Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

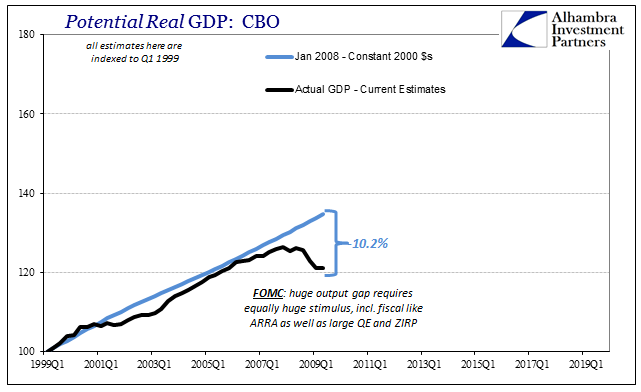

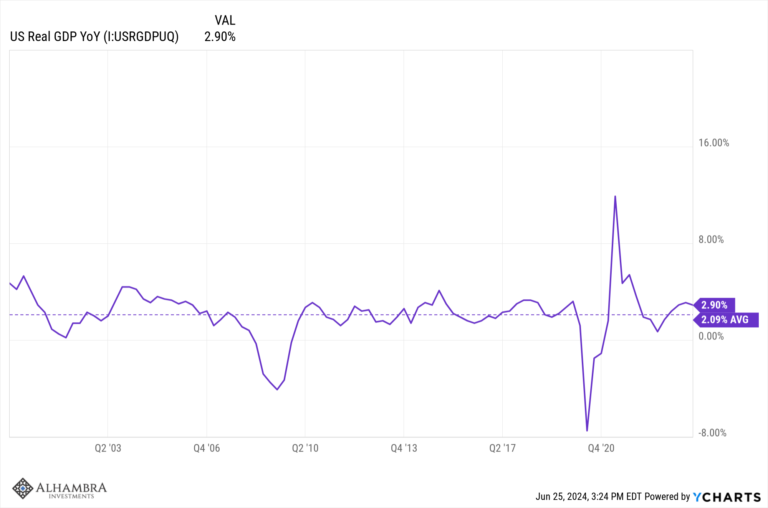

Weekly Market Pulse: The Turkey Leg

Weekly Market Pulse: The Turkey Leg23 Jun 2025

Markets do Cartwheels in Response to Traditional Pick for US Treasury Secretary

Markets do Cartwheels in Response to Traditional Pick for US Treasury Secretary25 Nov 2024

Fragile and Consolidative Tone Starts the Week in FX

Fragile and Consolidative Tone Starts the Week in FX18 Nov 2024

Searching for Direction

Searching for Direction8 Nov 2024

Serenity Now

Serenity Now7 Nov 2024

Stocks Higher, Dollar Lower: Post-Fed

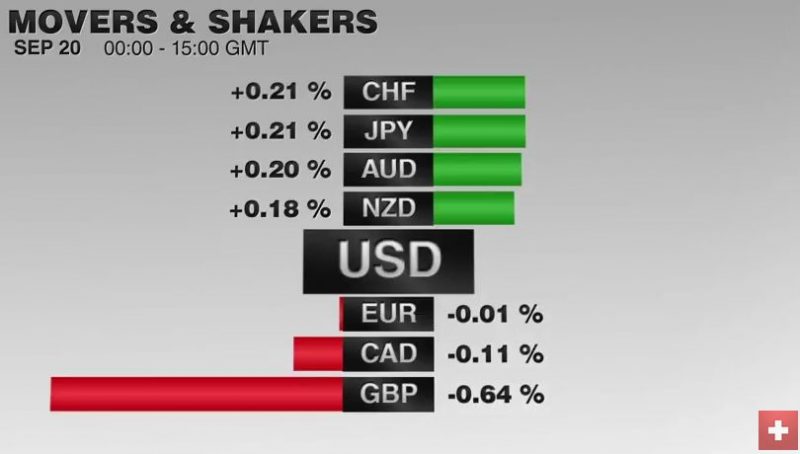

Stocks Higher, Dollar Lower: Post-Fed19 Sep 2024

Greenback Continues to Trade Heavily amid Heightened Speculation of a 50 bp Cut Wednesday

Greenback Continues to Trade Heavily amid Heightened Speculation of a 50 bp Cut Wednesday16 Sep 2024

Heightened Speculation that Fed may Cut 50 bp Next Week Sends the Dollar Lower

Heightened Speculation that Fed may Cut 50 bp Next Week Sends the Dollar Lower13 Sep 2024

Consolidative Tuesday

Consolidative Tuesday10 Sep 2024

The Dollar and Rates Come Back Firmer

The Dollar and Rates Come Back Firmer22 Aug 2024

US Benchmark Payroll Revisions Over-Hyped? Dollar may Benefit from Buying on Fact after Being Sold on Rumors

US Benchmark Payroll Revisions Over-Hyped? Dollar may Benefit from Buying on Fact after Being Sold on Rumors21 Aug 2024

Is the US CPI Anti-Climactic?

Is the US CPI Anti-Climactic?14 Aug 2024

Subdued Market Compared to a Week Ago: Is the Dramatic Position Unwinding Over?

Subdued Market Compared to a Week Ago: Is the Dramatic Position Unwinding Over?12 Aug 2024

Consolidation Featured

Consolidation Featured8 Aug 2024

BOJ Delivers, Sending Greenback to Almost JPY150; Now Over to the Federal Reserve

BOJ Delivers, Sending Greenback to Almost JPY150; Now Over to the Federal Reserve31 Jul 2024

Market Boosts Odds of a BOE Rate Cut this Week

Market Boosts Odds of a BOE Rate Cut this Week29 Jul 2024

Q3 Cyclical Outlook

Q3 Cyclical Outlook25 Jun 2024

Self-Inflicted Wounds in Europe and Japan Help the Greenback Shrug Off the Drag of Lower Rates

Self-Inflicted Wounds in Europe and Japan Help the Greenback Shrug Off the Drag of Lower Rates14 Jun 2024

Dollar Comes Back Bid

Dollar Comes Back Bid13 Jun 2024

UK CPI Disappoints

UK CPI Disappoints22 May 2024