Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

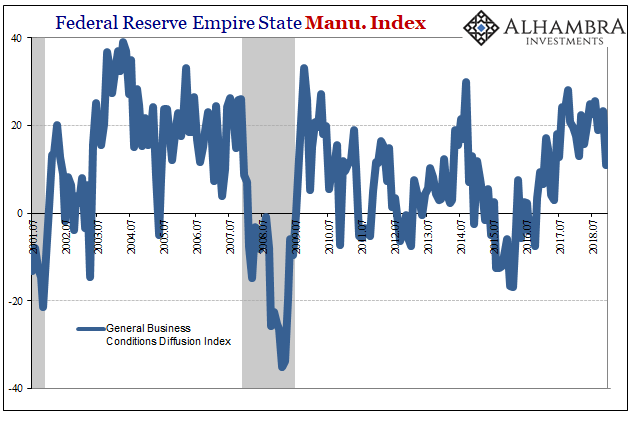

Weekly Market Pulse: Tune Out The Noise

Weekly Market Pulse: Tune Out The Noise24 Feb 2025

Busy Wednesday: French Confidence Vote, Fed’s Powell Speaks, ADP Jobs Estimate, and Beige Book

Busy Wednesday: French Confidence Vote, Fed’s Powell Speaks, ADP Jobs Estimate, and Beige Book4 Dec 2024

French Government on Precipice, Presses Euro Lower

French Government on Precipice, Presses Euro Lower2 Dec 2024

Yen Jumps on Rate Hike Speculation

Yen Jumps on Rate Hike Speculation27 Nov 2024

Euro and Sterling are Trying to Stabilize after Sharp Drop on Back of Disappointing Flash PMI

Euro and Sterling are Trying to Stabilize after Sharp Drop on Back of Disappointing Flash PMI22 Nov 2024

Turn Around Tuesday Comes Late

Turn Around Tuesday Comes Late24 Oct 2024

Mortgage Relief Lifts China’s CSI 300 by more than 8% Ahead of the Golden Week Holiday

Mortgage Relief Lifts China’s CSI 300 by more than 8% Ahead of the Golden Week Holiday30 Sep 2024

Dollar Consolidates as Stocks Melt

Dollar Consolidates as Stocks Melt4 Sep 2024

The Dollar is Bid but Ueda Lends Support to the Yen

The Dollar is Bid but Ueda Lends Support to the Yen3 Sep 2024

The Dollar and Rates Come Back Firmer

The Dollar and Rates Come Back Firmer22 Aug 2024

Dollar Losses Extended, Led by the Japanese Yen

Dollar Losses Extended, Led by the Japanese Yen19 Aug 2024

Greenback and Yen Extend Gains

Greenback and Yen Extend Gains24 Jul 2024

Short Covering Squeezes the Yen Higher

Short Covering Squeezes the Yen Higher23 Jul 2024

Dollar Mixed as Markets Digest US Political Developments

Dollar Mixed as Markets Digest US Political Developments22 Jul 2024

After Hawkish FOMC Minutes, the Dollar Comes Back Softer

After Hawkish FOMC Minutes, the Dollar Comes Back Softer23 May 2024

Risk On, Dollar Sold

Risk On, Dollar Sold22 Feb 2024

The US Dollar and Rates Rise Further

The US Dollar and Rates Rise Further5 Feb 2024

BOJ Stands Pat, Exit Draws Closer, while HK Liquidity is Squeezed Easing Pressure on the Yuan

BOJ Stands Pat, Exit Draws Closer, while HK Liquidity is Squeezed Easing Pressure on the Yuan23 Jan 2024

Softer Tokyo CPI Buys BOJ Time while Moody’s Cuts the Outlook for China’s Debt following Fiscal Stimulus and the Continued Property Slump

Softer Tokyo CPI Buys BOJ Time while Moody’s Cuts the Outlook for China’s Debt following Fiscal Stimulus and the Continued Property Slump5 Dec 2023

Corrective Forces Help the Dollar Stabilize

Corrective Forces Help the Dollar Stabilize22 Nov 2023