Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Speculative position adjustments in the currency futures were minimal in the immediate aftermath of the ECB's December 3 meeting and US employment data the following day. However, activity dramatically increased in the days ahead of the FOMC meeting on December 16.

Speculative position adjustments in the currency futures were minimal in the immediate aftermath of the ECB's December 3 meeting and US employment data the following day. However, activity dramatically increased in the days ahead of the FOMC meeting on December 16. In most Commitment of Traders reports the gross position adjustment of 10k or more contracts is seen in three or four of the 16 gross currency positions we track. In the latest report, which covers the five sessions before the conclusion of the FOMC meeting, there were seven gross currency position adjustments of more than 10k contracts. Also, there were only two gross currency position adjustments of less than 5k contracts, which is also unusual.

The first development to note is that among the major currencies (euro, yen, sterling and Swiss franc), there was a short squeeze. The speculative bears covered 21.5k gross short euro contracts (leaving 231.3k). During the previous reporting period, only 9k gross short contracts were covered.

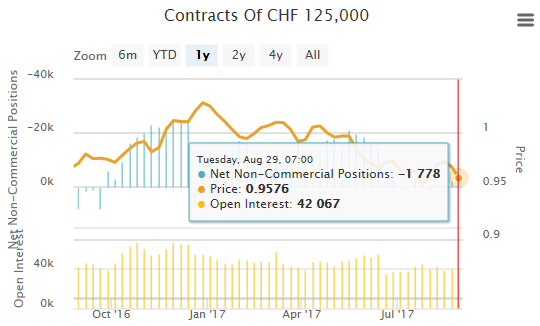

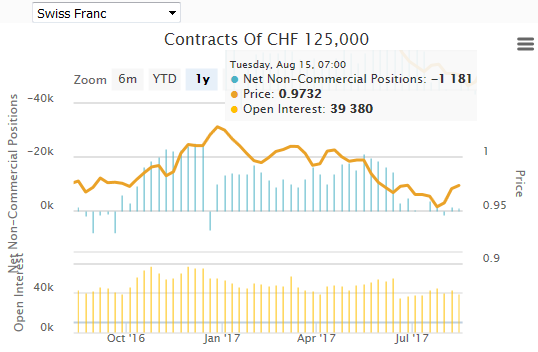

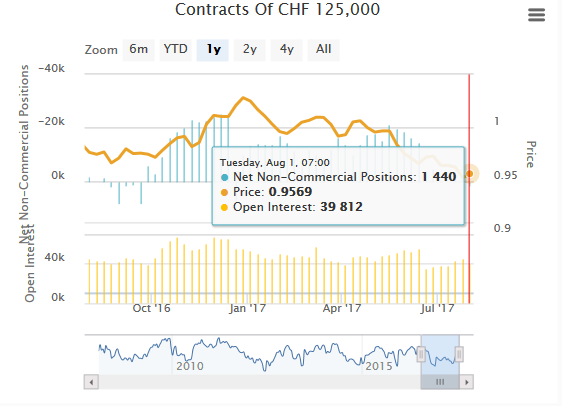

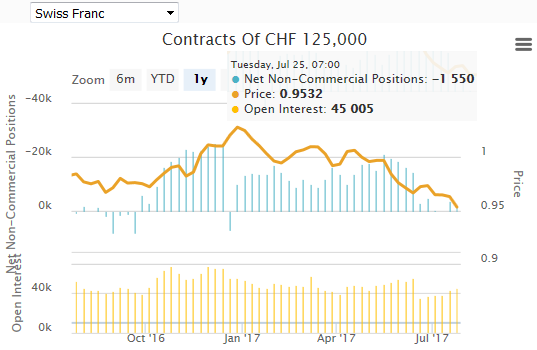

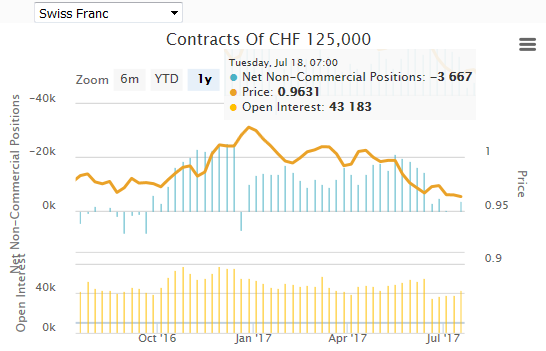

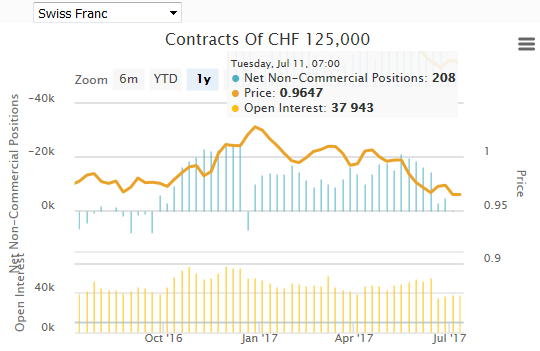

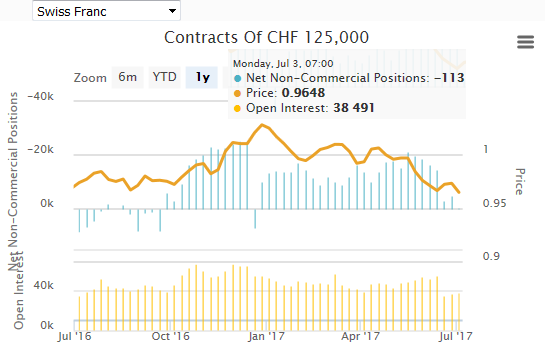

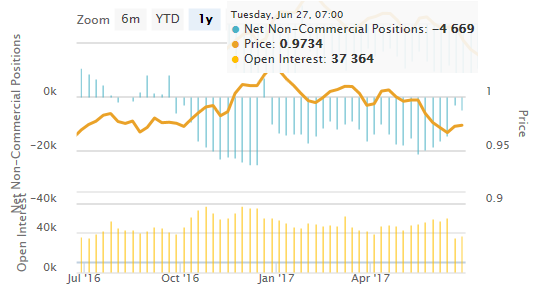

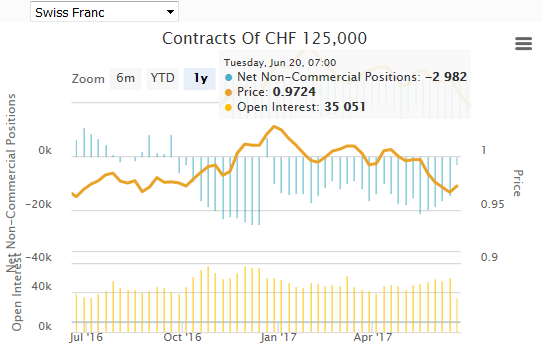

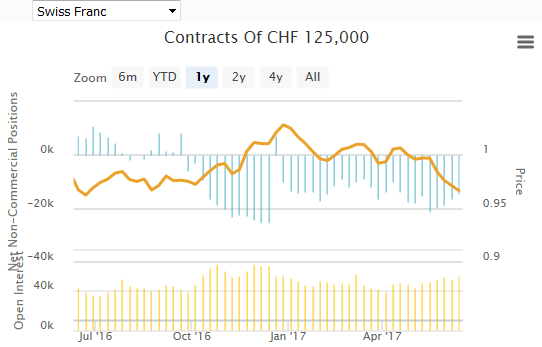

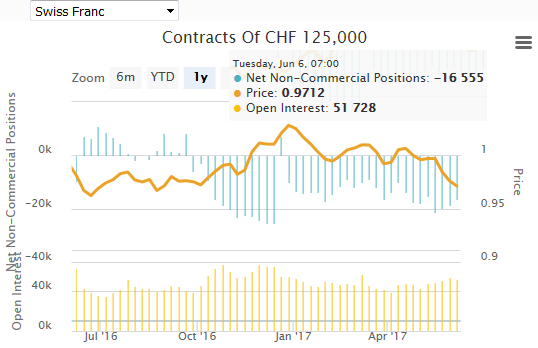

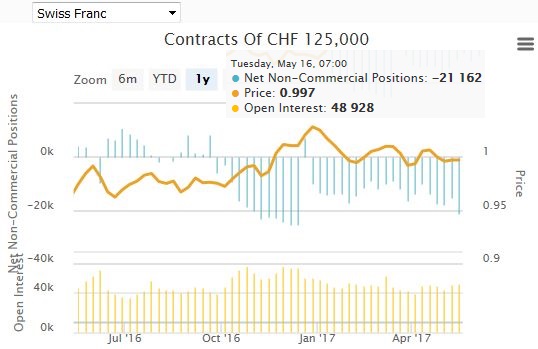

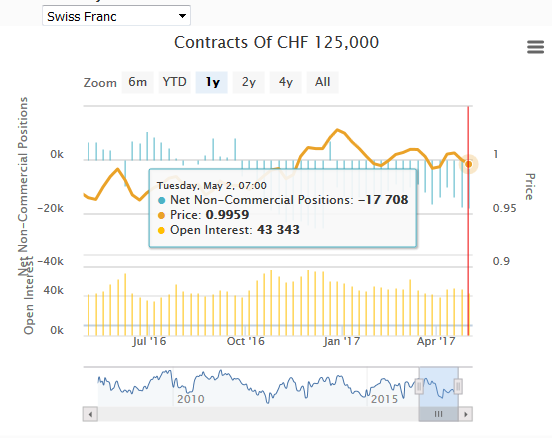

The yen bears cut the gross short position by nearly a third to 63.9k contracts. In percentage terms, it is the largest bout of short-covering in four years. In sterling, 9.5k short contracts were covered (leaving 56.0k). This helped drive the net short sterling position to 16.9k contracts, which is the smallest net short position in a month. Short-covering reduced the gross short Swiss franc position by a quarter to 27.8k contract. In percentage terms, the 9.3k contracts was the largest reduction of short positions since May.

The second broad trend was a more bearish view of the dollar bloc currencies and peso. The Australian dollar is an exception, but the gross longs were cut in the Canadian dollar (4.5k contracts), the New Zealand dollar (8.1k contracts) and Mexican peso (10.4k contracts). The gross short positions were mixed. In the Aussie and Kiwi, they were reduced by 8.9k contracts and three hundred contracts respectively. Gross shorts increased by 6.4k contracts in the Canadian dollar and 25.5k contracts in the Mexican peso.

The position adjustment in the euro continues to lag behind the adjustment in the other majors. Consider that the net short euro position has been trimmed to 159.6k contracts from 182k 48 hours before the ECB meeting. The net short yen position is 2/3 smaller at 26.6k contracts, after peaking in late-November near 78.6k contracts. The net short sterling position has been halved since the 32.3k was seen in late-November to stand at 16.9k as of December 15. The net speculative Swiss franc position swung back to the long side. In the prior reporting period, speculators were net short 25.5k franc contracts.

Speculators have turned decidedly bearish the Canadian dollar and Mexican peso. The net short Canadian dollar position was a little below 18k in the middle of last month. As of the FOMC decision, it stood at 51k contacts. In late-October and early-November, speculators were net short less than 1000 peso contracts. It has jumped to 60.4k contracts.

Speculators trimmed their net long crude oil futures contracts by 10.8k to 210.5k contracts. The bulls slimmed their gross long position by 7.9k contracts (leaving 472.2k). The bears took some profits, reducing the gross position by 20.5k contracts. It stands at 261.7k contracts.

The speculative net short 10-year Treasury futures contracts was halved to 11.4k contracts. This was a function of 9.2k contracts having been added to the gross long position, raising it to 444.7k contracts. The gross short position was pared by 3.9k contracts. That left 456.1k contracts still short.

| 15-Dec | Commitment of Traders | |||||

| Net | Prior | Gross Long | Change | Gross Short | Change | |

| Euro | -159.6 | -172.3 | 71.3 | -9.1 | 231.3 | -21.5 |

| Yen | -26.6 | -68.1 | 37.3 | 10.9 | 63.9 | -30.6 |

| Sterling | -16.9 | -23.9 | 39.1 | -2.5 | 56.0 | -9.5 |

| Swiss Franc | 2.0 | -25.5 | 29.7 | 18.2 | 27.8 | -9.3 |

| C$ | -51.0 | -40.1 | 44.3 | -4.5 | 95.3 | 6.4 |

| A$ | -33.6 | -33.6 | 47.7 | -0.4 | 81.2 | -13.4 |

| NZ$ | 1.1 | 8.9 | 16.3 | -8.1 | 15.2 | -0.3 |

| Mexican Peso | -60.1 | -24.4 | 34.8 | -10.4 | 95.2 | 25.5 |

| (CFTC, Bloomberg) Speculative positions in 000's of contracts | ||||||

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: Commitments of Traders,Speculative Positions