Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss FrancThe Swiss Franc remained nearly unchanged against the euro. It fell to 1.0875 during the day and recovered with the good U.S. new home sales data. |

Click to enlarge. - Click to enlarge |

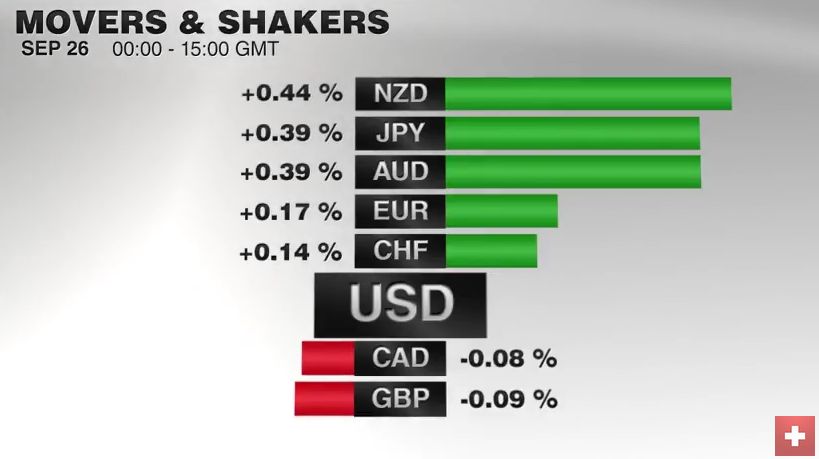

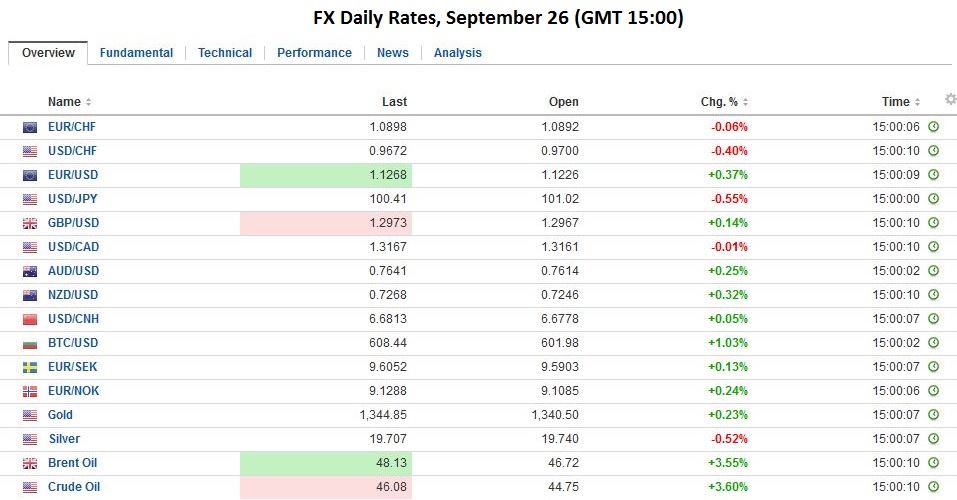

FX RatesThe US dollar is narrowly mixed. The euro, yen and Swiss franc are higher, while the dollar-bloc and sterling are softer. The moving element here is not so much the greenback, which serving more as a fulcrum, but idiosyncratic, country-level developments. The yen is the strongest of the majors. The dollar was turned back from above JPY101 and is now through the pre-weekend low near JPY100.70, is being driven be equity market losses and a belief that the shift in the BOJ’s framework from targeting the monetary base to the yield curve will do nothing to stem the yen’s year-long appreciation. The effort to steepen the yield curve may help solve one issue, the squeeze on banks and insurers, but exacerbates another, namely the recycling of Japan’s current account surplus and foreign investment inflows. |

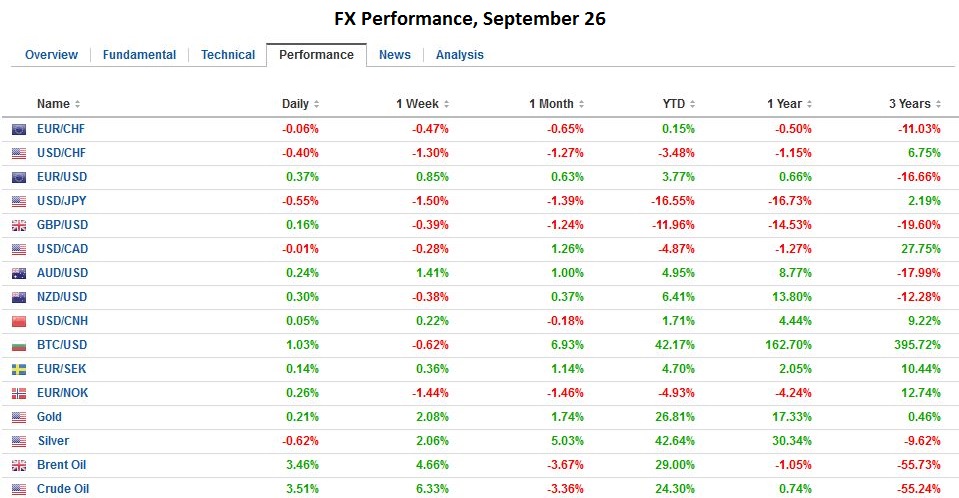

FX Performance September 26 Source DucascopyClick to enlarge. - Click to enlarge |

| Like last Friday, the euro has been confined to last Thursday’s trade range. The high that day was almost $1.1260, which was just above the retracement objective near $1.1250. The range is about than a quarter of a cent today.

Sterling has been unable to resurface of $1.30. This is a continuation of the heavy tone seen since the middle of the month. There has been increased speculation that Article 50 will be triggered, but there has been no clear indication from 10 Downing Street. Some are linking sterling’s weakness to quarter-end position and hedging adjustments. The pre-weekend low was set near $1.2915. It has barely held today. The mid-August low, which would be the next obvious target, is found near $1.2865. |

Click to enlarge. - Click to enlarge |

| The dollar-bloc currencies are slightly lower but have managed to shrug off some poor news. New Zealand reported an August trade deficit three-times greater than the July shortfall and half again as large as expected. Exports fell, and imports rose. The Australian dollar is holding above $0.7600 as last week’s suggestion by the central bank’s Lowe of the possibility of lower rates is shrugged off. The Canadian dollar is the heaviest. It is extending the pre-weekend losses that were spurred by disappointing retail sales and inflation data. The immediate objective is the month’s high for the US dollar near CAD1.3250. |

Click to enlarge. - Click to enlarge |

GermanyGermany’s IFO surprised on the upside after last week’s flash PMI fell to 16-month lows. The business climate reading jumped to 109.5 from 106.3. This is the highest reading since May 2014.

|

Germany Ifo Business Climate Index(see more posts on Germany IFO Business Climate Index, ) Click to enlarge. Source Investing.com - Click to enlarge |

| The current assessment rose to 114.7 from 112.9, and the expectations component rose to 104.5 from 100.1. The market had expected mostly flat readings.

Germany’s largest bank remains under pressure. A press report in Germany indicated that Merkel has ruled out state assistance and will not assert itself large fine sought by US regulators. German financials are the weakest sector today, losing 2.8%, while the overall market is down half as much. |

Germany IFO Business Expectations(see more posts on Germany IFO Business Expectations, ) Click to enlarge. Source Investing.com - Click to enlarge |

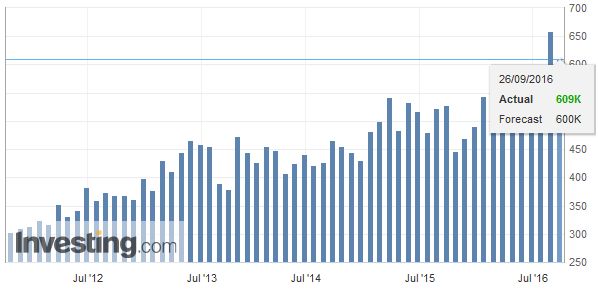

United StatesThe first US presidential debate will be held in the North American evening that will correspond to the start of the Asian session on Tuesday. The Real Clear Politics average of polls has Clinton at 46.5% and Trump at 43.7%. A week ago, the poll average was virtually even at 44.9% to 44.0% for Clinton. Of the last 183 polls through Sunday, Clinton was ahead in 155 and Trump in 21, with seven ties. Of the 100 polls, Clinton was ahead in 85, and Trump led in 11. There were four ties. The remainder of today’s session features speeches by Draghi and Nowotny of the ECB and Tarullo and Kaplan of the Federal Reserve. Bank of Canada’s Poloz will also speak late in the session. The US reports new homes sales for August, which are expected to pare back the outsides 12.4% gain seen in July. |

U.S. New Home Sales(see more posts on U.S. New Home Sales, ) Click to enlarge. Source Investing.com - Click to enlarge |

Spain may have taken a modest step toward resolving its nine-month political deadlock. The success of the PP in Galicia, where it secured a majority, and the success of the Basque Nationalists Party, may sap the ability and/or willingness of the Socialists to continue blocking a minority government led by Rajoy in Madrid. They will have until the end of October or face the third set of national elections in a year.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?

Tags: #GBP,#USD,$CAD,$EUR,Bank of Japan,FX Daily,Germany IFO Business Climate Index,Germany IFO Business Expectations,Japanese yen,newslettersent,U.S. New Home Sales