Well that did not last long. After initial exuberance over The BoJ's wishy-washy decision to adopt a 3-tiered rate policy including NIRP, markets have realized that without further asset purchases (which were maintained at the current pace), there is no ammo to lift stocks. An almost 200 point surge in Dow futures has been erased and Nikkei 225 has dropped 1000 points from its post BOJ highs...

Dow futures have plunged...

What a mess...

And Nikkei has crashed over 1000 points...

And bond yields are collapsing...

- *JAPAN'S 20-YEAR BOND YIELD FALLS TO 0.82%, LOWEST SINCE 2003

- *JAPAN'S 10-YEAR YIELD FALLS TO RECORD 0.11%

The reaction is starting to sink in...

- *NOMURA: BANKS TO FEEL BIGGEST DIRECT IMPACT FROM BOJ ACTION

- *NOMURA: WORRY THAT JAPANESE BANKS PROFITS MAY BE HURT AS SYSTEM

- *NOMURA: FOR WEAK JAPANESE REGIONAL BANKS IMPACT MAY BE TOUGHEST

- *NOMURA: BANKS MAY SEEK TO INCREASE LENDING TO MID-SIZED FIRMS

Of course the reality that is sinking in is that,. as Citi's Matt King noted, without an acceleration in direct reserves increases (i.e. moar QE) then net net this is a negative for the only indicator that matters to the world's financials - global net liquidty, which with EM reserves bleeding and The Fed on hold, China merely papering over the cracks with daily help, and ECB jawboning, means the world's last best hope - Kuorda-san - just let them down.

We hope that after they see the following chart, which shows not only DM net liquidity injections (i.e., q-easing), but also EM net liquidity outflows (i.e., quantitative tightening) and which explains not only the recent selloff, but also shows how to trade global central bank and sovereign wealth fund and reserve manager flows, all confusion and denial will end.

* * *

As Bloomberg reports, The Bank of Japan has surprised the markets in its first meeting of 2016, with a decision to shift interest rates into negative territory.

- The BOJ will pay an interest rate of -0.1% on current accounts held by financial institutions. Policy makers also signaled their willingness to do more, saying they would “cut interest rates further into negative territory if judged as necessary.”

- The move should bolster inflation through the exchange-rate channel; the yen dropped immediately below 121 to the dollar after the announcement before regaining some lost ground. It should also kick start lending by punishing banks for keeping funds idle in BOJ deposits.

- The danger is that negative rates put the sustainability of the BOJ’s policy framework at risk. Japan’s banks can hardly be expected to sell their Japanese government bonds to the BOJ if rates on the cash they receive in return will be negative.

- In addition, if negative rates spur investment in financial assets rather than an expansion of loans to fund capital spending, the result could be growing risks to financial stability.

- The controversial nature of the move is underlined by the split vote in the BOJ board, with the shift to negative rates only passing by a narrow 5-4 majority.

- The BOJ left its 80 trillion yen ($670 billion) asset purchase program unchanged.

Key Points of Today’s Policy Decision (via The BoJ)

The Introduction of "Quantitative and Qualitative Monetary Easing (QQE) with a Negative Interest Rate"

The Bank will apply a negative interest rate of minus 0.1 percent to current accounts that financial institutions hold at the Bank. It will cut the interest rate further into negative territory if judged as necessary.

The Bank will introduce a multiple-tier system which some central banks in Europe (e.g. the Swiss National Bank) have put in place. Specifically, it will adopt a three-tier system in which the outstanding balance of each financial institution’s current account at the Bank will be divided into three tiers, to each of which a positive interest rate, a zero interest rate, or a negative interest rate will be applied, respectively.

"QQE with a Negative Interest Rate" is designed to enable the Bank to pursue additional monetary easing in terms of three dimensions, combining a negative interest rate with quantity and quality.

The Bank will lower the short end of the yield curve and will exert further downward pressure on interest rates across the entire yield curve through a combination of a negative interest rate and large-scale purchases of JGBs.

The Bank will achieve the price stability target of 2 percent at the earliest possible time by making full use of possible measures in terms of the three dimensions.

Q1. Will the Bank continue to purchase Japanese government bonds (JGBs) after the introduction of a negative interest rate?

A. Under "QQE with a Negative Interest Rate," the Bank will pursue monetary easing by making full use of possible measures in terms of three dimensions, combining quantity, quality, and interest rate. It will lower the short end of the yield curve by slashing its deposit rate on current accounts into negative territory and will exert further downward pressure on interest rates across the entire yield curve, in combination with large-scale purchases of JGBs.

Q2. Will a negative interest rate make it difficult for the Bank to continue purchasing JGBs?

A. The Bank can continue purchasing JGBs because costs of negative interest will be passed on to its purchasing prices of JGBs (or yields on JGBs purchased by the Bank) so that the prices will be higher (or the yields will be lower). The European Central Bank has been implementing a combination of its Asset Purchase Program and a negative deposit facility rate. The Bank will conduct JGB purchases while paying due attention to the impact of a negative interest rate on the JGB market.

Q3. Will a negative interest rate cause a decrease in financial institutions’ earnings?

A. When central banks aim at boosting the real economy through monetary easing measures, these measures can negatively affect the earnings of financial institutions which function as financial intermediaries. In deciding the introduction of a negative interest rate at the Monetary Policy Meeting held today, the Bank also decided to adopt a three-tier system in which a positive interest rate or a zero interest rate will be applied to current account balances up to certain thresholds in order to make sure that financial institutions’ functions as financial intermediaries would not be impaired due to undue decreases in financial institutions’ earnings. It should be noted that overcoming deflation as soon as possible and exiting from the low interest-rate environment lasting for two decades is essential for improving the business conditions for the financial industry.

Q4. Will a negative interest rate be effective under the three-tier system, given that the negative rate will be applied partially?

A. Transaction prices in financial markets (e.g. interest rates, stock prices, and exchange rates) are determined by marginal losses or gains made in a new transaction. Although a negative interest rate is not applied to the total outstanding balances of current accounts, costs incurred with an increase in the current account balance brought by a new transaction will be minus 0.1 percent if it is applied to a marginal increase in the current account balance. Interest rates and asset prices will be determined in financial markets based on that premise.

Q5. How far into negative territory can the interest rate be moved?

A. With regard to potential problems associated with negative interest rates, the following can be mentioned: (1) if the decrease in financial institutions’ earnings due to negative interest rates become sizable, it could impair their functions as financial intermediaries; and (2) if financial institutions reduce their outstanding balances of the central bank’s current accounts with which a negative interest rate is charged and significantly increase their cash holdings which yield zero interest, the effects of negative interest rates will be lessened.

The Bank of Japan’s framework is designed to address these potential problems. With regard to (1), the Bank has adopted a three-tier system in order to mitigate a concern over undue impact on financial institutions’ earnings. With regard to (2), if a financial institution increases its cash holdings significantly, the Bank will deduct an increase in its cash holdings from the zero interest-rate tiers of current account balance. Thus, a negative interest rate will be charged on the increase in its cash holdings. Similar multiple-tier systems are adopted in countries where the size of negative interest rates is relatively large, including Switzerland (minus 0.75 percent), Sweden (minus 1.1 percent), and Denmark (minus 0.65 percent).

Q6. Given that the interest rate on current accounts at the Bank becomes negative, don’t you think financial institutions will stop using the Fund-Provisioning Measure to Stimulate Bank Lending, the Fund-Provisioning Measure to Support Strengthening the Foundations for Economic Growth, and the Funds-Supplying Operation to Support Financial Institutions in Disaster Areas affected by the Great East Japan Earthquake?

A. The Bank judges that these measures are playing an important role and it is not desirable that a negative interest rate on current accounts at the Bank would provide a disincentive for financial institutions to use these facilities. On this basis, the Bank decided to cut its lending rates for these facilities to zero percent and also to allow the amounts outstanding of the Bank’s provision of credit through these facilities to be included in the tier of current account balances to which a zero interest rate will be applied. Therefore, while the outstanding balances of current accounts which financial institutions hold at the Bank will increase due to the use of these facilities, these financial institutions will not incur a negative margin and thus will not be discouraged to use them.

Q7. Please explain why the Bank will adjust the tiers of current account balances, to which a zero interest rate will be applied, at an appropriate timing.

A. As the monetary base will grow at an annual pace of about 80 trillion yen in line with the Bank’s current guideline for money market operations, the outstanding balances of current accounts at the Bank will increase on an aggregate basis. In this situation, the Bank will accordingly increase the tiers of financial institutions’ balances of current accounts to which zero interest rates will be applied at an appropriate timing so that the balances to which a negative interest rate will be applied will remain at adequate levels.

* * *

As we explained earlier...while keeping asset purchases the same, The Bank of Japan confirmed the earlier leaked details that it will shift to a negative interest rate policy:

- *BOJ: ADOPTS RATE OF -0.1%

- *BOJ: VOTES 5-4 TO ADOPT NEGATIVE INTEREST RATES

- *BOJ: WILL CUT RATE FURTHER IF NEEDED

- *BOJ: KEEPS ASSET PURCHASES UNCHANGED

- *BOJ RETAINS PLAN FOR 80T YEN ANNUAL RISE IN MONETARY BASE

- *BOJ: JAPAN ECONOMY HAS CONTINUED TO RECOVERY MODERATELY

- *BANK OF JAPAN: NEGATIVE INTEREST RATE TO APPLY FROM FEB. 16

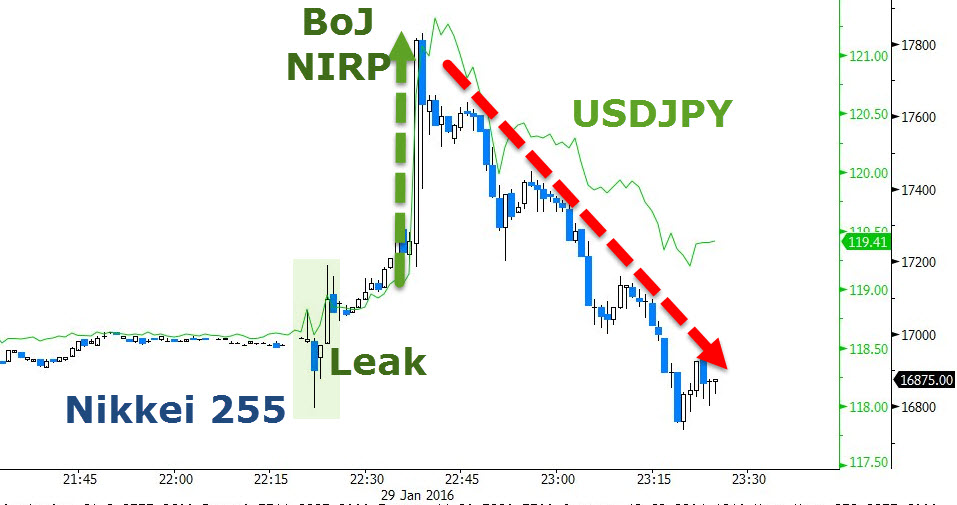

Clearly the decision was far from unanimous. Japanese stocks and USDJPY have exploded higher...

The adoption of NIRP enables The BoJ to break the bond market even further...

- *BOJ: POLICY FRAMEWORK DESIGNED TO LET BOJ PURSUE MORE EASING

- *BOJ: TIERS TO INCLUDE POSITIVE RATE, ZERO RATE OR NEGATIVE RATE

- *BOJ: MULTI TIER SYSTEM RESEMBLES SOME IN EUROPE E.G. SWISS BANK

- *BOJ: DEPOSIT RATE CUT WILL LOWER SHORT END OF YIELD CURVE

So The BoJ follows EU's route - because that has worked out so well for them!!

- *BOJ: 3-TIER RATES ENSURE NO `UNDUE DECREASES' IN BANK EARNINGS

- *BANK OF JAPAN: NEGATIVE INTEREST RATE TO APPLY FROM FEB. 16

- *BOJ: POSITIVE RATE OF 0.1% APPLIES TO EXISTING BALANCE

- *BOJ: ZERO RATE APPLIES TO REQUIRED RESERVES HELD BY BANKS

- *BOJ:MINUS RATE APPLIES TO ACCOUNTS IN EXCESS OF THESE AMOUNTS

- *BOJ WILL CONTINUE NOT TO SET LOWER BOUND FOR YIELD ON JGB BUYS

In other words - all excess reserves will cost you - so liquify the stock market with them!

Dow futures are soaring on the collapse in Yen...

* * *

As we detailed earlier, just minutes before The BoJ is due to release its statement, USDJPY and Nikkei 225 went haywire around 2220ET as Nikkei news dropped a headline about NIRP discussions taking place at The BoJ. This is not the BoJ statement but has sparked chaos in Japanese (and all carry trade linked markets). We can only assume this was some well-placed strawman for The BoJ statement enabling Kuroda to get a glimpse of what is possible.

Total chaos broke out ahead of the BoJ Statement...as Nikkei News dropped this headline...

- *BOJ DISCUSSES NEGATIVE INTEREST RATE POLICY, NIKKEI SAYS

BOJ discusses introduction of negative interest rates today at policy meeting, Nikkei reports.

- Negative rates discussed due to growing concern of downward pressure on Japan economy and CPI because of cheap crude oil, China slowdown: Nikkei

Nikkei 225 is up 500 points on the news, USDJPY +50 pips

Some context for that move...

Having given up all its gains since the last QQE update...

G622

Full story here Are you the author?

Tags: Bank of Japan,Bond yield,Carry Trade,central banks,China,Crude Oil,European central bank,excess reserves,Japan,Japanese yen,Monetary Base,Monetary Policy,Nikkei,Nomura,Reality,recovery,Swiss National Bank,Switzerland,Yield Curve