Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

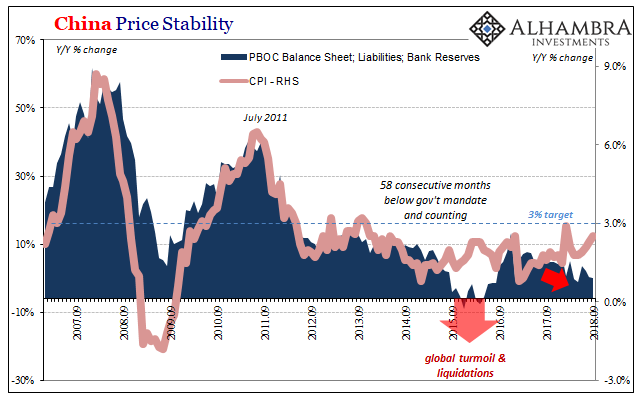

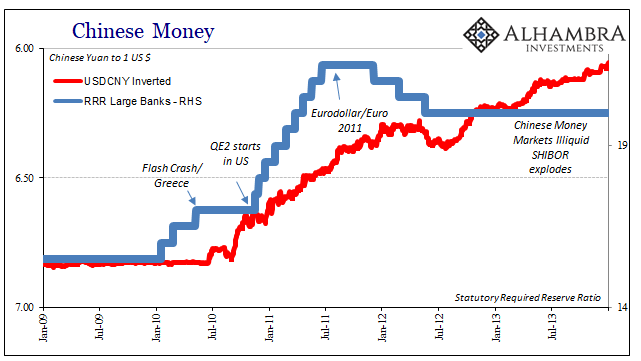

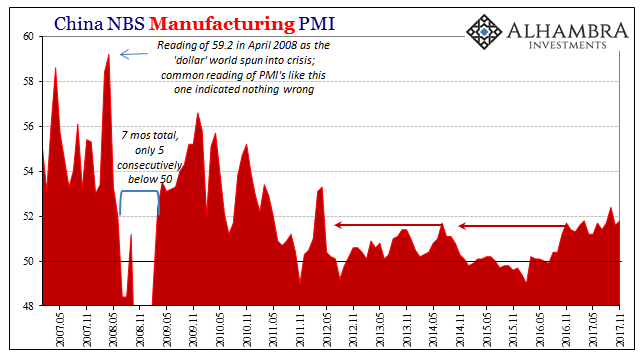

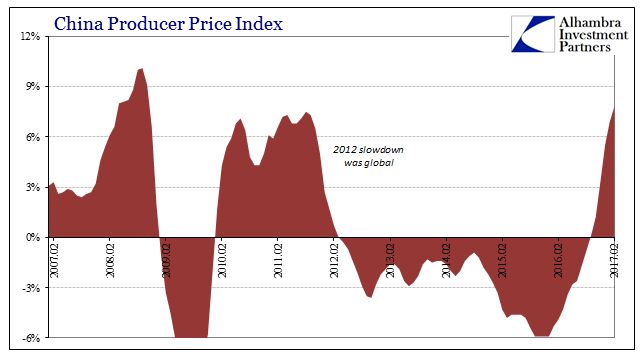

Raining On Chinese Prices

Raining On Chinese Prices20 Oct 2018

China’s Seven Years Disinflation11 Jul 2018

Three Years Ago QE, Last Year It Was China, Now It’s Taxes13 Dec 2017

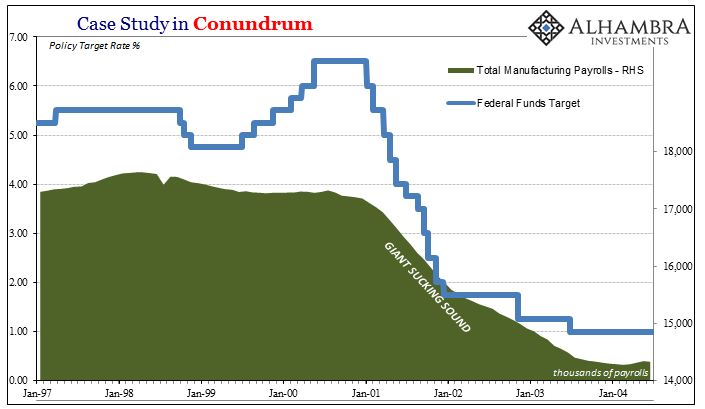

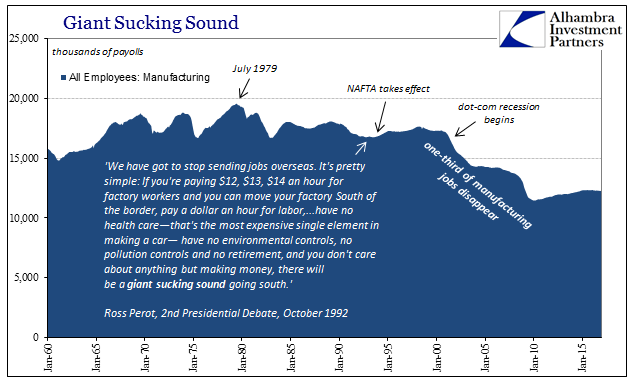

Giant Sucking Sound Sucks (Far) More Than US Industry Now11 Dec 2017

2017 Is Two-Thirds Done And Still No Payroll Pickup7 Sep 2017

Noose Or Ratchet11 May 2017

This Is Not Expansion6 May 2017

‘Dollar’ ‘Improvement’29 Apr 2017

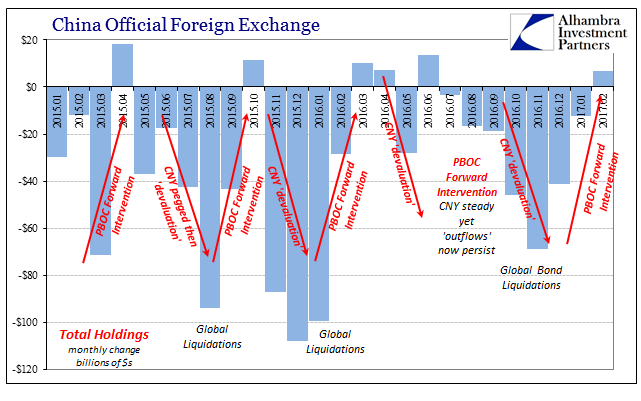

PBoC: Mechanical Tightening PBoC is China Central Bank28 Apr 2017

Assessing China’s Economic Risks18 Apr 2017

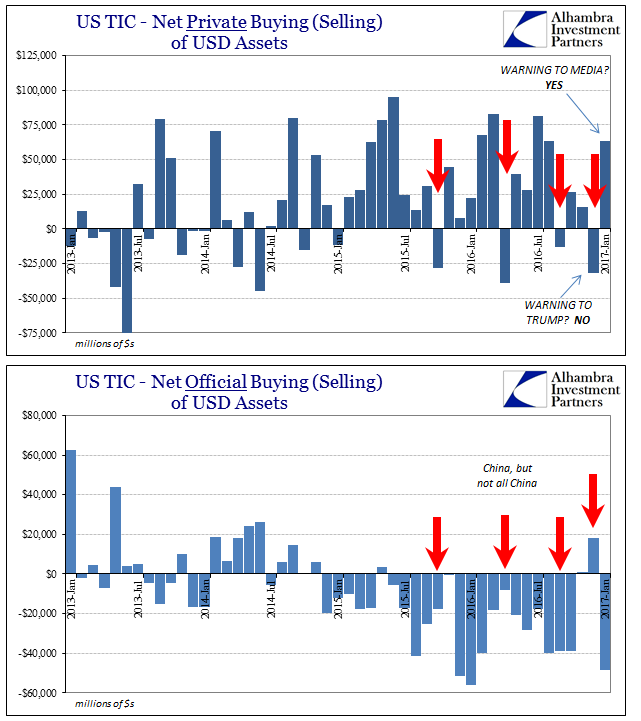

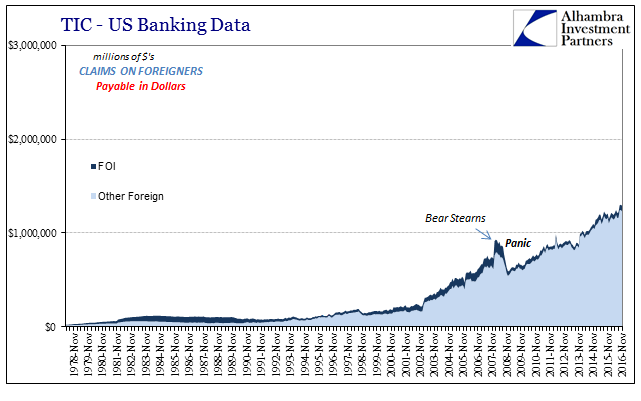

TIC Analysis of Selling25 Mar 2017

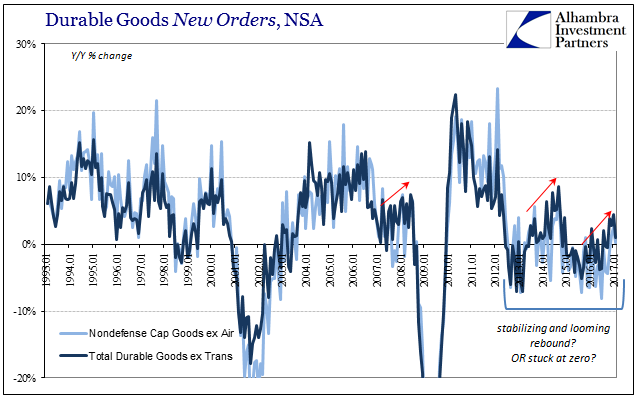

Durable Goods After Leap Year25 Mar 2017

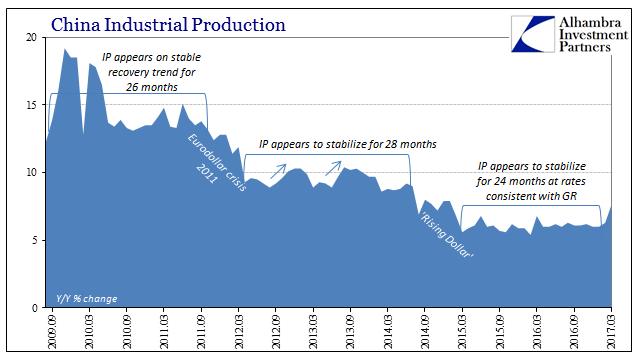

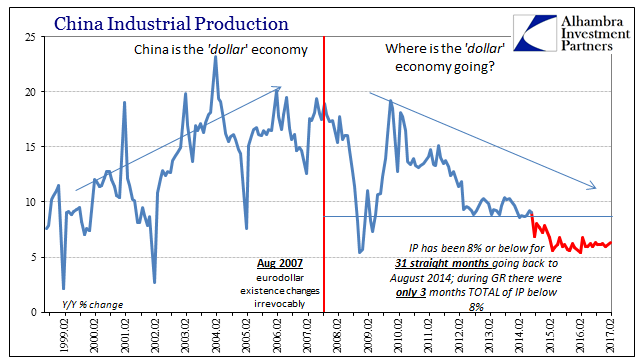

China Starts 2017 With Chronic, Not Stable And Surely Not ‘Reflation’15 Mar 2017

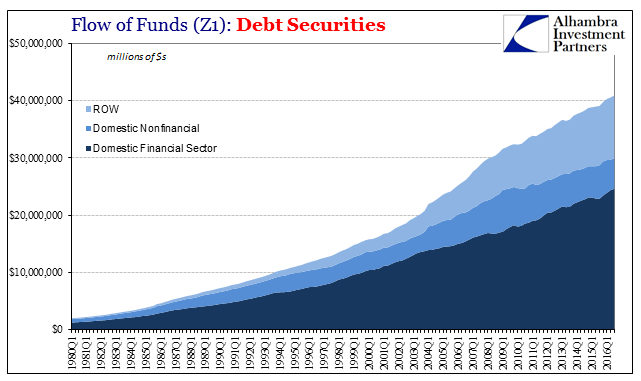

Do Record Debt And Loan Balances Matter? Not Even Slightly12 Mar 2017

Same Country, Different Worlds10 Mar 2017

China And Reserves, A Straightforward Process Unnecessarily Made Into A Riddle8 Mar 2017

Do Record Eurodollar Balances Matter? Not Even Slightly7 Mar 2017

It Was ‘Dollars’ All Along28 Feb 2017

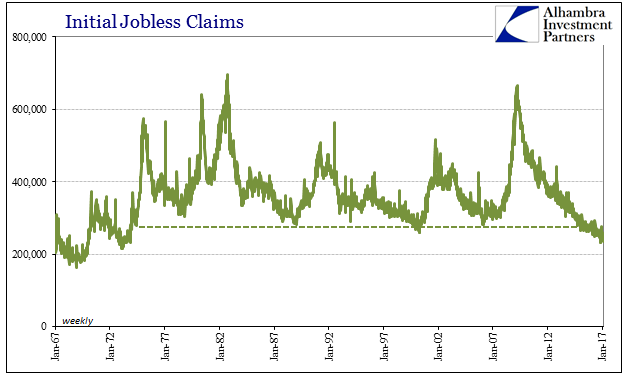

Jobless Claims Look Great, Until We Examine The Further Potential For What We Really, Really Don’t Want10 Feb 2017