Stock MarketsEM ended the week on a firm note, with markets digesting what they perceived as a dovish Fed bias. We disagree, and continue to believe that markets are underestimating the Fed’s capacity to tighten this year. EM FX could continue gaining some traction if the dollar correction continues, but we think US interest rates will ultimately move higher and put pressure on EM once again. |

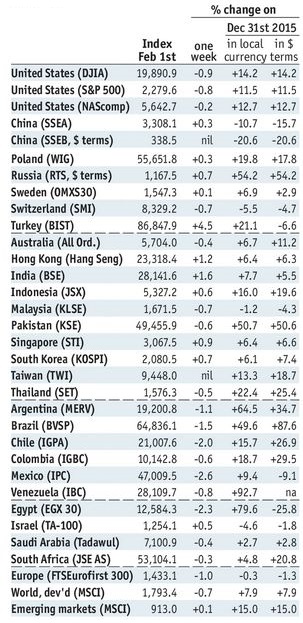

Stock Markets Emerging Markets February 06 Source: economist.com - Click to enlarge |

ChinaCaixin reports China January composite and services PMI readings Monday. Last week, official services PMI reading ticked higher to 54.6, so there are small upside risks to the Caixin data. Note, however, that manufacturing PMI readings fell from December so the overall economic outlook is mixed. January trade will be reported Friday, with export seen rising 3% y/y and imports 9.6% y/y. Czech RepublicCzech Republic reports December retail sales Monday, which are expected to rise 6.2% y/y vs. 8.6% in November. It then reports December trade, industrial and construction output Tuesday. January CPI will be reported Friday, and is expected to rise 2.1% y/y vs. 2.0% in December. PhilippinesThe Philippines reports January CPI Tuesday, which is expected to rise 2.8% y/y vs. 2.6% in December. Last week, we saw higher than expected CPI prints for Korea, Taiwan, Thailand, and Indonesia and so we see upside risks for the Philippines. The central bank then meets Thursday and is expected to keep rates steady at 3.0%. December trade will be reported Friday, with exports seen rising 3.5% y/y and imports 10% y/y. HungaryHungary reports December IP Tuesday, which is expected to rise 0.4% y/y vs. 0.6% in November. Central bank minutes will be released Wednesday. December trade will be reported Thursday. The economy remains robust, and we think rising price pressures could limit or even prevent further easing at the March meeting. That is when the central bank will decide if it will make another adjustment to its borrowing facility. TaiwanTaiwan reports January trade Tuesday. Exports are expected to rise 10.0% y/y and imports by 12.7% y/y. January CPI will be reported Wednesday, which is expected to rise 2.0% y/y vs. 1.7% in December. The central bank does not have an explicit inflation target. However, rising price pressures should push it into a more hawkish stance as the year progresses. ChileChile reports January trade Tuesday. It then reports January CPI Wednesday, which is expected to rise 2.5% y/y vs. 2.7% in December. This is moving towards the bottom of the 2-4% target range and should keep the central bank in dovish mode. Minutes from the last central bank meeting showed that a 50 bp cut was discussed before they settled on a 25 bp one. Next policy meeting is February 14, and another 25 bp cut then seems likely. MalaysiaMalaysia reports December trade Wednesday. December IP will be reported Friday. The economy remains fairly robust, while price pressures are rising. While we do not think a rate hike is imminent, the central bank is likely to tilt more hawkish and so further easing is very unlikely. ThailandBank of Thailand meets Wednesday and is expected to keep rates steady at 1.5%. January CPI rose 1.55% y/y, the highest since September 2014. With low base effects from last year, we believe inflation will move toward the upper end of the 1.0-4.0% target range over the course of this year. Towards mid-year, the BOT will likely start thinking about rate hikes. TurkeyTurkey reports December IP Wednesday, which is expected to rise 2.0% y/y vs. 2.7% in November. The economy remains sluggish even as inflation surged to 9.22% y/y in January vs. 8.6% consensus and 8.53% in December. This is the highest since January 2016, and moved further above the 3-7% target range. Next policy meeting is March 16. While the bank should hike the benchmark rates, it may keep relying on the current backdoor tightening. IndiaReserve Bank of India meets Wednesday and is expected to cut rates 25 bp. December IP will be reported Friday, which is expected to rise 1.4% y/y vs. 5.7% in November. The economy has softened, due partially to the demonetization seen back in November. CPI rose 3.4% y/y in December, which is in the bottom half of the 2-6% target range. January CPI will be released February 13 and is expected to ease further to 3.2%. BrazilBrazil reports January IPCA inflation Wednesday, which is expected to rise 5.44% y/y vs. 6.29% in December. Is so, then this would be the lowest rate since September 2012 and supports further easing. Next COPOM meeting isFebruary 22, and another 75 bp cut to 12.25% is likely. So far, the economy has not responded much to previous easing. PolandNational Bank of Poland meets Wednesday and is expected to keep rates steady at 1.5%. Inflation pressures are rising, and could force the NBP to hike in 2017, before its plan to start in 2018. The economy remains robust, while CPI is expected to pick up from 0.8% y/y in December to 1.7% in January. If so, then this would be the highest rate since January 2013. South AfricaSouth Africa reports December manufacturing production Thursday, which is expected at -0.4% y/y vs. +1.9% in November. The economy remains sluggish, even as price pressures remain elevated. CPI rose 6.8% y/y in December, the highest since February 2016 and further above the 3-6% target range. Next SARB meeting is March 30, and it is unlikely to hike rates then due to the weak economy. MexicoMexico reports January CPI Thursday, which is expected to rise 4.72% y/y vs. 3.36% in December. If so, this would be the highest since September 2012 and moves further above the 2-4% target range. Banco de Mexico meets later that day and is expected to hike rates 50 bp to 6.25%. Mexico then reports December IP Friday, which is expected flat y/y vs. 1.3% in November. PeruPeruvian central bank meets Thursday and is expected to keep rates steady at 4.25%. CPI rose 3.1% y/y in January, the lowest since August but still above the 1-3% target range. Chile and Colombia have already started easing, and Peru is likely to join them in H1 if disinflation continues. |

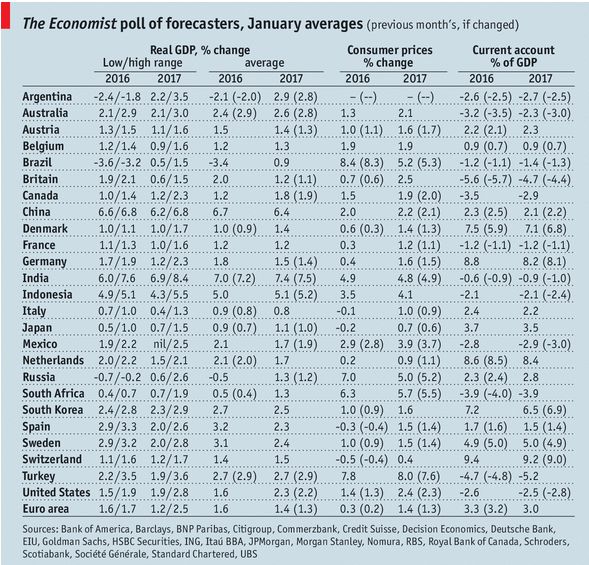

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, January 2017 Source: Economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets,newslettersent