Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The latest Commitment of Traders report that covers the four sessions through January 19 saw speculators anticipating the continuation of the current moves. Of the sixteen gross positions we track, only five were in reducing exposures. Last week there was only six increased exposures.

The latest Commitment of Traders report that covers the four sessions through January 19 saw speculators anticipating the continuation of the current moves. Of the sixteen gross positions we track, only five were in reducing exposures. Last week there was only six increased exposures.With the benefit of hindsight, we know that something changed a day or two after the reporting period ended. Given the magnitude of the reversal in some cases, some of these late positions were likely forced out.

There were two significant gross position adjustments (10k of more contracts) during the reporting period. The bears added 11.6k contracts to their gross short sterling position, which stood at 76.4k contracts at the end of the period. It is the largest such position since March 2015. The other was the 10.2k increase in the gross short Australian dollar speculative position to 81.7k. It has increased by more than a third since the start of the year.

Speculators generally increased their gross short currency exposures. There were two exceptions. These were the euro (gross shorts were reduced by 3.1k contracts) and yen (gross shorts were reduced by 6.3k contracts). The gross short euro position has been above 200k contracts since early November. The gross short yen position has fallen from 113k contracts in the middle of November to 46.8k contracts in the latest reporting period.

Speculators mostly increased gross long positions. The three dollar-bloc currencies were the exceptions. Given the spot moves, though the adjustment by the speculators in the futures market was minor. The gross long Canadian dollar positions was cut by 5.8k contracts to 33.1k. The gross long Australian dollar position was trimmed by 3.1k contracts to 45.5k. Speculators pared their long New Zealand dollar position by 2.2k contracts to 17.9k. The net Kiwi position flipped back to the short-side with the help of the bears adding 2.3k contracts to the gross shorts.

If our suggestion that it is helpful to conceive of the dollar as not the mover presently but the fulcrum, with the dollar-bloc, and sterling on one side and the euro, yen and Swiss franc on the other, then the surprise is with the speculators adding to long sterling and peso positions. The bottom pickers added 3.6k contracts to the gross long sterling position (to 37.9k). The gross long peso position edged up less than 1k contracts to 30.4k. If they held on as the peso made new lows on January 21, they were rewarded on January 22 as the peso posted its largest advance in 10 months.

Bullish speculators were happy to take profits into the rally in the US 10-year Treasury note futures. The gross longs sold 18.1k contracts to leave them with 413.4k contracts. Some sold into the rally. The gross short position was increased by 6.4k contracts to 481.1k. This resulted in an increase in the net short position from 43.2k contracts to 67.7k.

In contrast, in the light sweet crude oil futures short took some profits, but there were no bottom picked as the gross longs were pared. The gross long position fell by 17k contracts (to 482.8k), and the gross long position fell by 10% (32.9k contracts) to 303.4k. The low was set the next day, but its was several percentage points below January 19 when the reporting period ended. The March contract closed on January 22 $4.80 above it lows and posted its highest close in nearly two weeks.

| 19-Jan | Commitment of Traders | |||||

| Net | Prior | Gross Long | Change | Gross Short | Change | |

| Euro | -137.0 | -146.5 | 69.4 | 6.3 | 206.5 | -3.1 |

| Yen | 37.7 | 25.3 | 84.5 | 6.1 | 46.8 | -6.3 |

| Sterling | -38.6 | -30.5 | 37.9 | 3.6 | 76.4 | 11.6 |

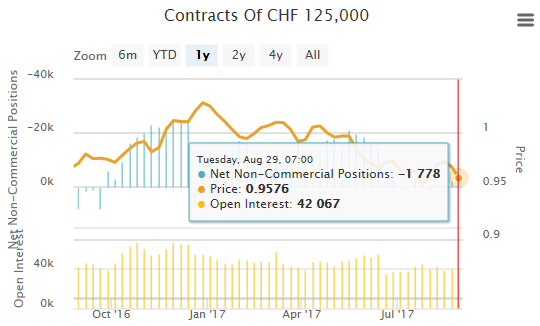

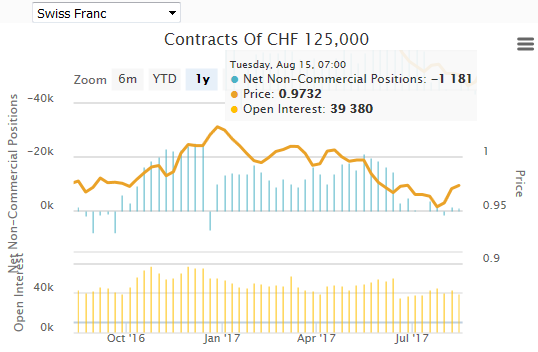

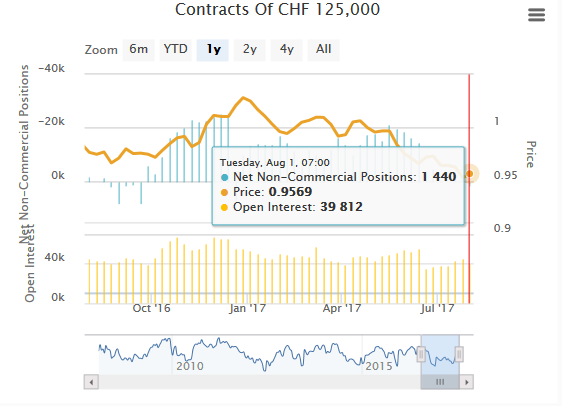

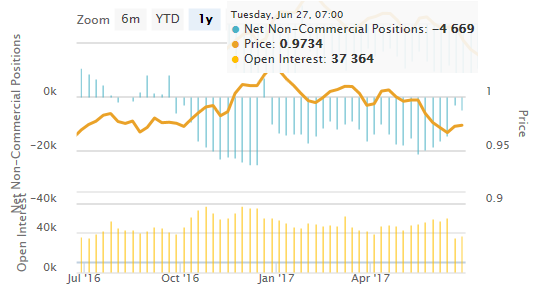

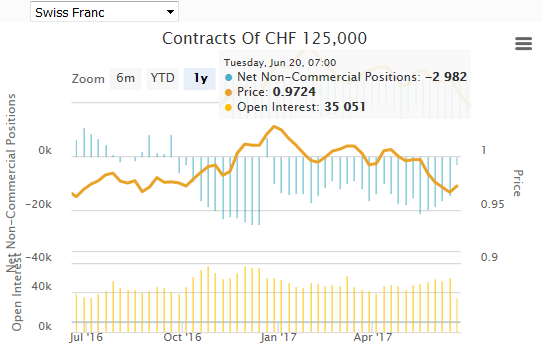

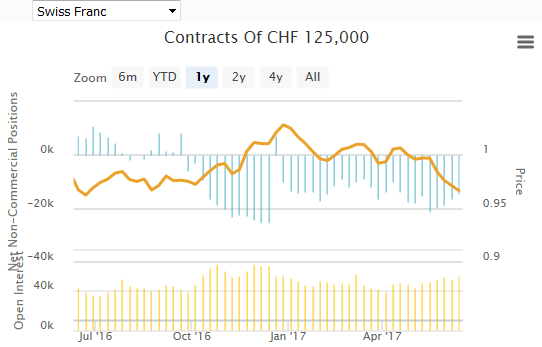

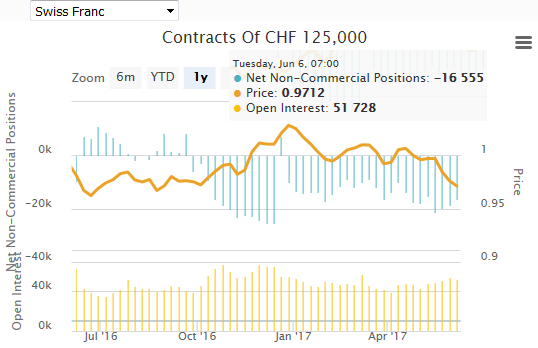

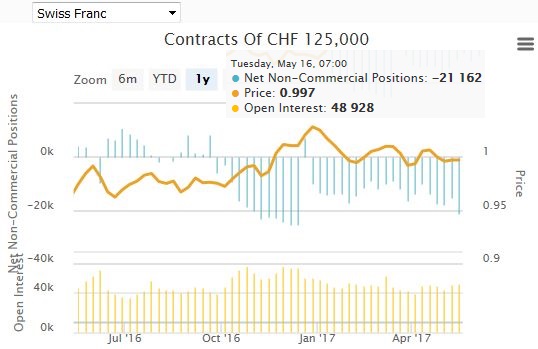

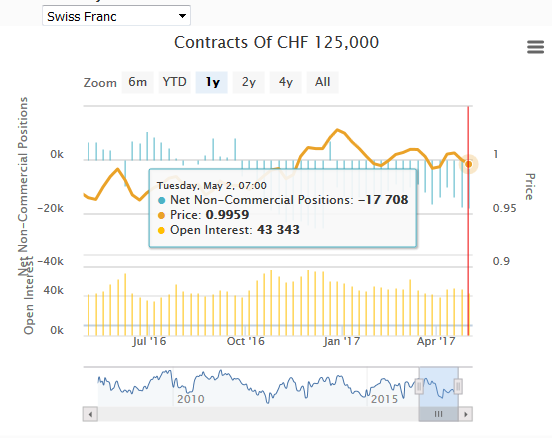

| Swiss Franc | 0.9 | 3.3 | 25.2 | 0.7 | 24.3 | 3.1 |

| C$ | -66.4 | -59.2 | 33.1 | -5.8 | 99.5 | 1.4 |

| A$ | -36.3 | -23.0 | 45.5 | -3.1 | 81.7 | 10.2 |

| NZ$ | -3.0 | 1.5 | 14.9 | -2.2 | 17.9 | 2.3 |

| Mexican Peso | -76.0 | -74.0 | 30.4 | 0.9 | 106.4 | 2.9 |

| (CFTC, Bloomberg) Speculative positions in 000's of contracts | ||||||

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: Commitments of Traders,Speculative Positions