Read More »

Tag Archive: Emerging Markets

EM Preview for the Week Ahead

Read More »

EM Preview for the Week Ahead

Read More »

EM Preview for the Week Ahead

Read More »

EM Preview for the Week Ahead

Read More »

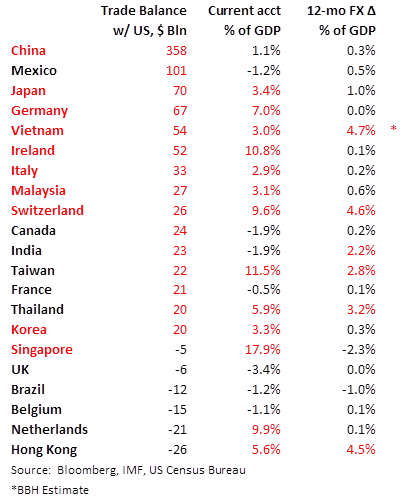

Some Thoughts on the Latest Treasury FX Report

Read More »

EM Preview for the Week Ahead

Read More »

EM Preview for the Week Ahead

Read More »

EM Preview for the Week Ahead

Read More »

EM Preview for the Week Ahead

Read More »

EM Preview for the Week Ahead

Read More »

EM Preview for the Week Ahead

Read More »

EM Preview for the Week Ahead

Read More »

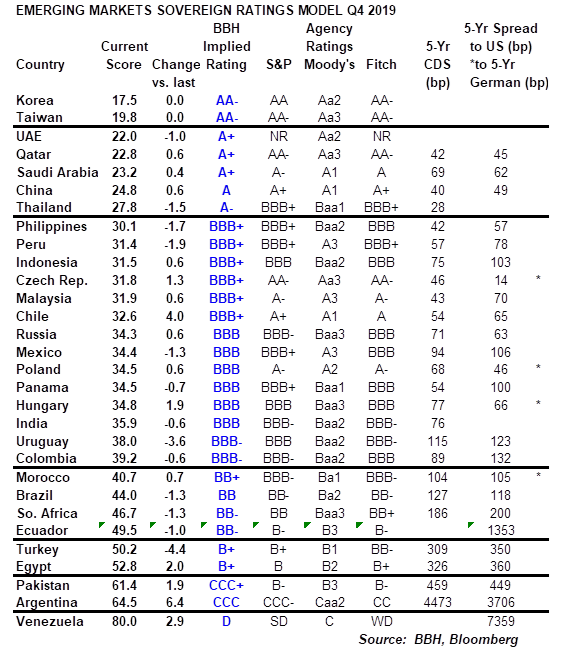

EM Sovereign Rating Model For Q4 2019

Read More »

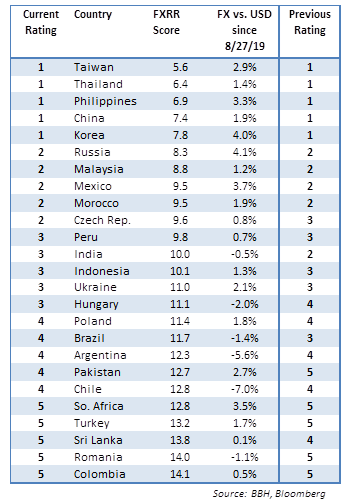

EM FX Model for Q4 2019

Read More »

EM Preview for the Week Ahead

Read More »

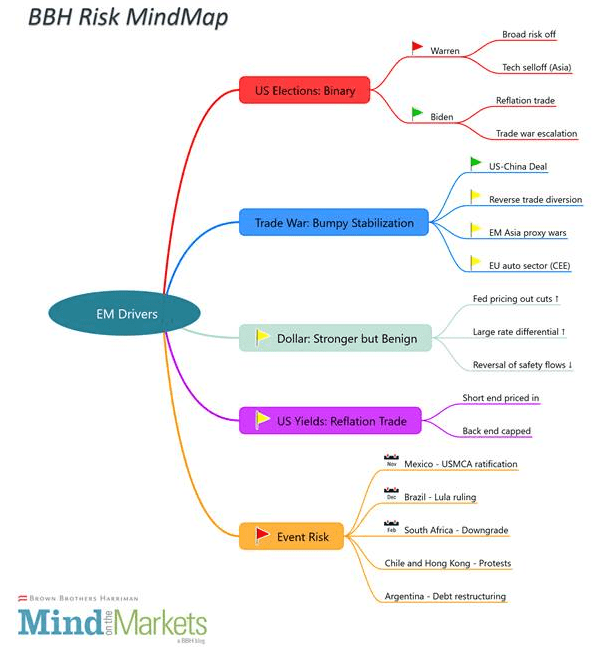

Emerging Market Risk Map

Read More »

EM Preview for the Week Ahead

Read More »

EM Preview for the Week Ahead

Read More »

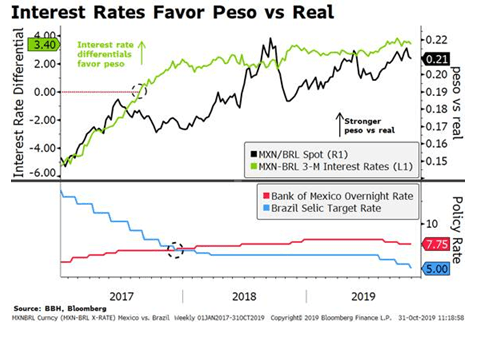

Mexico vs. Brazil Near-Term Outlook

Read More »

EM Preview for the Week Ahead

Read More »

On Swiss National Bank

On Swiss National Bank

-

SNB Sight Deposits: increased by 3.9 billion francs compared to the previous week

-

SNB’s Chairman Schlegel: A few months of negative inflation wouldn’t be a problem

-

2025-07-31 – Interim results of the Swiss National Bank as at 30 June 2025

-

SNB Brings Back Zero Percent Interest Rates

-

Hold-up sur l’eau potable (2/2) : la supercherie de « l’hydrogène vert ». Par Vincent Held

Main SNB Background Info

Featured and recent

-

MintID Silver Bars and Rounds Up Close with Money Metals

MintID Silver Bars and Rounds Up Close with Money Metals -

Swiss cheesemakers allowed to artificially make holes in Emmental cheese

Swiss cheesemakers allowed to artificially make holes in Emmental cheese -

Linksextreme schäumen vor WUT! AfD gelingt weitere Sensation in Sachsen-Anhalt!

Linksextreme schäumen vor WUT! AfD gelingt weitere Sensation in Sachsen-Anhalt! -

US imposes 15% tariff on Swiss pharma products

US imposes 15% tariff on Swiss pharma products -

Wann zahlt die BU nicht?

Wann zahlt die BU nicht? -

Was bedeutet das PFOF-Verbot?

Was bedeutet das PFOF-Verbot? -

Money Metals Gold Bar In Space

Money Metals Gold Bar In Space -

4-2-26 The Fed Is TRAPPED… And Oil Is The Problem

4-2-26 The Fed Is TRAPPED… And Oil Is The Problem -

4-2-26 Dynamic Learning Series – Tax Strategies: Beyond Filing: Avoid Penalties & Plan Smarter

4-2-26 Dynamic Learning Series – Tax Strategies: Beyond Filing: Avoid Penalties & Plan Smarter -

Will China be the real winner from the Iran war? | The Economist

Will China be the real winner from the Iran war? | The Economist

More from this category

Weekly Market Pulse: The Real Reason The Fed Should Pause

Weekly Market Pulse: The Real Reason The Fed Should Pause11 Oct 2022

Weekly Market Pulse: The Dog That Didn’t Bark

Weekly Market Pulse: The Dog That Didn’t Bark29 Aug 2022

Weekly Market Pulse: Things That Need To Happen

Weekly Market Pulse: Things That Need To Happen5 Jul 2022

Weekly Market Pulse: Oil Shock

Weekly Market Pulse: Oil Shock8 Mar 2022

Weekly Market Pulse: Are We There Yet?

Weekly Market Pulse: Are We There Yet?31 Jan 2022

Weekly Market Pulse: Fear Makes A Comeback

Weekly Market Pulse: Fear Makes A Comeback24 Jan 2022

Weekly Market Pulse: A Very Contrarian View

Weekly Market Pulse: A Very Contrarian View19 Jan 2022

Weekly Market Pulse: Zooming Out

Weekly Market Pulse: Zooming Out3 Oct 2021

Weekly Market Pulse: As Clear As Mud

Weekly Market Pulse: As Clear As Mud19 Jul 2021

Some Thoughts on the Latest Treasury FX Report

Some Thoughts on the Latest Treasury FX Report18 Dec 2020

EM Preview for the Week Ahead

EM Preview for the Week Ahead23 Nov 2020

Turkey Central Bank Preview

Turkey Central Bank Preview20 Nov 2020

Roadblocks and Opportunities for International Trade in 2021

Roadblocks and Opportunities for International Trade in 202118 Nov 2020

- EM Preview for the Week Ahead

26 Oct 2020

- EM Preview for the Week Ahead

19 Oct 2020

- EM Preview for the Week Ahead

28 Sep 2020

- EM Preview for the Week Ahead

8 Sep 2020

Where Has All the Carry Gone?

Where Has All the Carry Gone?21 Aug 2020

- EM Preview for the Week Ahead

10 Aug 2020

EM Preview for the Week Ahead

EM Preview for the Week Ahead3 Aug 2020