Summary

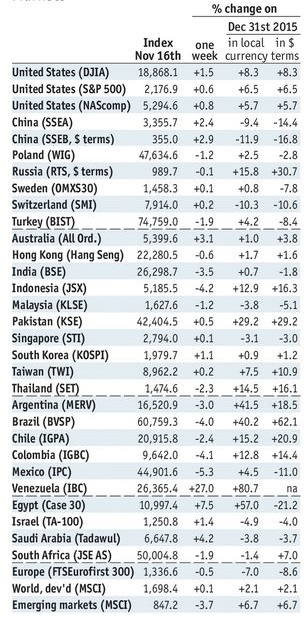

Stock MarketsIn the EM equity space as measured by MSCI, Poland (+4.0%), Russia (+3.3%), and Thailand (+2.0%) have outperformed this week, while Indonesia (-2.6%), the Philippines (-2.1%), and Turkey (-1.7%) have underperformed. To put this in better context, MSCI EM rose 1.4% this week while MSCI DM rose 1.3%. In the EM local currency bond space, India (10-year yield -20 bp), Hungary (-18 bp), and Poland (-15 bp) have outperformed this week, while the Philippines (10-year yield +51 bp), Indonesia (+49 bp), and Turkey (+17 bp) have underperformed. To put this in better context, the 10-year UST yield rose 1 bp this week to 2.37%. In the EM FX space, ZAR (+2.2% vs. USD), PLN (+0.6% vs. EUR), and PKR (+0.6% vs. USD) have outperformed this week, while EGP (-9.3% vs. USD), TRY (-2.3% vs. USD), and BRL (-1.1% vs. USD) have underperformed. |

Stock Markets Emerging Markets November 26 Source: economist.com - Click to enlarge |

PhilippinePhilippine President Duterte will reportedly ask central bank Governor Tetangco to stay on for a third term. The government will have to amend laws to allow this. Finance Secretary Dominguez confirmed that he had been authorized by Duterte to ask Tetangco to stay for another term after his second term ends July 2017. This would be a very good move and may be the first steps in regaining investor confidence. South AfricaSouth Africa’s government has proposed a national minimum wage. The country’s biggest labor union called the proposed monthly minimum wage of ZAR3500 ($246) “an insult.” On the other hand, local firms will likely complain about higher labor costs. Unemployment was just reported at a higher than expected 27.1% in Q3, and so it’s not surprising that the government is trying to address tensions in the labor market. Fitch moved the outlook on South Africa’s BBB- from stable to negative. This was long overdue, and supports our long-held view that the country will lose investment grade rating from at least one agency soon. Both S&P (BBB-) and Moody’s (Baa2) have negative outlooks too. TurkeyTurkey’s central bank surprised markets with a 50 bp hike in its benchmark repo rate to 8.0%. A small handful looked for tightening, but most analysts saw no change. The bank noted that “Exchange rate movements due to recently heightened global uncertainty and volatility pose upside risks on the inflation outlook.” Yet the lira failed to hold on to early gains, ending the day down to record new all-time lows. Tightening was certainly warranted, but it seems to be too little too late. BrazilPolitical risk in Brazil is rising as President Temer’s top aide was implicated in an influence peddling scandal. Government Secretary Lima resigned after former Culture Minister Calero claimed that he was pressured into authorizing a construction project that Lima had financial interest in. Temer may also be directly linked, as press reports existence of recordings of conversations between the president and Calero. |

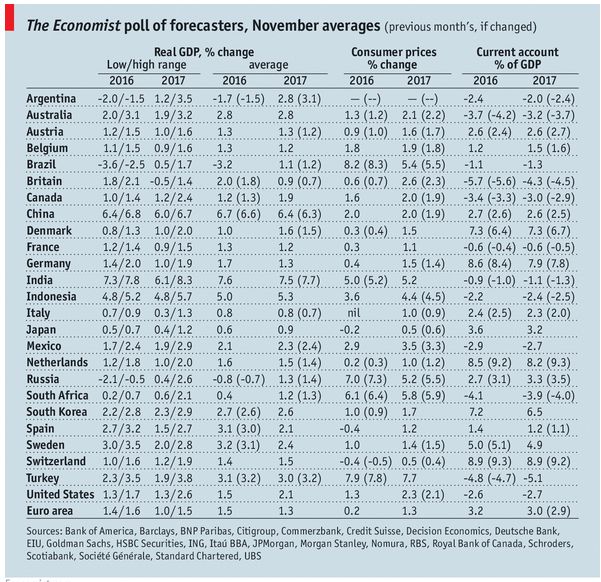

GDP, Consumer Inflation and Current Accounts The economist poll of forecasters November 2016 Source: Economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets,newslettersent