Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss Franc |

Click to enlarge. |

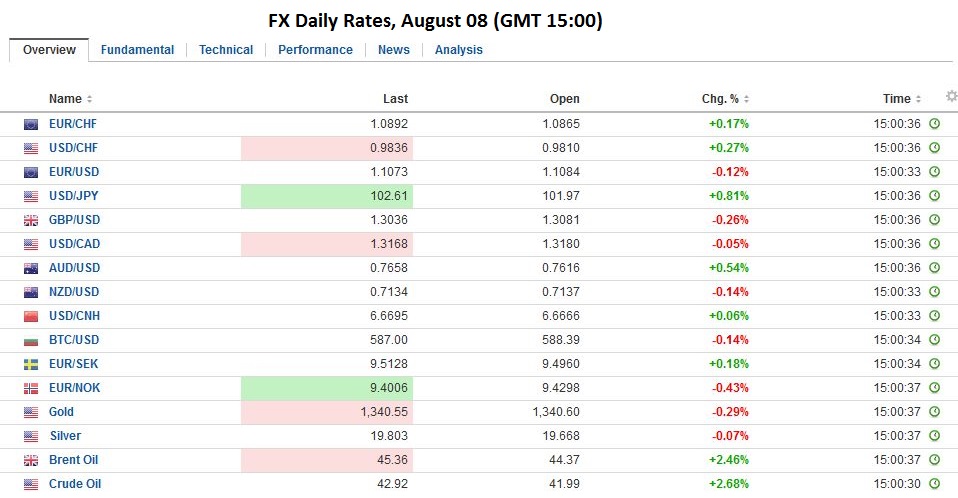

FX RatesInvestors favor risk assets today. Global stocks are moving higher in the wake of the pre-weekend US rally that saw the S&P 500 close at record levels. Bond yields are mostly firmer, again with US move in response to the robust employment report setting the tone in Asia. European bonds participated in most of the pre-weekend move and are consolidating today with a slightly heavier tone. UK Gilts are outperforming, with a new record low of 64 bp on the benchmark 10-year issue.

The Nikkei’s 2.4% rally was the biggest in nearly a month. It gapped sharply higher, leaving a three-day island in its wake, and closed on its highs. All the Asian equity markets advanced. The MSCI Asia-Pacific Index rose 1.3%, its three consecutive advance and the largest since July 11.

|

Click to enlarge. |

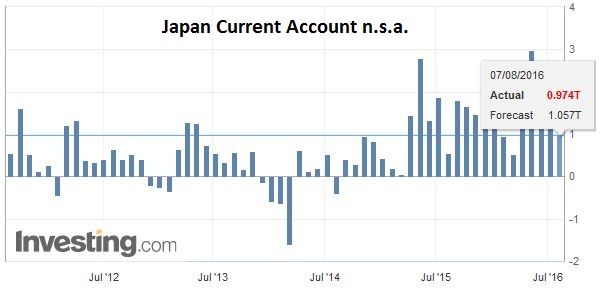

JapanJapan reported its June current account. There is a strong seasonal pattern that the balance typically deteriorates in June from May. The pattern held. The surplus was nearly halved to JPY974.4 bln from JPY1.809 trillion in May. This comes despite the jump in the trade surplus (to JPY763.3 bln from JPY39.9 bln).

|

Click to enlarge. Source Investing.com |

TaiwanFour other markets may be particularly interesting. The first is South Korea. S&P lifted its rating to AA from AA- before the weekend and left the outlook stable. The Kospi advanced 0.6%, and the Korean won was the strongest of the Asian currencies, rising 0.2% against the dollar. In Thailand, voters backed the military-sponsored constitution, which will pave the way for elections. The Thai equity market advanced 1.5%, while the baht slipped almost 0.5%. Taiwan, which has seen strong capital inflows, reported exports rose in July for the first time in 18 months. The Taiwanese equity market rose 0.6%, while the local currency was the second strongest in Asia, rising almost 0.15%.

|

Click to enlarge. Source Investing.com |

ChinaChina reported July reserves in line with expectations and little changed from June at just above $3.2 trillion. It also reported a larger than expected July trade surplus. In dollar terms, the surplus rose to $52.3 bln from $48.1 bln. The driver was not so much stronger exports as weaker imports.

Exports fell 4.4% year-over-year in dollar terms, a touch slower than the 4.8% decline reported in June. In yuan terms, exports rose 2.9% year-over-year, up from 1.3% in June.

|

Click to enlarge. Source Investing.com |

| Imports fell 12.5% in dollar terms, and 5.7% in yuan terms. This compares with an 8.4% drop and a 2.3% fall respectively in June. |

Click to enlarge. Source Investing.com |

Eurozone

Europe is quieter than Asia. The Dow Jones Stoxx 60 is up about 0.7% in late-morning turnover in London. The financials are leading the way with nearly a 2% gain. Insurers setting the pace with a 2.7% rise and banks up 2.1%. Real estate is flat-to-lower. Italian banks shares are up 2.4% following the pre-weekend nearly 5% advance. It is the third consecutive advance.

There are three developments to note. First, before the weekend, DBRS indicated it would review Italy’s debt rating, with negative implications. It gives Italy a low A-rating, which has prevented a larger haircut using Italian bonds as collateral for borrow at the ECB. Ostensibly, the referendum, which Italy’s high court is expected to give its go-ahead later today, is the trigger. Prime Minister Renzi has threatened to resign it if is not accepted, which seems to be the odds-on most likely scenario. Italy’s 10-year bond yields is up 2 bp today, the same as Spain.

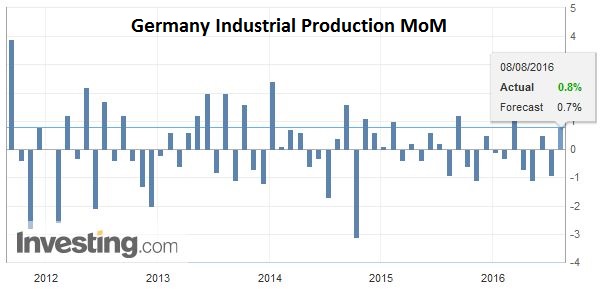

GermanySecond, Germany reported a 0.8% rise in June’s industrial output, and it revised to -0.9% the May decline that was initially reported at -1.3%. The output for investment goods offset the weaker construction and energy output. It follows the unexpected decline in June factory orders (-0.4%) reported before the weekend. Germany will report its June trade balance surplus tomorrow. It is expected to widen to 23.0 bln euros from 21.0 bln in May. The record was set in March at 26.2 bln euros.

|

Click to enlarge. Source Investing.com |

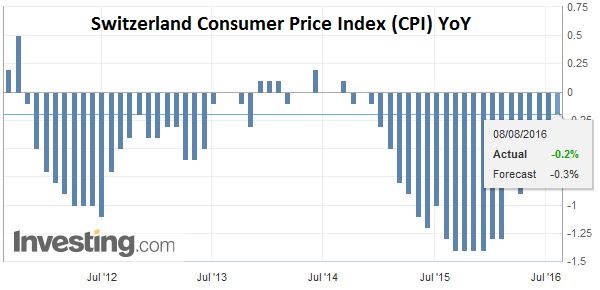

SwitzerlandThird, Switzerland reported July CPI figures. The national measure fell 0.4% in July for a minus 0.2% year-over-year pace. The EU-harmonized measures slipped 0.1% on the month, which is the first decline since January. Nevertheless, due to the base-effect, the year-over-year pace rose to –0.5% from -0.6%. This matches its best level since March 2015. Recall that the year-over-year pace bottomed in January at -1.5%.

|

Click to enlarge. Source Investing.com |

United States

The US dollar is softer against most of the major and emerging market currencies. It is largely consolidating the jobs-inspired gains. The yen is the weakest of the majors. It is off 0.6%. It is approaching the JPY102.60 area that corresponds to a 38.2% retacement of the drop since the BOJ’s disappointment at the end of July. Last week’s high was set near JPY102.85 before the move toward JPY100.70, where it seemed to carve out a shelf. The is in less than a third of a cent range today, mostly below $1.11 and is uninspiring. Sterling is in a two-thirds of a cent range, pinned near the pre-weekend lows. In Europe, sterling is encountering offers in the $1.3060 area. The Australian and Canadian dollars are firm, while the Kiwi is heavy ahead of the rate cut August 10.

Look for a quiet North American summer session with a light economic calendar.

Graphs and additional information on Swiss Franc by the snbchf team.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: Bank of Japan,China Exports,China Imports,ECB,FX Daily,Germany Industrial Production,Japan Current Account,newslettersent,Switzerland Consumer Price Index