Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

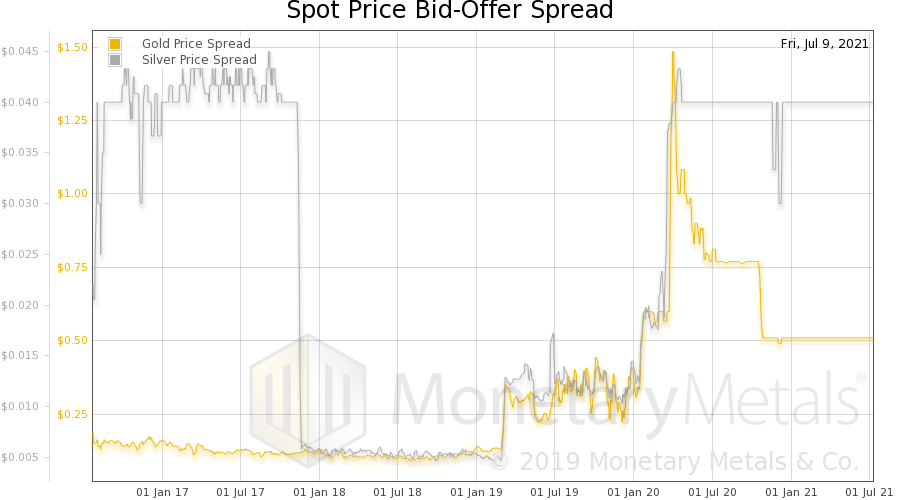

Basel III’s Effect on Gold and Silver

Basel III’s Effect on Gold and Silver13 Jul 2021

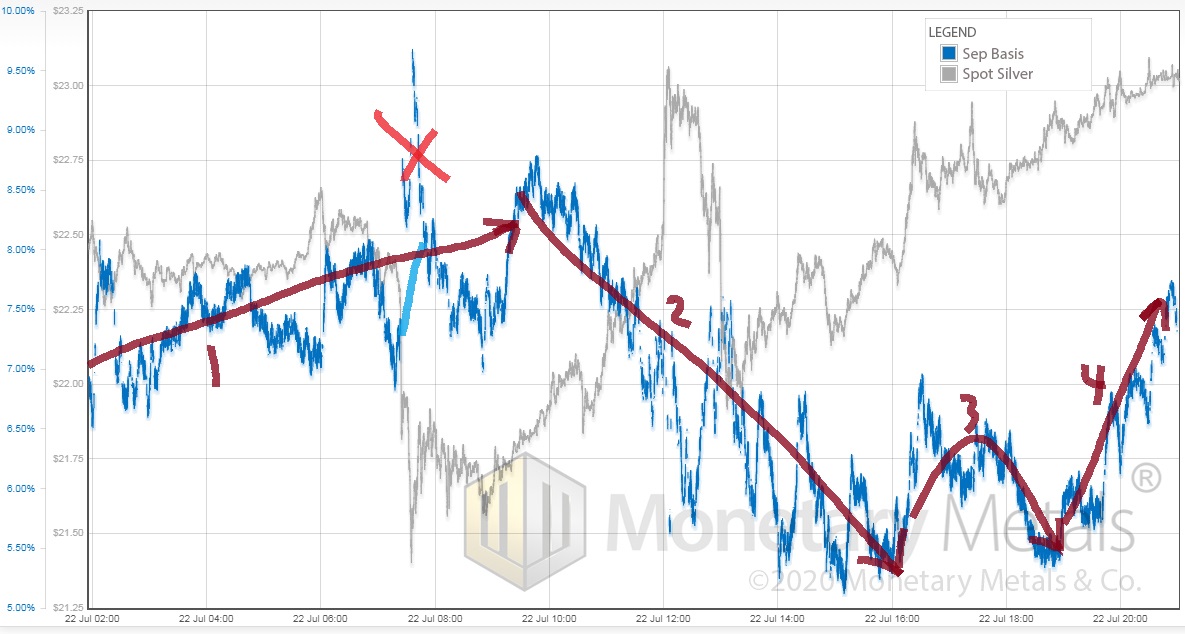

One of These Silver Days is Not Like the Other, 23 July

One of These Silver Days is Not Like the Other, 23 July24 Jul 2020

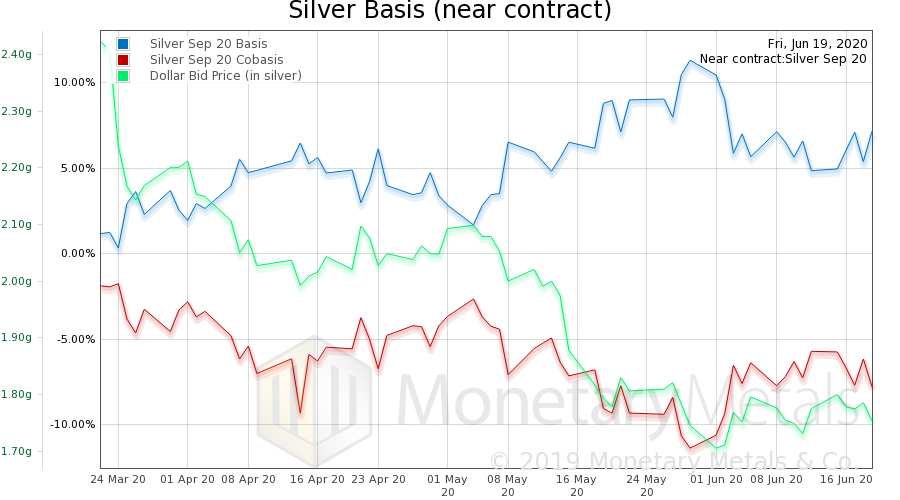

Defaults Are Coming, Market Report, 22 June

Defaults Are Coming, Market Report, 22 June23 Jun 2020

When Is a Capital Gain Capital Consumption? Market Report, 25 May

When Is a Capital Gain Capital Consumption? Market Report, 25 May26 May 2020

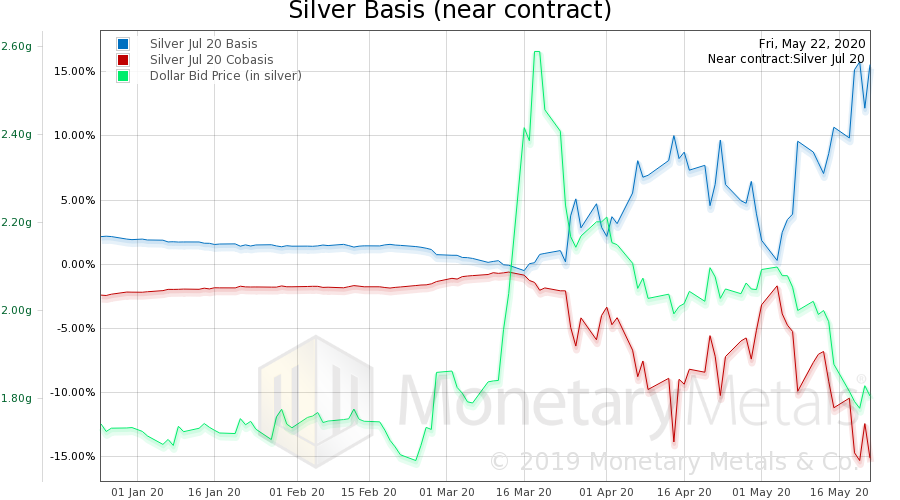

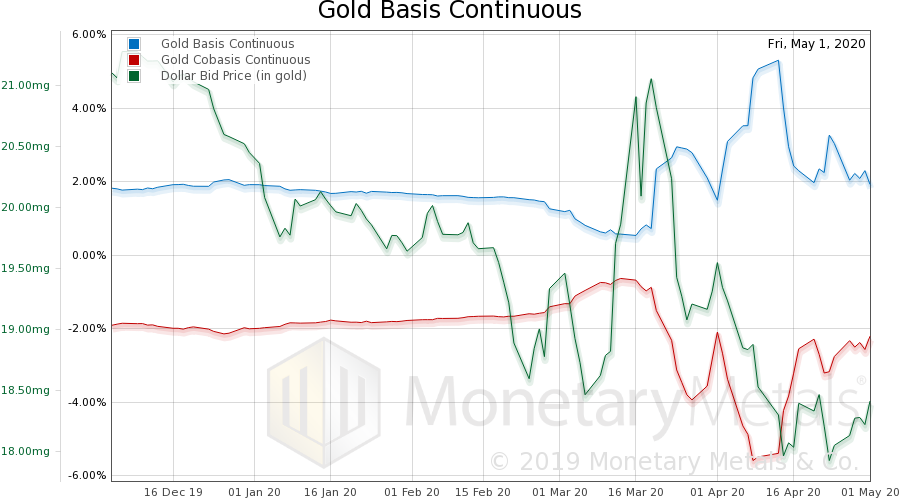

Gold and Silver Markets Start to Normalize, Report 4 May

Gold and Silver Markets Start to Normalize, Report 4 May5 May 2020

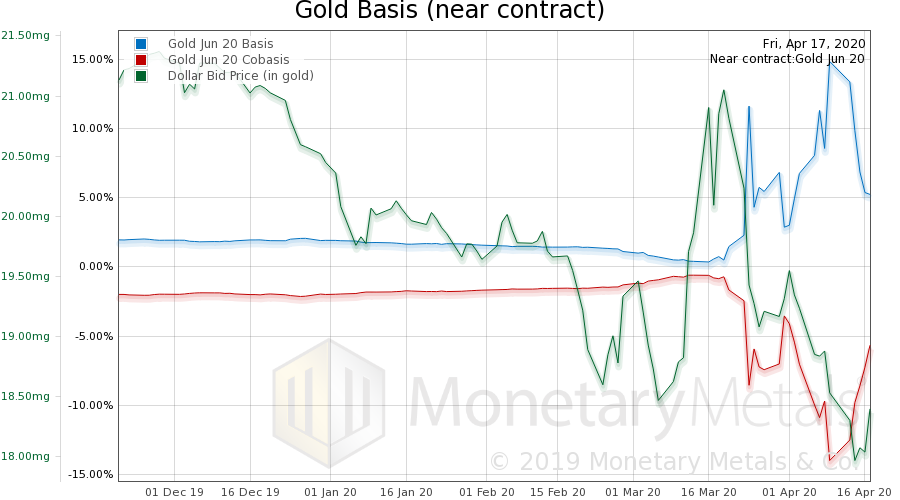

Crouching Silver, Hidden Oil Market Report 20 Apr

Crouching Silver, Hidden Oil Market Report 20 Apr21 Apr 2020

Silver Backwardation Returns, Gold and Silver Market Report 2 March

Silver Backwardation Returns, Gold and Silver Market Report 2 March2 Mar 2020

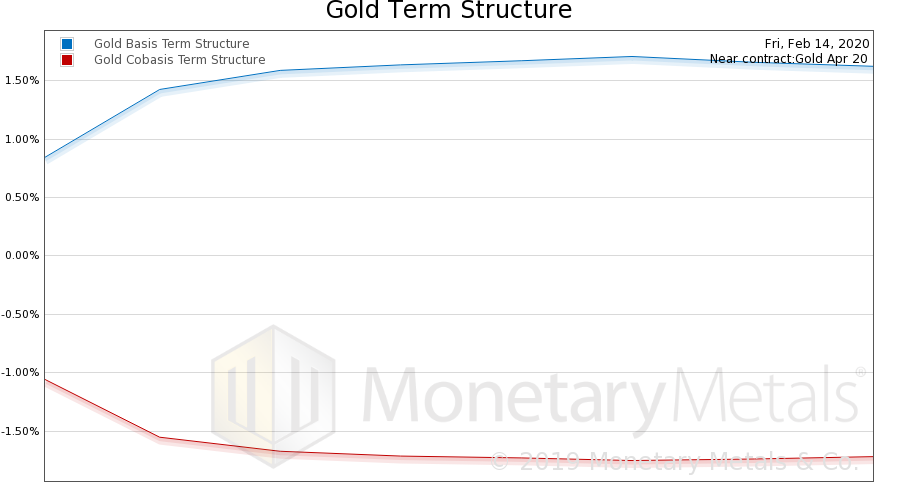

Widening Bid-Ask Spreads, Gold and Silver Market Report 17 February

Widening Bid-Ask Spreads, Gold and Silver Market Report 17 February17 Feb 2020

Wealth Consumption vs. Growth – Precious Metals Supply and Demand

Wealth Consumption vs. Growth – Precious Metals Supply and Demand3 Jan 2020

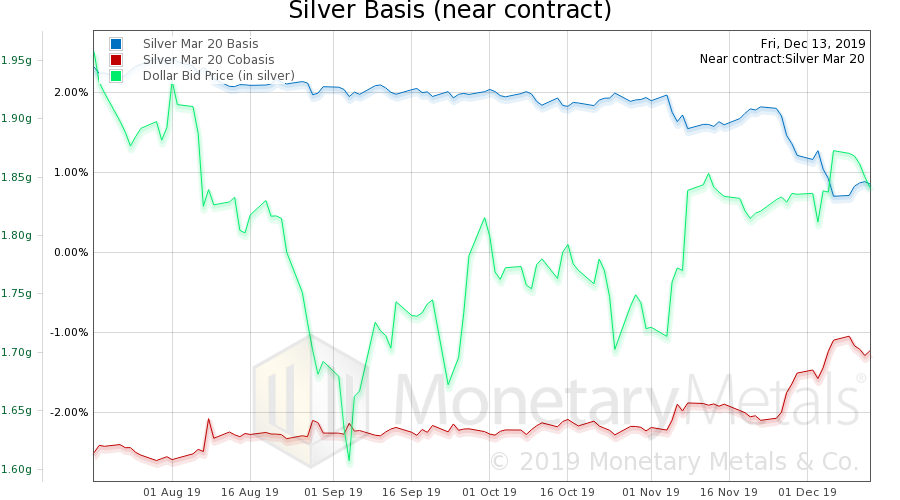

Open Letter to John Taft, Report 17 Dec

Open Letter to John Taft, Report 17 Dec18 Dec 2019

The End of an Epoch, Report 8 Dec

The End of an Epoch, Report 8 Dec10 Dec 2019

Money and Prices Are a Dynamic System, Report 1 Dec

Money and Prices Are a Dynamic System, Report 1 Dec3 Dec 2019

Raising Rates to Fight Inflation, Report 24 Nov

Raising Rates to Fight Inflation, Report 24 Nov26 Nov 2019

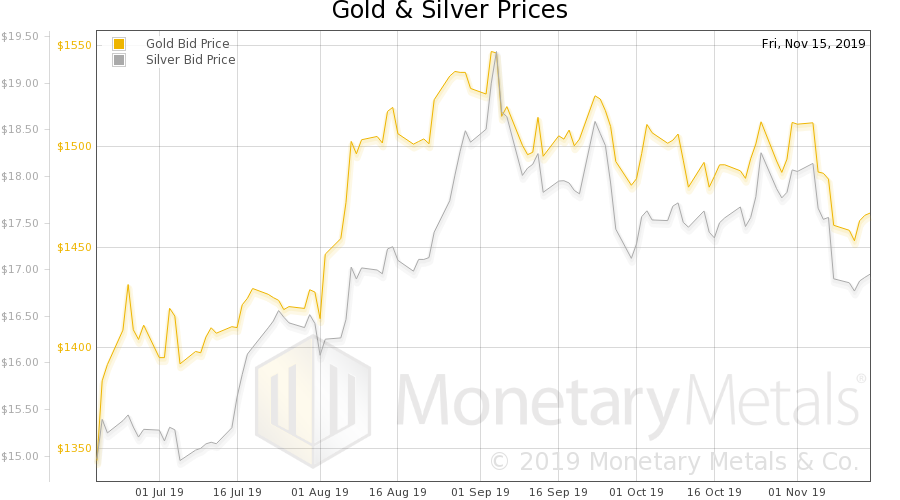

The Perversity of Negative Interest, Report 17 Nov

The Perversity of Negative Interest, Report 17 Nov18 Nov 2019

What’s the Price of Gold in the Gold Standard, Report 10 Nov

What’s the Price of Gold in the Gold Standard, Report 10 Nov12 Nov 2019

Targeting nGDP Targeting, Report 3 Nov

Targeting nGDP Targeting, Report 3 Nov5 Nov 2019

Bitcoin Myths, Report 27 Oct

Bitcoin Myths, Report 27 Oct28 Oct 2019

Wealth Accumulation Is Becoming Impossible, Report 20 Oct

Wealth Accumulation Is Becoming Impossible, Report 20 Oct22 Oct 2019

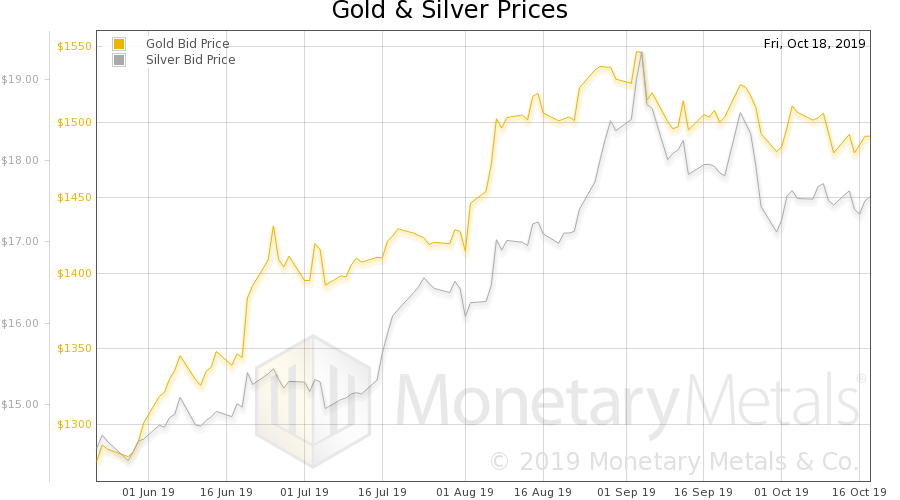

Motte and Bailey Fallacy, Report 13 Oct

Motte and Bailey Fallacy, Report 13 Oct15 Oct 2019

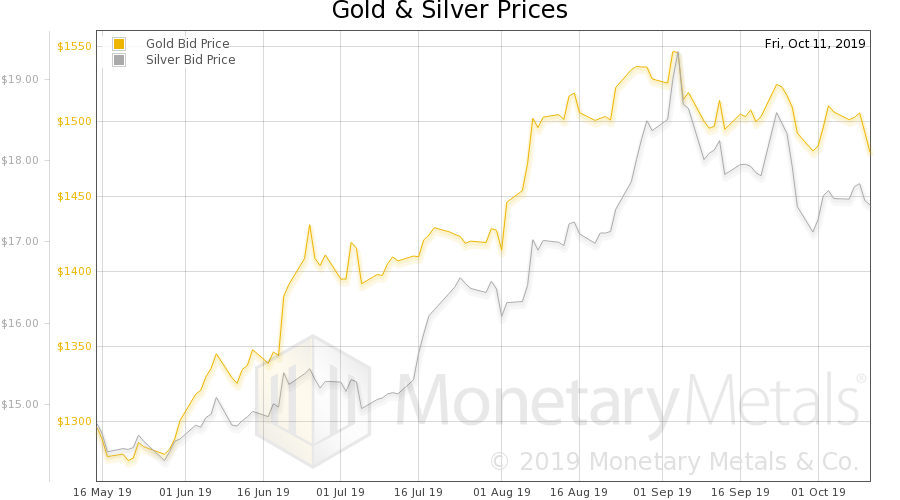

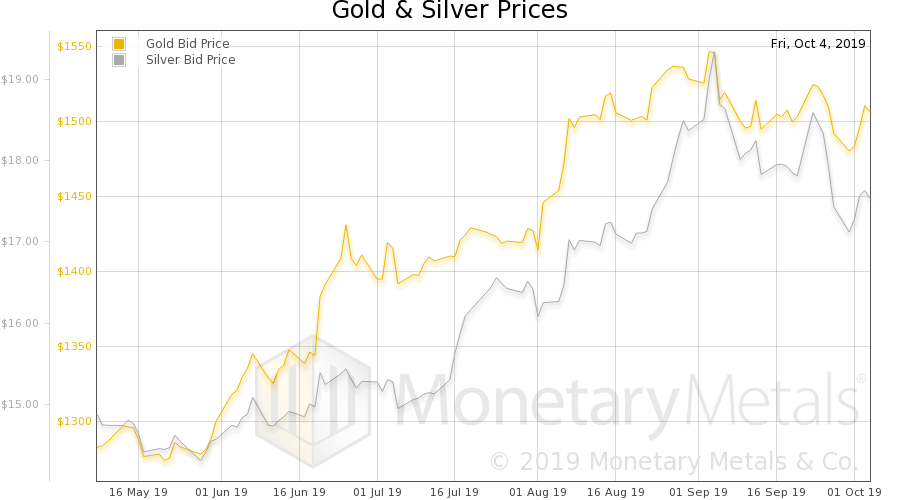

A Wealth Tax Consumes Capital, Report 6 Oct

A Wealth Tax Consumes Capital, Report 6 Oct7 Oct 2019