Read More »

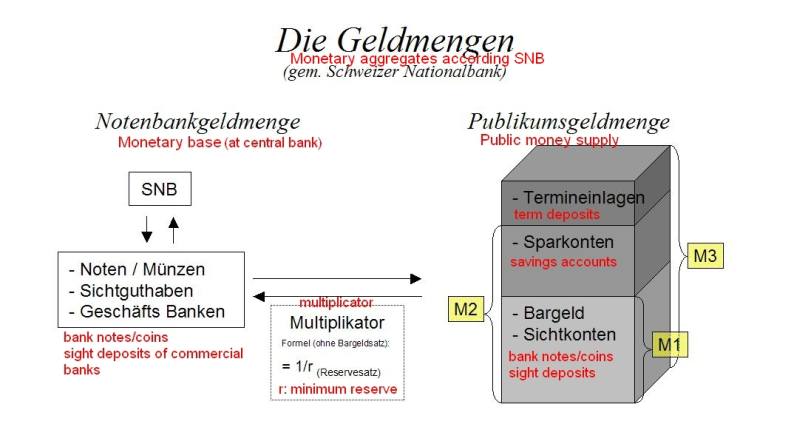

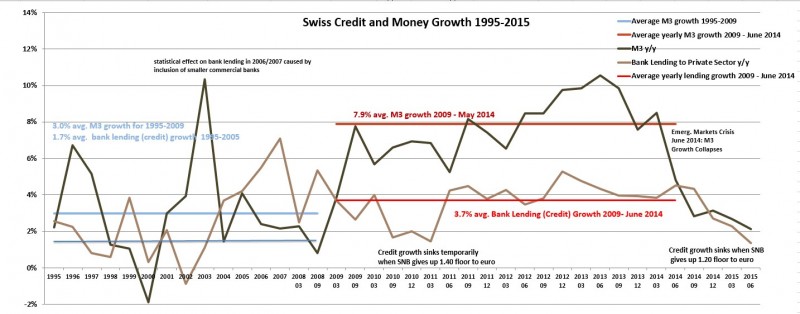

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

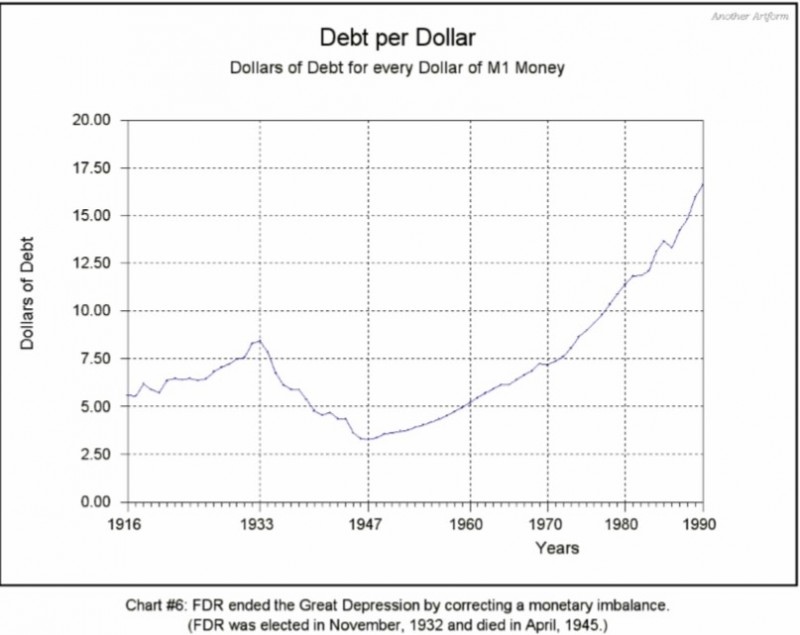

Taper Discretion Means Not Loving Payrolls Anymore

Taper Discretion Means Not Loving Payrolls Anymore10 Jan 2022

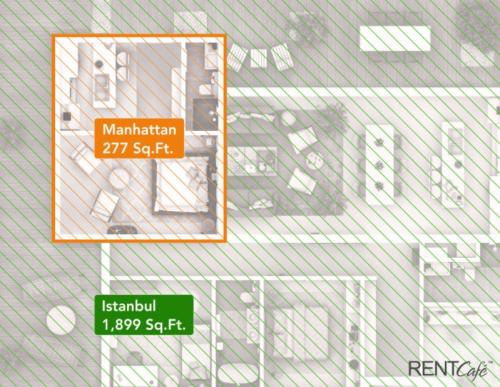

How Much Space Does $1,500 Rent In The World’s ‘Most Magnetic’ Cities?28 Sep 2017

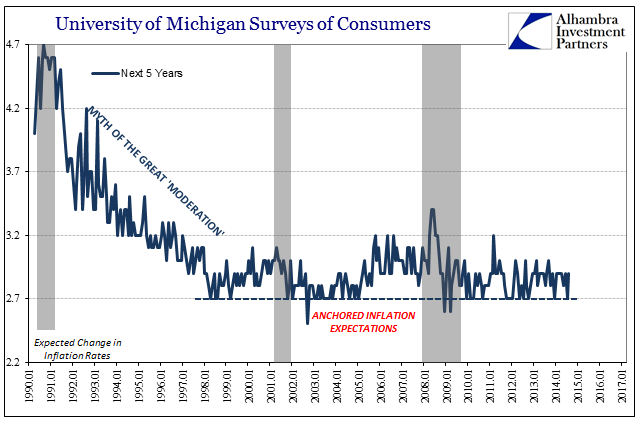

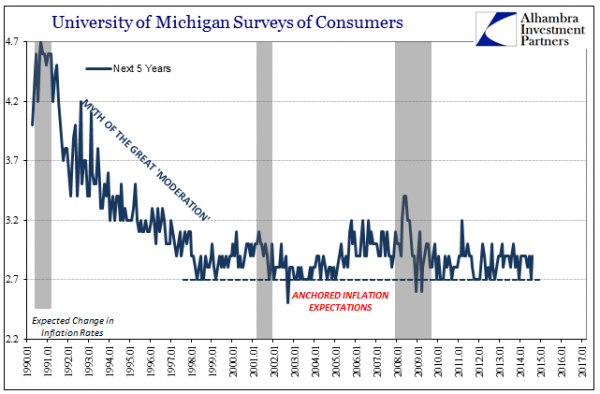

Further Unanchoring Is Not Strictly About Inflation

Further Unanchoring Is Not Strictly About Inflation18 Mar 2017

Global Risk Off: China Reenters Bear Market, Oil Tumbles Under $30; Global Stocks, US Futures Gutted15 Jan 2016

Will the Dollar Appreciate on higher U.S. Savings and a Smaller Trade Deficit?12 Jul 2014

Who Has Got the Problem? Europe or Japan?23 Oct 2012