Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

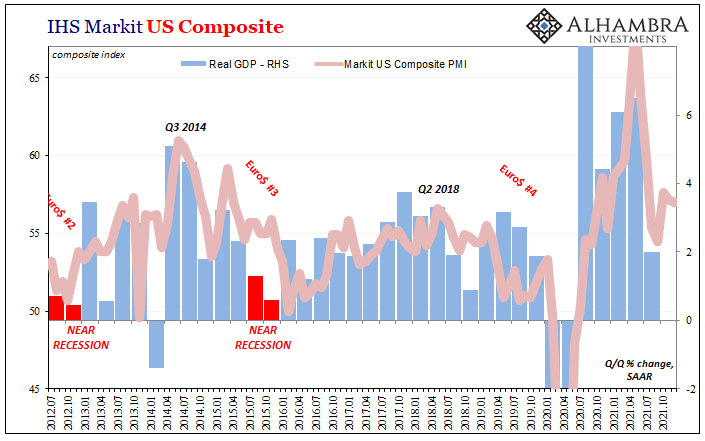

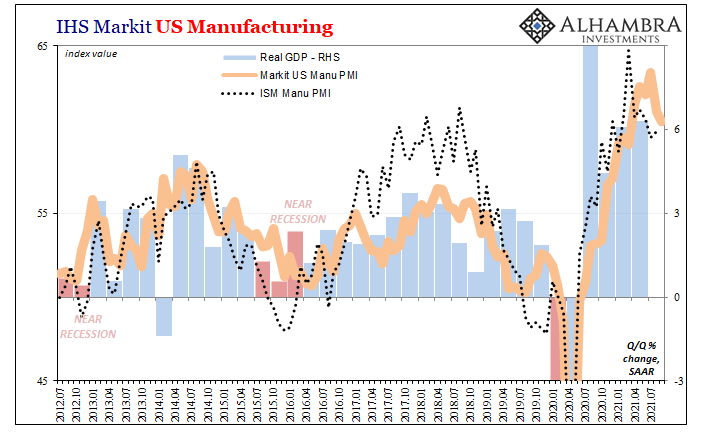

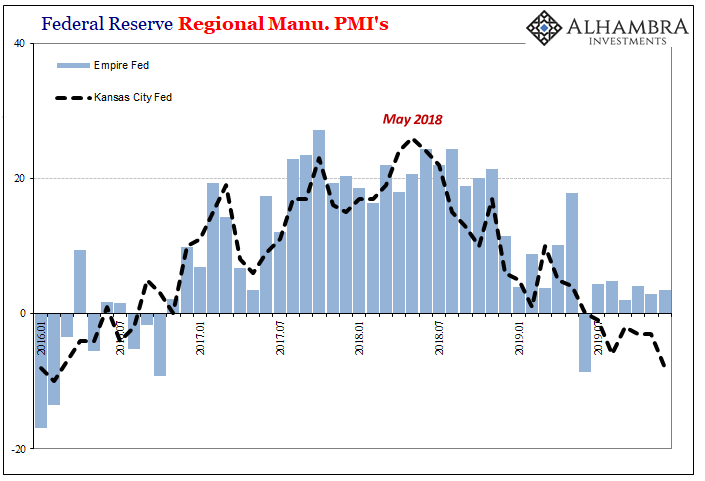

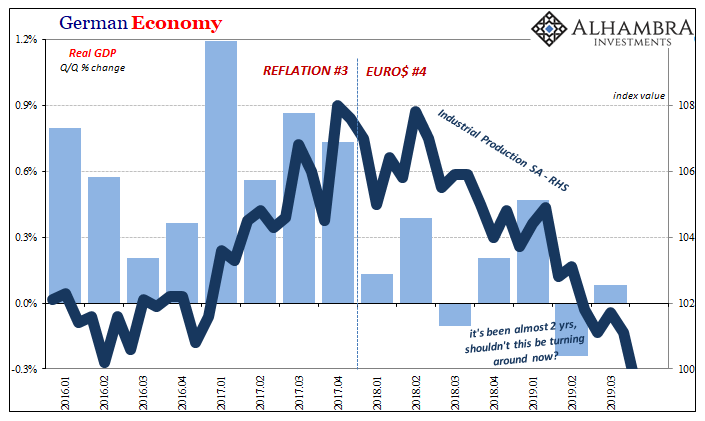

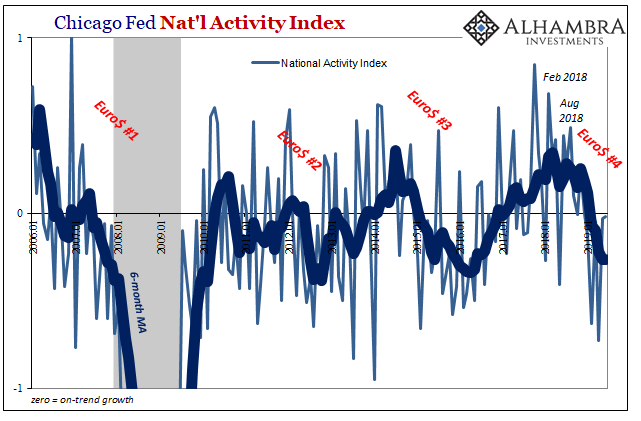

As The Fed Seeks To Justify Raising Rates, Global Growth Rates Have Been Falling Off Uniformly Around The World

As The Fed Seeks To Justify Raising Rates, Global Growth Rates Have Been Falling Off Uniformly Around The World8 Jan 2022

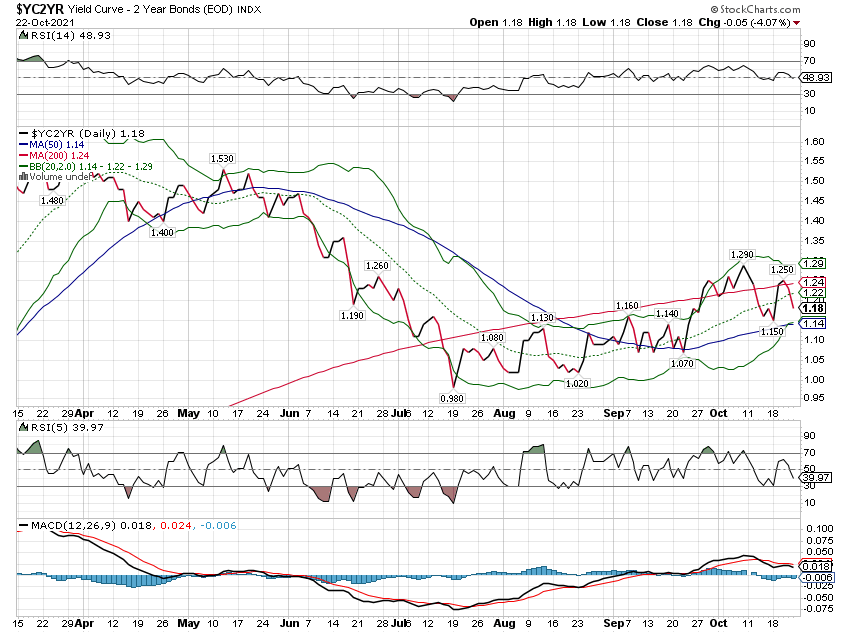

Weekly Market Pulse: Inflation Scare!

Weekly Market Pulse: Inflation Scare!25 Oct 2021

All Eyes On Inventory24 Sep 2021

US Stall? Only Half The Imagined “V” May Indicate One, Too27 Jul 2020

Manufacturing Clears Up Bond Yields7 Jan 2020

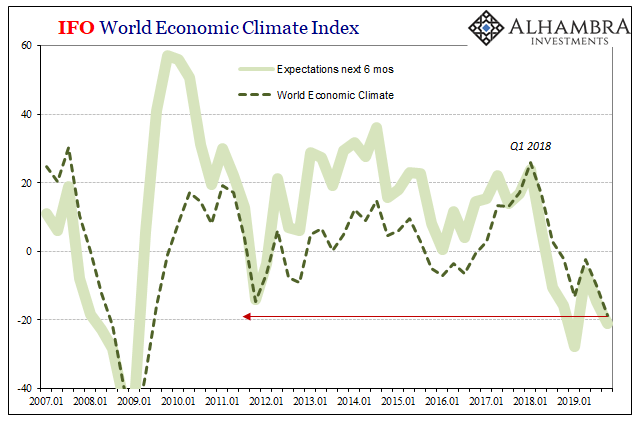

Latest European Sentiment Echoes Draghi’s Last Take On Global Economic Risks19 Dec 2019

QE’s and Rate Cuts: Two Very Different Sets of Sentiment Drawn From Them17 Nov 2019

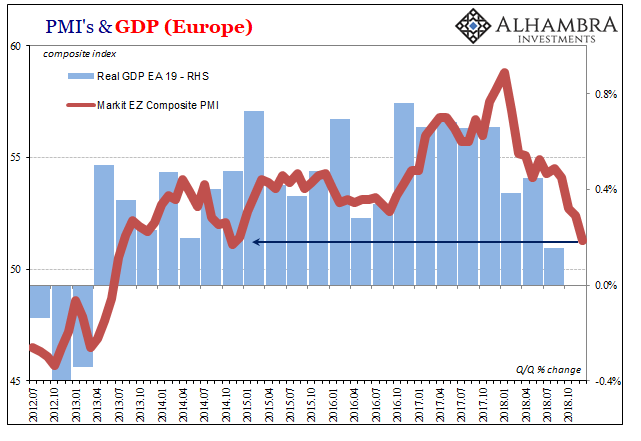

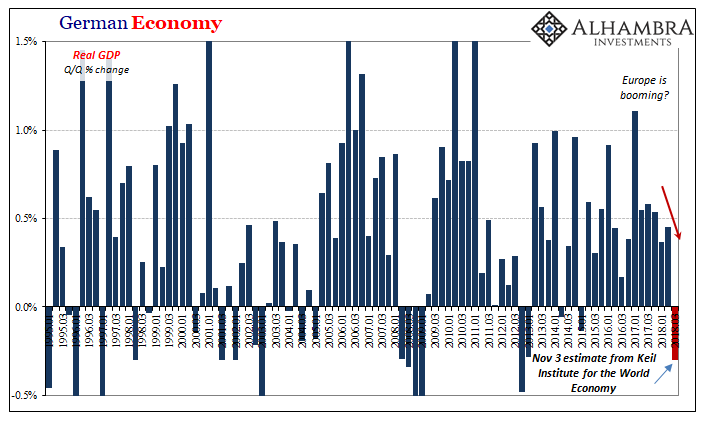

Somehow Still Decent European Descent

Somehow Still Decent European Descent28 Oct 2019

More Down In The Downturn25 Oct 2019

No Longer Hanging In, Europe May Have (Been) Broken Down24 Sep 2019

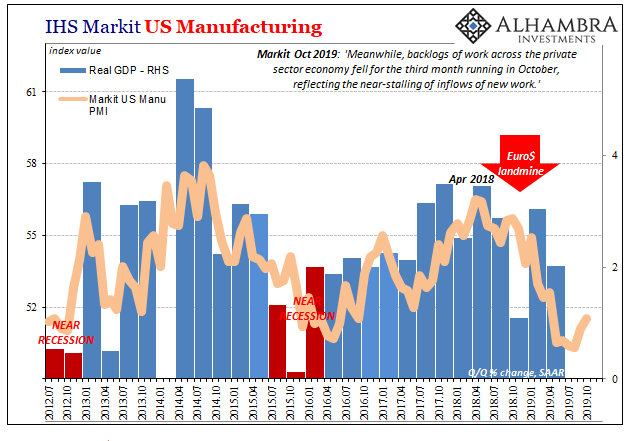

US Economic Crosscurrents Reach the 50 Mark27 Jul 2019

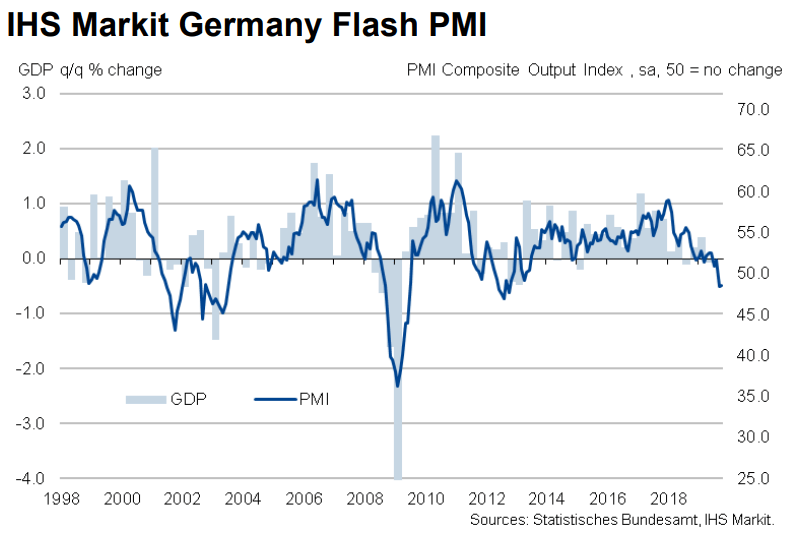

Germany Struggles On25 Jul 2019

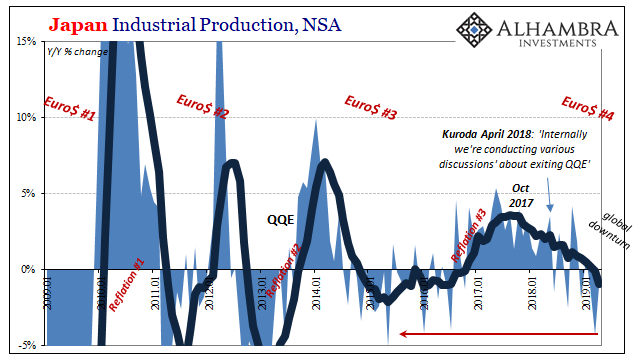

Japan’s Bellwether On Nasty #425 Jun 2019

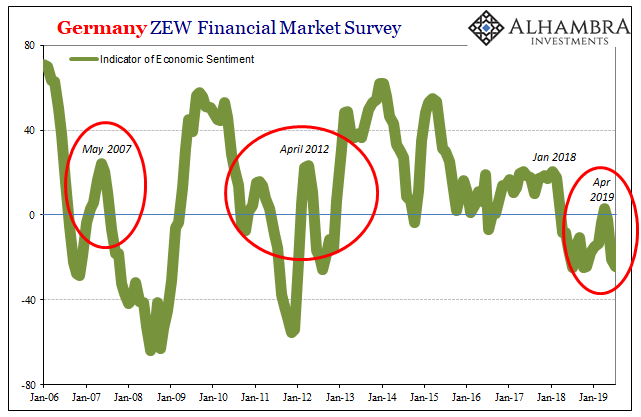

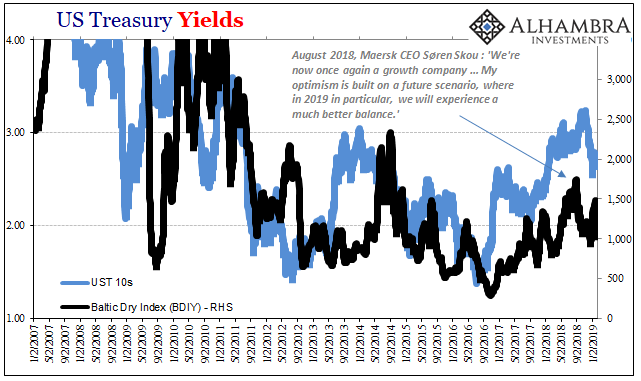

Sinking Shippers Signal Global Goods Troubles24 Feb 2019

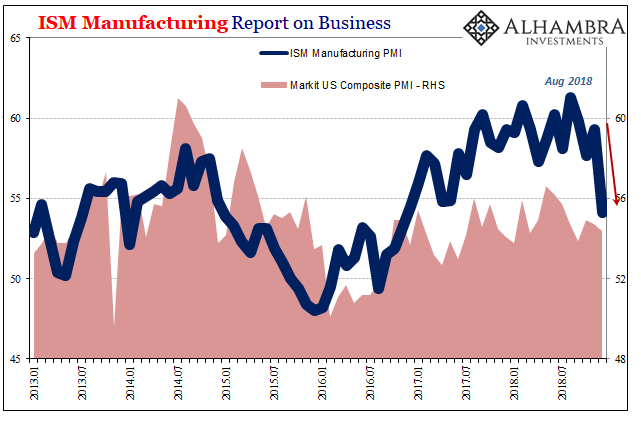

If You’ve Lost The ISM…9 Jan 2019

Just In Time For The Circus26 Dec 2018

The Direction Is (Globally) Clear29 Nov 2018

Harmful Modern Myths And Legends8 Nov 2018

Global PMI’s Hang In There And That’s The Bad News25 Aug 2018

The Currency of PMI’s27 May 2018