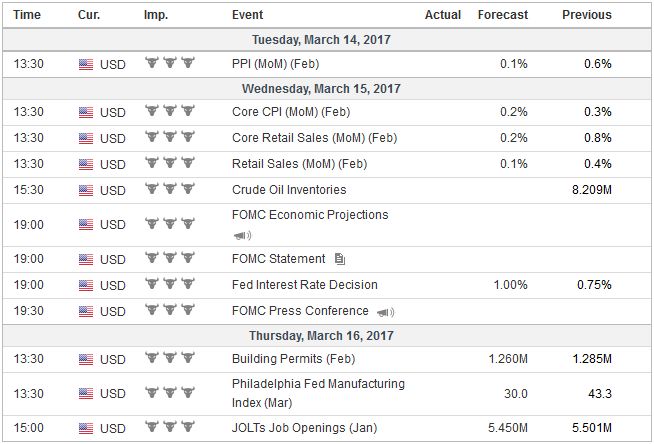

FOMC meeting: The combination of data and official comments spurred a sharp swing in expectations toward a rate hike on March 15. There is no reason to think that the Fed will not deliver. This is taken as given now, and investors will be more interested in the updated forecasts (dot plot) and the context Yellen provides at her press conference. While the last set of forecasts showed the median expectation (not a promise or commitment) that three rate hikes would be appropriate this year, the market is unconvinced. It is discounting about a one in three chance that the Fed will deliver three hikes this year. We suspect the market is underestimating the hawkishness of many regional presidents, some of whom will be emboldened by the resilience of the US economy as they have argued. To the extent that the forecasts are changed, we expect more dots to be raised. We see the confidence of the Fed officials, seen in subtle shifts in their word cues, as indicative a different reaction function. Previously officials needed confirmation that the recovery was resilient. It has become convinced. Now it is looking for appropriate opportunities. A hawkish hike, as opposed to the past two dovish hikes, could support the dollar and spur bearish curve flattening (short-term rates rise more than long-term rates). If the Fed statement, forecasts, and press conference fail to convince the market that a follow-up hike in June ought not to be ruled out, the dollar would likely sell-off, as stale longs move to the sidelines. A rally in bonds would likely weigh on the dollar against the yen. Rising yields are seen helping banks and other financial institutions. A fall in yields may see some investors shifts into other sectors.

Dutch Election: Judging by the developments in the credit markets, investors are not as worried about the prospect of the populist-nationalist forces winning that the media. The fragmented nature of Dutch political parties requires coalitions, and this serves as the ultimate check on the Freedom Party and Wilders’ agenda. It will take some time to sort out the results and form a new government, which may entail the inclusion of four or five political parties. The hubris of small differences may make it difficult to form a government in the first place or lead to a fragile government. A stronger than expected showing for the Freedom Party (PVV), of say 26 seats (150-seat chamber) could elicit a market reaction, but in lieu of this, the market impact is likely to be minor. The generally expected outcome that a new government excludes the PVV might encourage investors and observers to question the main narrative that populism-nationalism is sweeping across Europe and the US. To the extent that the populist-nationalist agenda entered the governments in the US and UK was when the main center-right party adopted. In Europe, the center-right parties are running against the populist-nationalist parties.

G20 finance ministers and central banks meeting: No fresh initiatives can be expected. The outlook for the global economy has improved marginally. The most important change since the last meeting is the inclusion of the new US Treasury Secretary. Many partisans fail to appreciate that the despite that there are two distinct economic wings of the Trump Administration. There is protectionist, unilateralist (most definitely not isolationist), American-First wing. It is facing off against a more free-trade wing that accepts the basic premises of the liberal global world order of the post-WWII era. The G20 statement, and how the final version evolved from the preliminary leaked version may occupy analysts and journalists, but investors will likely file it with the “good to know” rather than an inducement to act.

GermanyBefore the G20 meeting, there are two US-German meetings that will draw attention. German Chancellor Merkel will meet Trump in Washington, and Treasury Secretary Mnuchin will meet Schaeuble, his counterpart in Germany. Over the past year or two, the US Treasury Department’s semi-annual reports on the international economy and foreign exchange market have become more critical of Germany. In the early days of the Trump Administration the line has been pushed more forcefully. There has been a striking juxtaposition of roles. Merkel has defended the liberal global order against the threats to it by American protectionism. Traditionally, Americans often saw Russia posing a greater threat than many Germans. Now Merkel is trying to keep sanctions in place of the seemingly more accommodative Americans. Mnuchin appears to be part of the free-trade wing of the Trump Administration and will likely get on well with Schaeuble. They can commiserate over the soft money policies of the ECB and the bureaucrats in Brussels. The market impact may be in inverse proportion to the news coverage. The more talk, the less was done. |

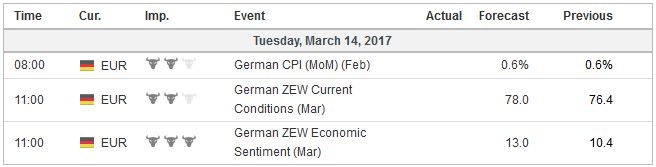

Economic Events: Germany, Week March 13 - Click to enlarge |

EurozoneECB:The ECB does not meet, but the market attention has shifted toward the inevitable exit of the unorthodox policies. Reading between the lines and attentive to Draghi’s press conference, it seems clear that the ECB is past peak QE. What has captured the market’s attention is the sequencing of the exit. Even before the leaked reports claiming that the possibility of lifting the deposit rate was discussed, we noted: “With the negative deposit rate of 40 bp, there is some thought that the ECB could reduce the negativity before completely ending is asset purchase program. But this does not appear particularly likely in the next several months, and, moreover, it may look a bit different if inflation peaks, as we expect, in Q2.” The Federal Reserve waited for a “considerable period” after the end of its asset purchases before raising its Fed funds target. However, negative deposit rates add a complication. The increase in market rates may offer an opportunity to do so with minimal risks. Norges Bank meeting: The market had felt comfortable with ideas that Norway’s central bank would leave the deposit rate at 0.5% when it meets on March 16. However, before the weekend, Norway reported a soft February CPI report, and it captured some imaginations. It accelerated the krone’s slide. The euro rose 2.65% against the krone last week, the most in over a year. It was pushing on an open door as the euro had already begun rallying against Nokkie and rose 1.1% against it the previous week, which at the time was the most since last August. The 0.4% rise in February consumer prices was the largest increase since last September, but it was only half was what had been anticipated. The year-over-year rate fell to 2.5% from 2.8%, and the core rate, which excludes energy and tax changes, fell to 1.6% from 2.1%. The sell-off in the krone, not just against the euro but on a trade-weighted basis in the last couple of weeks takes pressure off the central bank to do something it does not really want to do. |

Economic Events: Eurozone, Week March 13 - Click to enlarge |

JapanBank of Japan meeting: No new initiatives are expected to be announced. Governor Kuroda made a big splash when announcing new measures, but he has more quietly modified the program so that the BOJ’s balance sheet is growing slower and slightly fewer funds at the BOJ are burdened with a penalty or negative rate. The market has hardly talked about Kuroda’s soft exit. Although there have been periods that required action, the 10-year yield has been mostly stable as global interest rates have risen. The key driver of dollar-yen are the interest rate differentials (US-Japan 10-year, dictated now by the US side) and equity markets. Japan’s policy of relatively loose fiscal and monetary policy is a given and not a new factor for investors. |

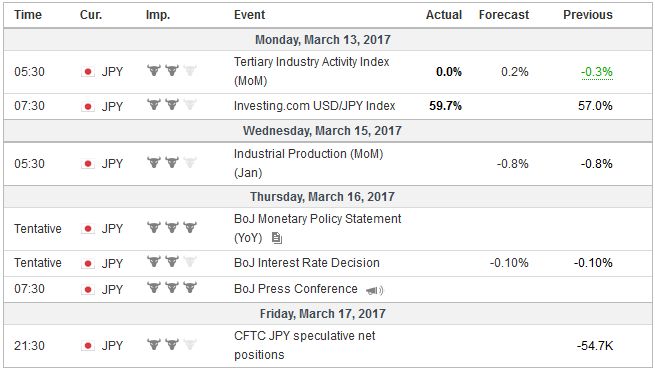

Economic Events: Japan, Week March 13 - Click to enlarge |

United KingdomBank of England meeting:This meeting, like the BOJ meeting, is likely to pass without much fanfare. Under past governors, when the Bank of England didn’t do anything they wouldn’t say anything. That was then. Now, in the new era of greater transparency and enhanced communication, the BOE will hold a press conference and release the minutes simultaneously. The minutes themselves are a channel of communication and not simply an objective record of the meeting. The two key drivers of sterling presently are Brexit and interest rate differentials. The discount to the US is near record levels. The Brexit amendments return to the House of Commons this week. The Tory majority should be sufficient to defeat them. A formal trigger is still seen as most likely before the end of the month. Two other Brexit-related issues have arisen: A second Scottish referendum and maybe an early UK election. The former is seen as sterling negative. The latter has been denied by 10 Downing Street, but the political logic, with Labour continuing to falter, is not deterred by the more complicated legislative process that is required. The Tories themselves voting no confidence in its own government to topple it trigger the new elections. |

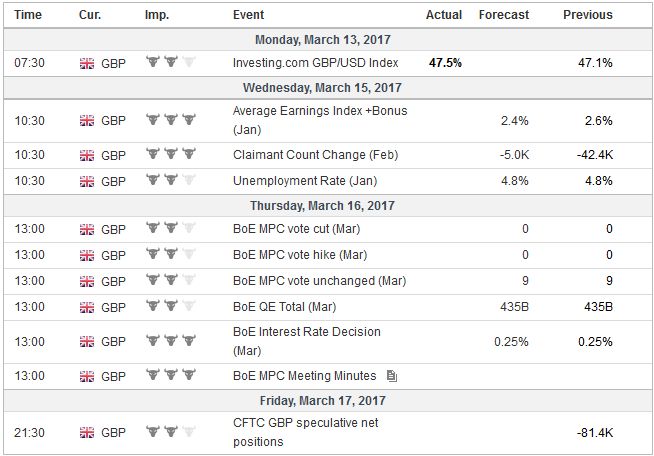

Economic Events: United Kingdom, Week March 13 - Click to enlarge |

SwitzerlandSwiss National Bank meeting: The euro rallied against the Swiss franc at the end of last week and reached its best level in three months. The increase in Swiss sight deposits seems to reflect that the SNB had been actively defending the CHF1.0650 area where the euro chiseled out a bottom since the end of January. Separately, we note the convergence of short-term German and Swiss rates. Consider that over the past year, the Germany two-year yield has fallen 38 bp tominus85, while the Swiss two-year yield has risen 16 bp tominus95. Despite the low level of anxiety over the Dutch election and the ECB exit talk, the German two-year yield was flat to slightly lower last week. The comparable Swiss yield was up nearly seven basis points. Can the Swiss begin normalizing policy toward the end of the year, maybe after the German elections, or is it a 2018 story? |

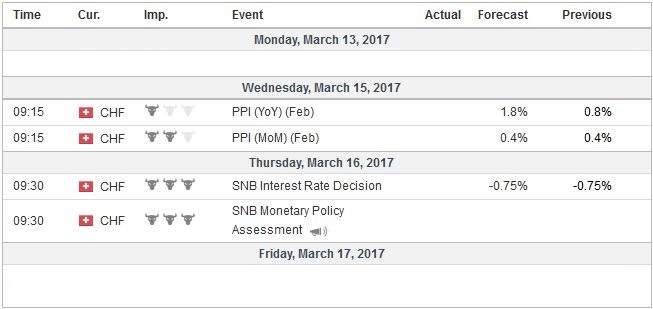

Economic Events: Switzerland, Week March 13 - Click to enlarge |

United StatesUS debt ceiling: The forbearance of the debt ceiling that was agreed at the end of 2015, to effectively kick the can past the election, ends on March 15. It is a political ritual in the United States in which the legislative branch often seeks concessions to grant the executive branch the authorization to pay for what has already been purchased/borrowed. The looming expiration is already impacting the T-bill market as the government has already begun preparing and investors have also responded accordingly. However, the larger market impact is minimal. There are several months before truly difficult decisions will have to be made and there are several opportunities to raise the debt ceiling. Even though one party has a majority of both chambers of the legislative branch and the executive branch, the issue is also illustrative of another split in the government. On one side is the seize-the-moment strategy that sees this as an opportunity to roll back the government’s role in the economy and society. On the other side are those that ultimately are more opposed to the direction of previous policies not the legitimacy of the policies. In the campaign, the candidate Trump briefly suggested the possibility of renegotiating US debt, but this line has not been pursued and, currently, does not seem relevant. |

Economic Events: United States, Week March 13 - Click to enlarge |

Tags: #GBP,#USD,$EUR,$JPY,newslettersent,Norwegian Krone