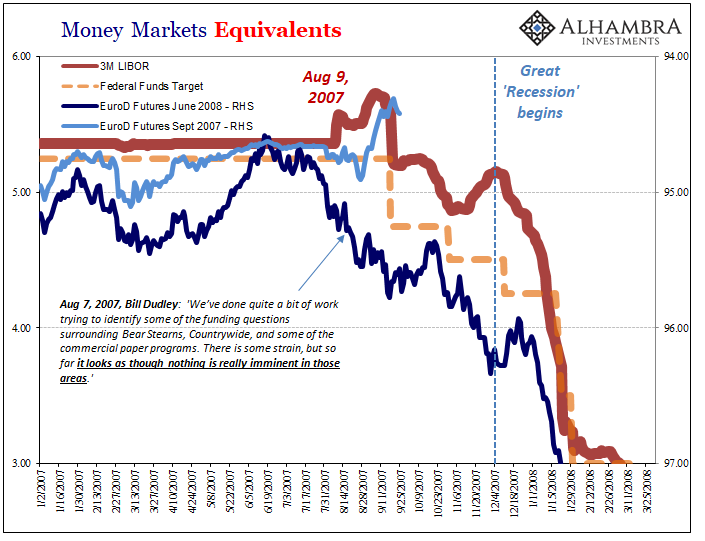

Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Eurodollar Futures Interpretation Is Everywhere

Eurodollar Futures Interpretation Is Everywhere1 Jul 2022

Sorry Chairman Powell, Even FRBNY Now Has To Forecast Serious and Seriously Rising Recession Risk20 Jun 2022

UST 2s & Euro$ Futures *Whites* Both Ask, Landmine At Last?25 May 2022

Inversion Is The Real March Madness, Just Don’t Take It Literally22 Mar 2022

Media Attention All Over FOMC, Market Attention Totally Elsewhere19 Mar 2022

Consumer Prices And The Historical Pain(s)12 Mar 2022

The Red Warning24 Feb 2022

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)25 Dec 2021

This Is A Big One (no, it’s not clickbait)2 Dec 2021

What Does Taper Look Like From The Inside? Not At All What You’d Think5 Nov 2021

Wait A Minute, What’s This Inversion?28 Jun 2020

Fragile, Not Fortified9 Apr 2020

Banks Or (euro)Dollars? That Is The (only) Question3 Apr 2020

Is GFC2 Over?18 Mar 2020

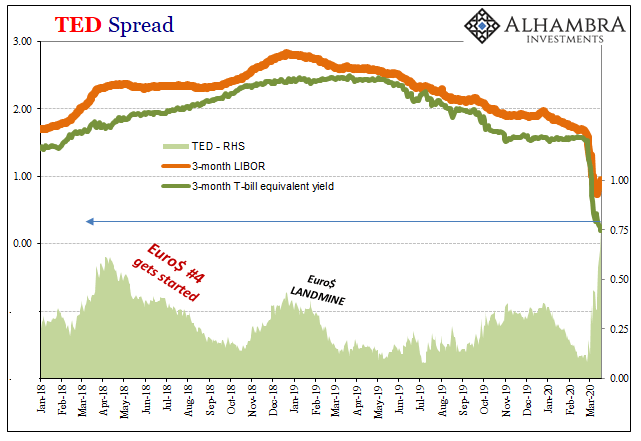

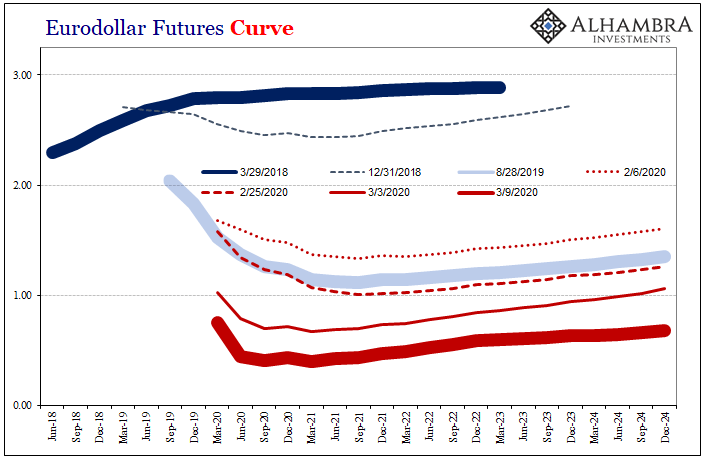

(Almost) Everything Sold Off Today12 Mar 2020

Economy: Curved Again27 Feb 2020

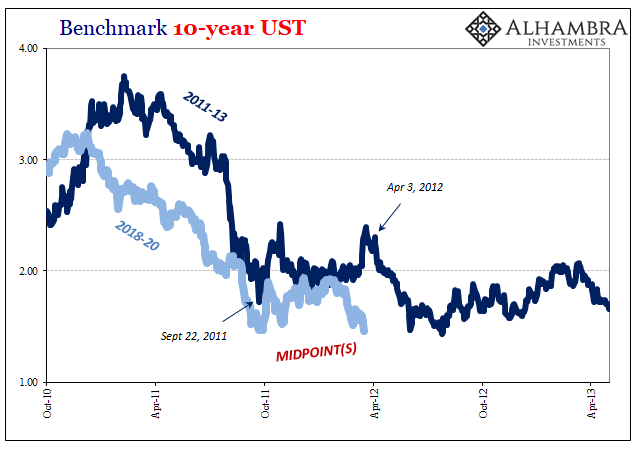

Was It A Midpoint And Did We Already Pass Through It?25 Feb 2020

ISM Spoils The Bond Rout!!! Again5 Oct 2019

What Kind Of Risks/Mess Are We Looking At?4 Jun 2019

The Transitory Story, I Repeat, The Transitory Story24 May 2019