Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Inching Closer To Another Warning, This One From Japan

Inching Closer To Another Warning, This One From Japan20 Jul 2021

Anyone Remember That Whole SLR Cliff?2 Jul 2021

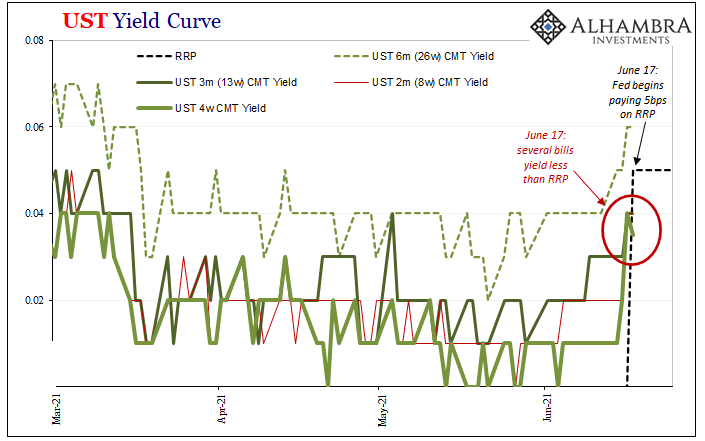

The FOMC Accidentally Exposes Itself (Reverse Repo-style)18 Jun 2021

Rechecking On Bill And His Newfound Followers9 Apr 2021

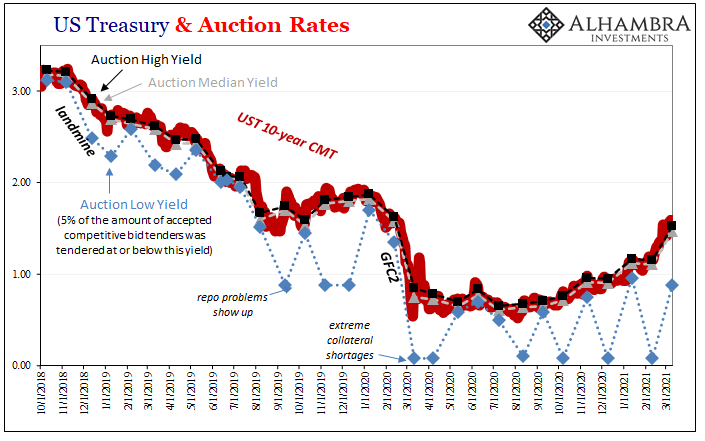

What Gold Says About UST Auctions11 Mar 2021

What Might Be In *Another* Market-based Yield Curve Twist?23 Feb 2021

Seizing The Dirt Shirt Title6 Jan 2021

Japan’s Bellwether On Nasty #425 Jun 2019

Fear Or Reflation Gold?4 Feb 2019

Insight Japan16 Jan 2019

China Now Japan; China and Japan3 Nov 2018

‘Mispriced’ Bonds Are Everywhere2 Sep 2018

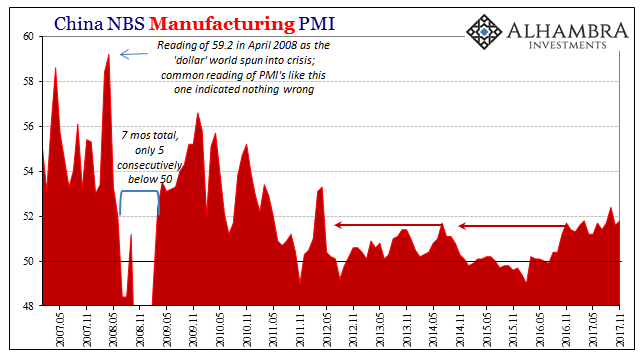

What China’s Trade Conditions Say About The Right Side Of ‘L’12 May 2018

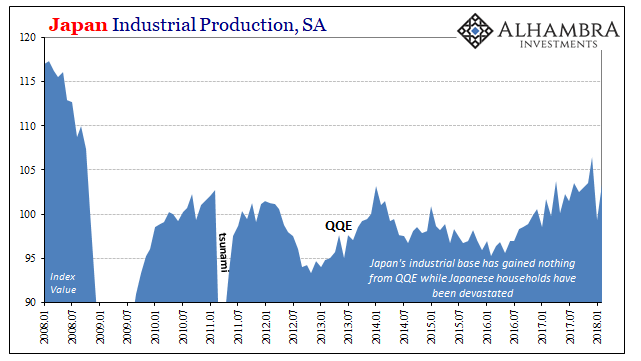

The Best ‘Reflation’ Indicator May Be Japanese4 Apr 2018

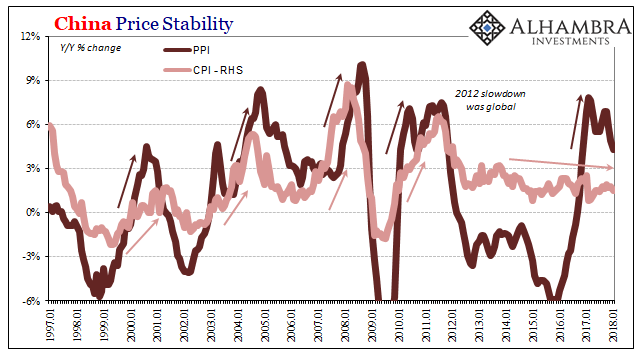

China: Inflation? Not Even Reflation16 Feb 2018

Three Years Ago QE, Last Year It Was China, Now It’s Taxes13 Dec 2017

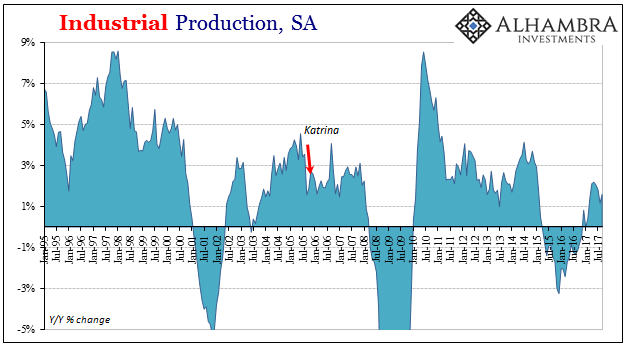

Broader Slowing in Industrial Production20 Oct 2017

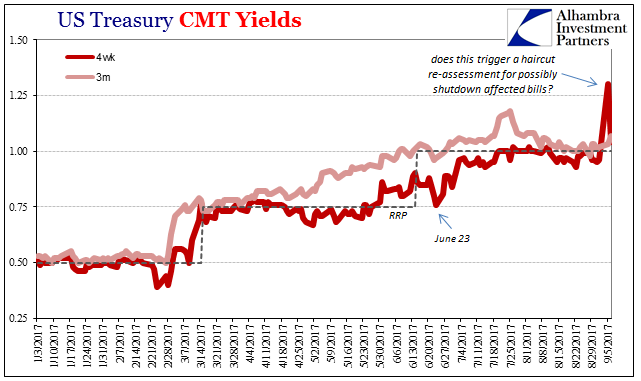

It Was Collateral, Not That We Needed Any More Proof30 Sep 2017

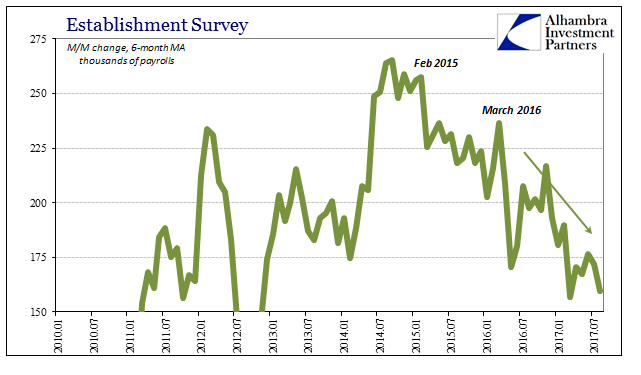

2017 Is Two-Thirds Done And Still No Payroll Pickup7 Sep 2017

Deja Vu1 Sep 2017