Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

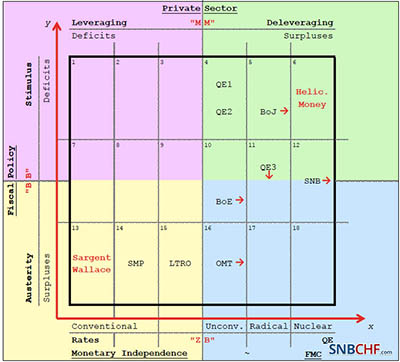

Helicopter Money and the End of Taxes

Helicopter Money and the End of Taxes1 Oct 2020

Albert Edwards: Investors Should Brace For A World Of Negative Rates, 15percent Budget Deficits And Helicopter Money

Albert Edwards: Investors Should Brace For A World Of Negative Rates, 15percent Budget Deficits And Helicopter Money8 Feb 2019

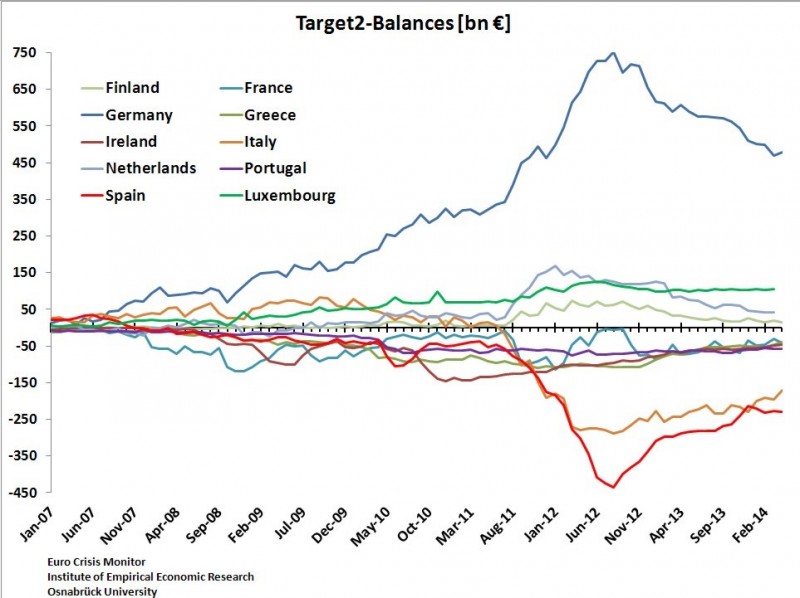

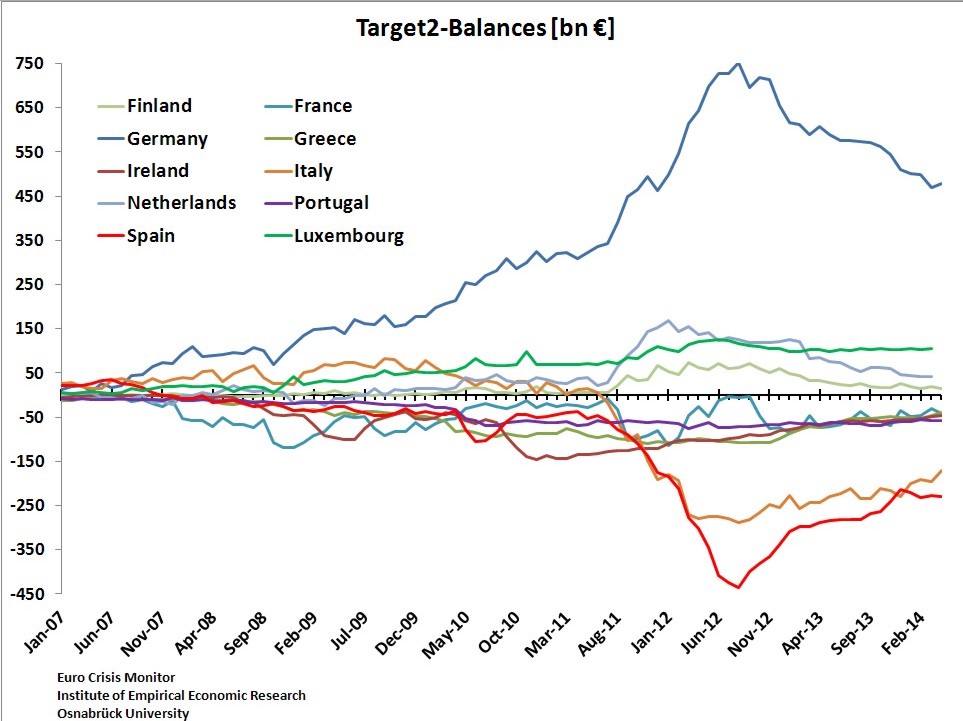

Negative Rates for Bundesbank TARGET2 Surplus?

Negative Rates for Bundesbank TARGET2 Surplus?13 Jun 2014

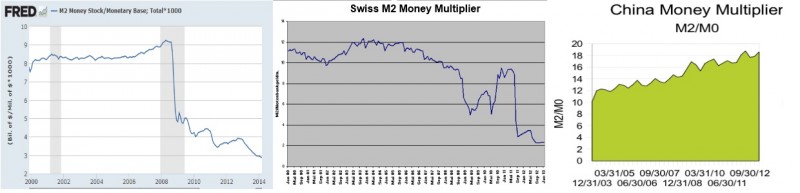

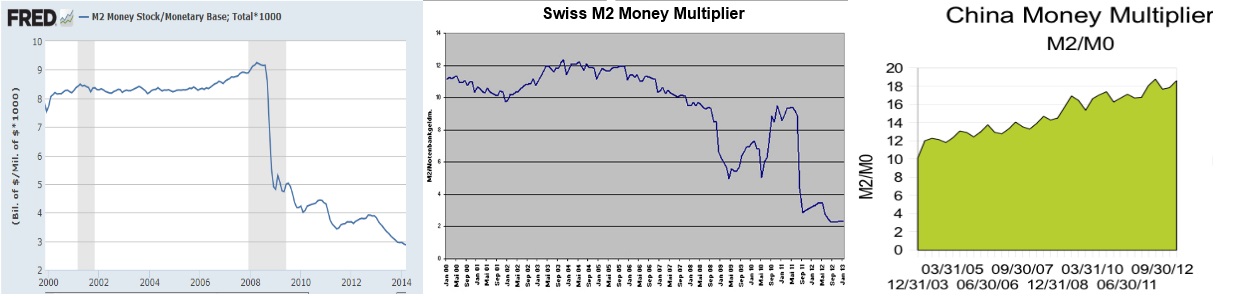

QE, QEE, the Money Multiplier and the Secular Stagnation Confusion

QE, QEE, the Money Multiplier and the Secular Stagnation Confusion29 Apr 2014

Quantitative Easing, its Indicators and the Swiss Franc, Update FOMC September 201318 Sep 2013

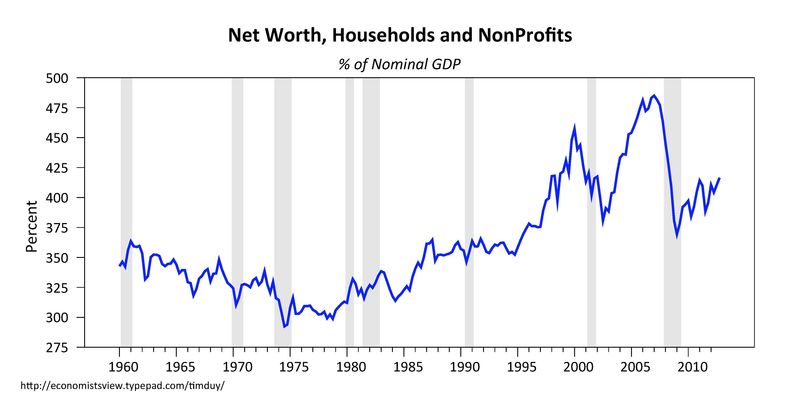

Are Asset Price Bubbles Needed to Make the US Economy Recover?

Are Asset Price Bubbles Needed to Make the US Economy Recover?22 Apr 2013

Quantitative Easing: The Fed Wants Americans to Continue Deficit Spending

Quantitative Easing: The Fed Wants Americans to Continue Deficit Spending13 Dec 2012