![]() What is New?

What is New?

-

Did the MMT Camp Correctly Predict the Post-Covid Economy?

What is the Mises Institute? The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private...

Read more » -

Word of the Day: Performative

-

In diesen Städten sind die #Mieten am stärksten gestiegen #wohnen #shorts

-

5 Entscheidungen, von denen Dein Wohlstand abhängt

-

Bayer Hauptversammlung: Damit müssen Aktionäre jetzt rechnen!

-

Help Us Publish These Three New Books

-

Low Time Preference Leads to Civilization

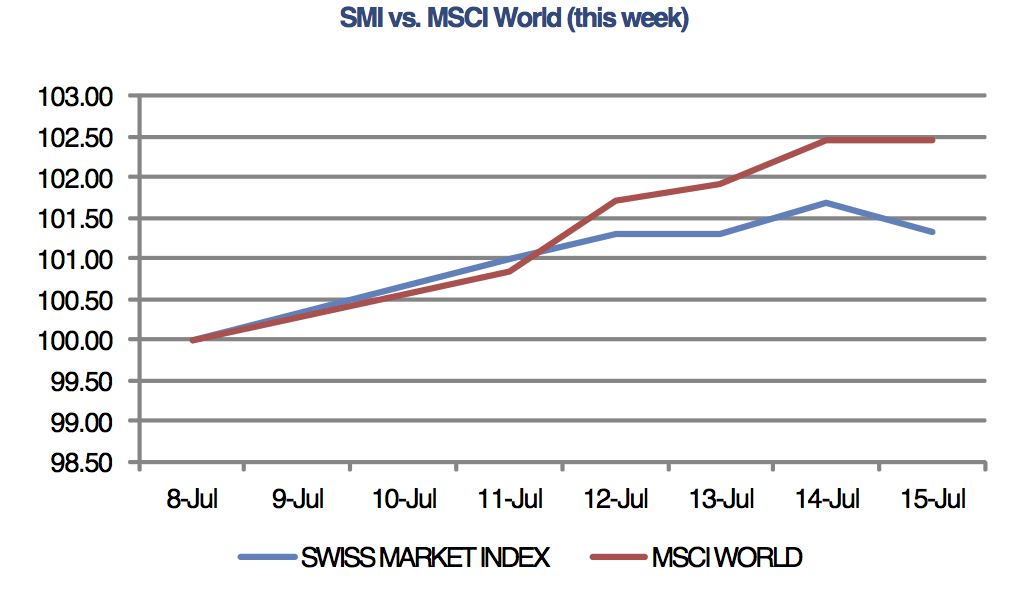

SNB and CHF

SNB and CHF

-

SNB Sight Deposits: increased by 3.4 billion francs compared to the previous week

The sight deposits at the SNB increased by 3.4 billion francs compared to the previous week.

Read more » -

USD/CHF stays above 0.9100 nearing the highs since October

-

Canadian Dollar remains vulnerable after strong US Retail Sales

-

Pound Sterling falls back as upbeat US Retail Sales strengthen US Dollar

-

2024-04-09 – Martin Schlegel: Interest rates and foreign exchange interventions: Achieving price stability in challenging times

-

2024-04-08 – Thomas Jordan: Towards the future monetary system

-

Swiss Franc at risk as inflation diverges from SNB forecasts

Swiss & European Macro

Swiss & European Macro

-

Brisant: Momentanes perfides Täuschungsmanöver läuft an – Ernst Wolff im Gespräch mit Krissy Rieger

Raus aus dem System? Aber wie? Trage dich zu unserem kostenlosen Report ein: https://www.rieger-consulting.com/riegersreport Mehr zu Krissy Rieger: Finanzkanal ►► / @chrisrieger91 Zweitkanal ►► / @krissy.rieger2 Instagram ►► https://www.instagram.com/krissy.rieg... Twitter ►► https://twitter.com/krissyrieger?lang=de Telegram ►► https://t.me/KrissyRieger ____________________ 📅 Alle Termine und die Links zu meiner Vortragsreihe finden...

Read more » -

Increase of 1.7% in nominal wages in 2023 and 0.4% decline in real wages

-

Diese Aktien sind extrem günstig!

-

Korrektur bei Aktien! Vorsicht!

-

Gold: Kursziel 5.092 US-Dollar?

-

Eskalation im Nahost-Konflikt als nächster Schwarzer Schwan für die Finanzmärkte?

-

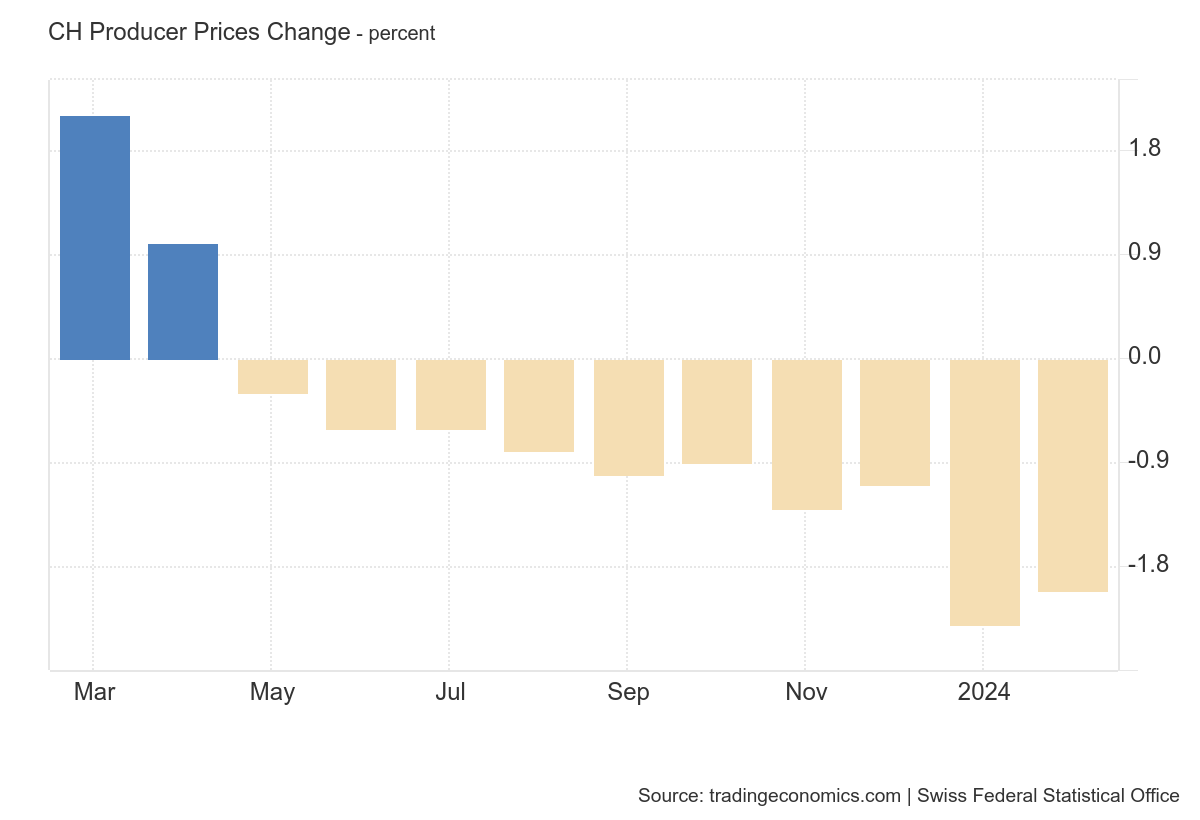

Producer and Import Price Index rose by 0.1% in March

Swiss Markets & News

Swiss Markets & News

-

SNB returns to quarterly profit thanks to Swiss franc weakness

The Swiss National Bank (SNB) returned to a quarterly profit because of the weakness of the Swiss franc, potentially helping officials to rebuild the central bank’s depleted capital base. The Zurich-based institution notched up a gain of CHF58.8 billion ($64 billion) in the first quarter, according to a statement on Thursday. That’s the strongest start to the year on record.

Read more » -

Luftfahrtindustrie: Rückblick auf 2023 und Prognose für 2024

-

Switzerland braced for wave of bank staff layoffs

-

UBS must build up more equity, says Swiss government

-

Switzerland’s Growing Online Gambling Ecosystem and the Rise of iGaming White Label Solutions

-

Investigation into collapse of Credit Suisse beset by delays

-

CEO pay: can Switzerland compete with the US?

Global Macro & Emerging Markets

Global Macro & Emerging Markets

-

Financial Forecast 2025-2032: Please Don’t Be Naive

Rather than attempt to evade Caesar's reach, a better strategy might be to 'go gray': blend in, appear average. Let's start by stipulating that I don't "like" this forecast. I'm not "talking my book" (for example, promoting nuclear power because I own shares in a uranium mine) or issuing this forecast because I favor it.

Read more » -

Weekly Market Pulse: Are Higher Interest Rates Good For The Economy?

-

Sound Money Vs. Fiat Currency: Trade and Credit Are the Wild Cards

-

Global Recession’s Winners and Losers

-

Who is “Europe’s last dictator”?

-

Rates, Risk and Debt: The Unavoidable Reckoning Ahead

-

How the Economy Changed: There’s No Bargains Left Anywhere

Austrian Economics

Austrian Economics

-

Did the MMT Camp Correctly Predict the Post-Covid Economy?

What is the Mises Institute? The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private...

Read more » -

Word of the Day: Performative

-

Help Us Publish These Three New Books

-

Low Time Preference Leads to Civilization

-

¿Cómo nos PROTEGEMOS ante una GUERRA?, con Gustavo Martínez

-

Opposing Military Intervention: Loving Dictators or Hating War?

-

Gold, Euro oder Dollar: Die Zukunft des Geldsystems | Anlageempfehlungen von Prof. Dr. Polleit

![]() Buy and Hold

Buy and Hold

-

In diesen Städten sind die #Mieten am stärksten gestiegen #wohnen #shorts

Die Mieten steigen fast überall. Aber wo am stärksten? Leo hat die Liste der Städte dabei, wo Wohnen sich am schnellsten verteuert. Quelle: Immowelt

Read more » -

5 Entscheidungen, von denen Dein Wohlstand abhängt

-

Retail Sales Data Suggests A Strong Consumer Or Does It

-

Hier ist Wohnen günstiger geworden

-

Schlechte Geldanlagen loswerden | Geld ganz einfach

-

Understanding Elliott Wave Theory and Investment Strategies – Andy Tanner and Bob Prechter

-

Die günstigsten Spritpreise Europas #shorts

![]() Crypto Währungen Deutsch

Crypto Währungen Deutsch

-

Bitcoin: Das darf JETZT NICHT passieren!

Da schaut man nichtsahnend am Sonntagmorgen auf den Bitcoin-Chart und stellt fest: Ein Crash bildet sich hier gerade aus! Wobei ich zugebe, Ich denke mal, ich weiß es noch gar nicht genau, der Titel des heutigen Videos wird irgendwas mit „Crash“ oder „Absturz“ drin haben.

Read more » -

BREAKING: Krypto-Preise auf dem Vormarsch? Ledger Drama enthüllt! Bitcoin Miami Highlights!

-

LEDGER RECOVERY DRAMA – DIESE 3 DINGE MUSST DU WISSEN!

-

DIE NEUSTEN TRENDS – WIE INVESTIEREN?

-

BITCOIN MIAMI KONFERENZ: BULLISCH ODER BÄRISCH?

-

CRASHT BITCOIN MIAMI WIEDER DEN PREIS?

-

FÜHREN ORDINALS ZU BITCOIN’S UNTERGANG?

![]() Crypto Currencies English

Crypto Currencies English

-

Launch of the Swiss4 Application, Combining Financial Services and Lifestyle

Swiss4, a financial player founded in Geneva in 2020, announces the launch of its application combining financial services and high-end lifestyle management services. Entirely designed, developed and hosted in Switzerland, the app guarantees security and ease of use for its customers, deposits in CHF held with the Swiss National Bank (SNB). The multi-currency account (CHF, EUR, GBP, AED, and SGD), alongside the MasterCard World Elite card,...

Read more » -

Swiss Fintech Awards 2024 Announce Top 10 Swiss Fintech Startups

-

Blackrock Launches Its First Tokenized Fund on Ethereum

-

Luzerner KB steigt in den den Handel und die Verwahrung von Kryptowährungen ein

-

US Spot Bitcoin ETFs Daily Trading Volume Soars to 6 Billion USD

-

SNB Study: Results of the Swiss Payment Methods Survey

-

The Top Swiss Law Firms for Fintech and Blockchain Practice

![]() Stock Picking & Dividends

Stock Picking & Dividends

-

Bayer Hauptversammlung: Damit müssen Aktionäre jetzt rechnen!

Zu meinen Onlinekursen: https://thomas-anton-schuster.coachy.net/lp/finanzielle-unabhangigkeit Vortrags- und Seminartermine, sowie kostenlose Anforderung des Aktienbewertungsblatts: https://aktienerfahren.de

Read more » -

Mario Voigt Dystopie: Entzug der Meinungsfreiheit!

-

Eilmeldung: FDP fordert nun Habeck Rücktritt!

-

Supergau für Jens Spahn wegen RKI Files!

-

BASF Hauptversammlung: DAS erwartet jetzt Anleger (2024)

-

Habeck Files: Die Grüne Kernschmelze!

-

Deutscher General: “Wir arbeiten an Operationsplan Deutschland”

![]() Mindset and Investing

Mindset and Investing

-

STARKES Umfeld, STARKE Renditen: Ein (Börsen-)Jahr voller Erfolg

Ein Jahr voller inspirierender Zusammenarbeit – unser Regionalleiter-Jubiläum! In diesem Vlog gibt es Einblicke hinter die Kulissen des Treffens und wir zeigen, wie Zusammenarbeit den Börsenerfolg fördert. Verpasse daher nicht die Highlights und lerne, wie auch du von unserer Academy profitieren kannst. http://jensrabe.de/regionalgruppen Vereinbare jetzt dein kostenfreies Beratungsgespräch: https://jensrabe.de/Q2Termin24 Tägliche Updates ab...

Read more » -

Der beste Hedge der Welt!

-

Sport mit Jens – 22042024 – SMCI, Bitcoin Halving, Trump vs. Biden

-

Einblick in unsere Livecalls (Video wird wieder gelöscht)

-

Mein YouTube Einnahmen: Totale Transparenz

-

UPDATE: Crash oder Korrektur – wie geht es jetzt weiter?

-

Geldmaschine Volatrading? Infos zum Reverse Split im UVXY

![]() Day Trading

Day Trading

-

Bodemann flippt aus: “Wir brauchen mehr Kontrolle”

Kostenfreier Live-Trading-Workshop (03.-05. Mai 2024): 👉 https://oliverklemmtrading.com/workshop?utm_source=youtube1&utm_campaign=workshop Jetzt anmelden! Plätze begrenzt... Klicke hier, um dich direkt gemeinsam mit Oli unabhängig zu machen 👉 https://oliverklemmtrading.com/apply-now-1?utm_source=youtube&utm_medium=social&utm_campaign=tradingcoacholi&utm_term=morning-news&utm_content=2 ►Folge Oliver auf Instagram:...

Read more » -

Wichtige Morning News mit Oliver Klemm #288

-

Wichtige Morning News mit Oliver Klemm #289

-

Eklat im Bundestag: “Wir müssen die FDP stoppen”

-

Wichtige Morning News mit Oliver Klemm #287

-

Wichtige Morning News mit Oliver Klemm #286

-

Eilt: dramatische Wende im Ukraine-Konflikt!

![]() Fund and Hedge Funds

Fund and Hedge Funds

-

Happy World Book Day!

Happy World Book Day! Do some reading today, see what you like. #raydalio #principles #worldbookday #worldbookday2024 #reading #education #books

Read more » -

This is why we NEED to Protect the Ocean

-

How the World can Tackle Climate Change

-

Climate Change Efforts Must Be Practical and the Time is NOW

-

THIS is what it will cost to fight Climate Change

-

Ray Dalio on Stock Trading at 12 Years Old

-

Ray Dalio on his Principles for Success

Gold and Monetary Metals

Gold and Monetary Metals

-

Gold Price Just Dropped! What Happened? (2024 Update)

The #gold price recently experienced its most significant intraday loss in nearly two years, prompting questions about its trajectory and its status as an investment. In this video, we delve into the reasons behind the drop and whether gold remains a viable investment option. Despite the recent pullback, we maintain our bullish outlook on gold. Pullbacks are a natural part of a long-term uptrend, and historical patterns suggest that gold may...

Read more » -

Who’s to Blame for Inflation?

-

Will gold prices keep rising in 2024? #gold #inflation #goldprice #preciousmetals

-

2024 Gold Forecast: What Investors Need to Know

-

Sound Money Talks – A Conversation With Jeff Deist and Jp Cortez

-

Is the gold price too high to buy?

-

10oz STACKER Bars

FX Trends

FX Trends

-

EURUSD Technical Analysis – WATCH what happens around this key resistance

#eurusd #forex #technicalanalysis In this video you will learn about the latest fundamental developments for the EURUSD pair. You will also find technical analysis across different timeframes for a better overall outlook on the market. ---------------------------------------------------------------------- Topics covered in the video: 0:00 Fundamental Outlook. 1:20 Technical Analysis with Optimal Entries. 3:02 Upcoming Economic Data....

Read more » -

EURUSD has a cap near the 38.2% retracement, but buyers are pushing.

-

AUDUSD reacts to the weaker US data. Pair moves higher as yields move lower/stocks higher.

-

The USDCHF is not doing much in trading today, but the buyers are trying to take control.

-

The USDCHF is not doing much in trading today, but the buyers are trying to take control

-

Kickstart the FX trading day for April 23 w/a technical look at EURUSD, USDJPY and GBPUSD

-

USDJPY Technical Analysis – Key levels to watch for a pullback

![]() Personal Investment

Personal Investment

-

In diesen Städten sind die #Mieten am stärksten gestiegen #wohnen #shorts

Die Mieten steigen fast überall. Aber wo am stärksten? Leo hat die Liste der Städte dabei, wo Wohnen sich am schnellsten verteuert. Quelle: Immowelt

Read more » -

5 Entscheidungen, von denen Dein Wohlstand abhängt

-

Bayer Hauptversammlung: Damit müssen Aktionäre jetzt rechnen!

-

Mario Voigt Dystopie: Entzug der Meinungsfreiheit!

-

Retail Sales Data Suggests A Strong Consumer Or Does It

-

Eilmeldung: FDP fordert nun Habeck Rücktritt!

-

Supergau für Jens Spahn wegen RKI Files!