George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Monetary Assessment: Key phrases from Fritz Zurbrügg

Developments on the financial markets

In December, at the last news conference, I remarked on an easing of tensions on the financial markets. This easing largely continued in the first half of 2013 The government bonds of the European peripheral countries, in particular, benefited from the greater trust of investors,….

In the positive risk climate, investments perceived as secure have lost value. A prominent example is gold: The dollar price per fine ounce of gold had risen in 2011 to a high of USD 1,900. Currently, it is approximately a quarter lower.

Since January, the euro/Swiss franc exchange rate has moved further away from the minimum rate of CHF 1.20 … On a trade-weighted basis, however, the Swiss franc has remained largely unchanged since the beginning of the year.

Last December, the SNB announced it would be opening a branch office in Singapore….to expand our market coverage in Asia …. It will open in July, with a staff of seven.

Management of currency reserves

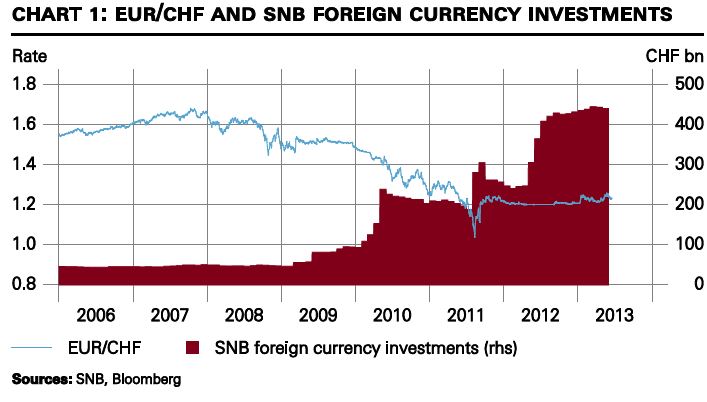

At the end of May, the SNB held foreign currency investments of just over CHF 440 billion (cf. chart 1).

Due to our liquidity and security requirements, a large portion of our foreign exchange holdings are in government bonds and deposits with other central banks. This portion amounted to 78% at the end of the first quarter of 2013. To further diversify investment risk and increase investment in real assets, we raised our proportion of equities from 12% to 15% in the first quarter. We currently hold equities worth around CHF 65 billion, which is three times more than at the end of 2011. In this regard, we have widened our scope to include shares of companies with relatively small market capitalisation, as well as those in advanced economies not previously considered, with the result that our equity portfolio now covers all advanced economies

The proportion of gold in the currency reserves amounted to 10%. From an investment viewpoint, gold is important for a good diversification of the currency reserves. Historically, gold often moves in an opposite direction to other assets. In contrast to equities or bonds, however, gold does not yield interest or dividends. And as the recent months have shown, gold is also among the most volatile and therefore most risky.

Swiss franc money market and reference interest rates

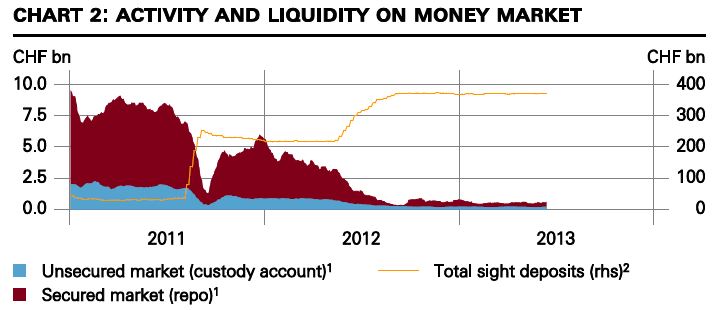

The continuing high level of Swiss franc liquidity has had the desired effect of keeping money market interest rates at close to zero.

The three-month Libor has been at around two basis points since mid-January. Interest rate expectations, based on Libor future contracts, are also close to zero for the foreseeable future, but not negative, as was the case over much of last year. As a result of the very low money market interest rates and high liquidity in the banking sector, money market turnover has dropped substantially in recent years. This is illustrated in chart 2, which shows the total of banks’ sight deposits at the SNB, as well as turnover in the area of secured and unsecured call money.

The small number of transactions on the money market is a problem for generating representative reference interest rates. In addition, the selection and setting of reference interest rates has come under the scrutiny of market participants and the public, as a consequence of the Libor manipulation.

… reform are underway on an international level. The aim is to make the Libor more representative and to restore the trust of market participants.

The responsibility for the provision of reference interest rates therefore lies primarily with the market participants…. SNB is playing a supportive role

Future of the repo market infrastructure in Switzerland

… the SNB has decided to conduct its monetary policy operations via a new [repo] trading platform, provided by SIX Group Ltd, as of May 2014. In this way, the repo market will be based on an integrated solution,

next page: The most interesting questions in the Q&A session

Tags: currency reserves,Monetary Policy,Swiss National Bank

1 comments

hr4free.org

2014-01-07 at 17:13 (UTC 2) Link to this comment

Very interesting analysis. Perfectly fits my expectations given the SNB’s current monetary creation drive.