SummaryEM FX ended the week on a soft note, as higher US rates continue to take a toll. EM policymakers are getting more concerned about currency weakness, with Brazil, Malaysia, Korea, India, and Indonesia all taking action to help support their currencies. If the EM sell-off continues as we expect, more EM central banks are likely to act to slow the moves. Several EM central banks (Hungary, Malaysia, South Africa, Turkey, and Colombia) meet. Most are struggling with sluggish growth, but FX weakness is likely to keep all of them on hold for now. We do not think individual country themes will be very important to investors in this current environment. |

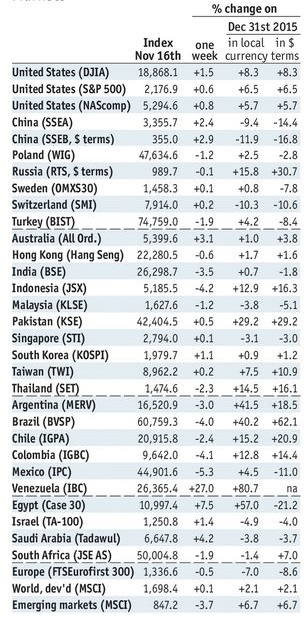

Stock Markets Emerging Markets November 26 Source: economist.com - Click to enlarge |

KoreaKorea reports trade data for the first 20 days of November on Monday. Both exports and imports continue to contract. While the external accounts have been worsening a bit in recent months, the current account surplus is still expected to end the year at around 8% of GDP. Yet the economy remains weak even as political tensions rise. ThailandThailand reports Q3 GDP Monday. Growth is expected to slow to 3.3% from 3.5% in Q2. For now, the central bank is likely to remain on hold, but low inflation should allow for easing next year if the economy slows further. Next policy meeting is December 21, no change seen then. TaiwanTaiwan reports October export orders Monday, which are expected to rise 3.7% y/y vs. 3.9% in September. It then reports October IP Wednesday, which is expected to rise 5.5% y/y vs. 5.0% in September. Taiwan data may be getting a bump from a stronger mainland economy. No action is expected at the December policy meeting. However, the central bank may resume easing in 2017 if growth remains sluggish. PolandPoland reports October industrial and construction output, retail sales, and PPI Monday. The economy is showing some signs of slowing, which led several central bankers last week to start talking about potential rate cuts. Next policy meeting is December 7, but this is likely to soon for a cut. Easing seems likely to be a 2017 story. BrazilBrazil reports October current account and FDI Tuesday. It then reports mid-November IPCA inflation Wednesday, which is expected to rise 7.63% y/y vs. 8.27% in mid-October. While the central bank has started the easing cycle, recent BRL weakness is likely to keep it very cautious. Next policy meeting is November 30, and another 25 bp cut to 13.75% seems likely. HungaryHungary’s central bank meets Tuesday and is expected to keep rates steady at 0.9%. The bank has signaled steady rates for now, but has suggested that unconventional measures may be used if needed. Measures already taken have pushed yields to record lows (0.47% for 12-month T-bills). SingaporeSingapore reports October CPI Wednesday, which is expected to remain steady at -0.2% y/y. It then reports October IP Friday, which is expected to rise 0.5% y/y vs. 6.7% in September. The economy remains weak, and so we cannot rule out another easing move next year if growth remains slow. MalaysiaBank Negara Malaysia meets Wednesday and is expected to keep rates steady at 3.0%. Malaysia reports October CPI Friday, which is expected to remain steady at 1.5% y/y. While the central bank has no explicit inflation target, low inflation should allow the bank to ease again if needed. For now, the weak ringgit is likely to prevent such a move near-term. South AfricaSouth Africa reports October CPI Wednesday, which is expected to rise 6.3% y/y vs. 6.1% in September. SARB then meets Thursday and is expected to keep rates steady at 7.0%. Inflation remains above the 3-6% target range, and recent ZAR weakness is likely to keep the central bank cautious. We see no easing until well into 2017, if at all. Much depends on the rand. TurkeyTurkey’s central bank meets Thursday and is expected to keep all rates steady. A small handful of analysts are looking for a rate hike. While officials are clearly getting concerned about lira weakness, there’s not much they can do in terms of FX intervention or rate hikes. Erdogan seems dead set against rate hikes, as the economy remains soft. MexicoMexico reports mid-November CPI Thursday, which is expected to rise 3.14% y/y vs. 3.09% in mid-October. Banco de Mexico signaled that a December hike is possible after it hiked 50 bp last week. It reports October trade and Q3 current account data Friday. The current account gap is seen at around -3% of GDP in both 2016 and 2017, before narrowing to -2.5% in 2018. ColombiaColombia’s central bank meets Friday and is expected to keep rates steady at 7.75%. Earlier in the day, Colombia reports Q3 GDP. Growth is expected to slow to 1.7% y/y vs. 2.0% in Q2. For the full year, growth is seen at 2.1%, but the risks are to the downside. Inflation is falling, but remains above the 2-4% target range and so easing is likely to be a 2017 story. |

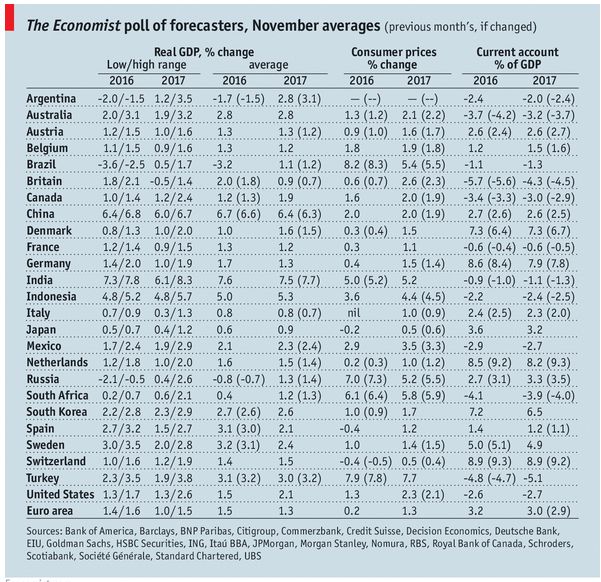

GDP, Consumer Inflation and Current Accounts Source: Economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets,newslettersent