Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

The (less) Dollars Behind Xi’s Shanghai of Shanghai

The (less) Dollars Behind Xi’s Shanghai of Shanghai25 Apr 2022

China’s Loan Results Back The PBOC Going The Opposite Way From The Fed16 Mar 2022

Second Wave Global Trade10 Jul 2020

No Flight To Recognize Shortage

No Flight To Recognize Shortage22 May 2020

So Much Bond Bull21 May 2020

You Shouldn’t Miss The Cupom14 Feb 2020

China’s Dollar Problem Puts the Sync In Globally Synchronized Downturn18 Oct 2019

Where The Global Squeeze Is Unmasked17 Sep 2019

Dollar (In) Demand12 Sep 2019

Is The Negativity Overdone?10 Sep 2019

That Can’t Be Good: China Unveils Another ‘Market Reform’20 Aug 2019

China Has No Choice6 Mar 2019

China’s Big Money Gamble19 Feb 2019

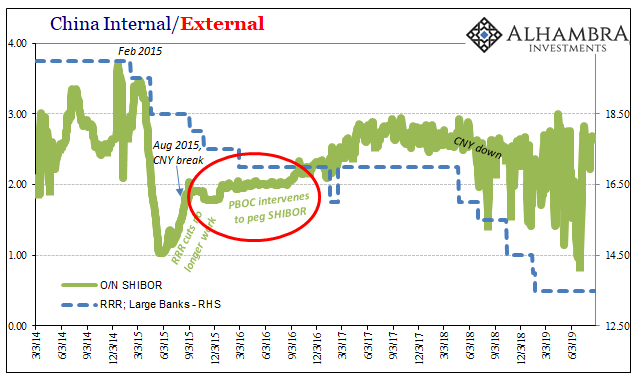

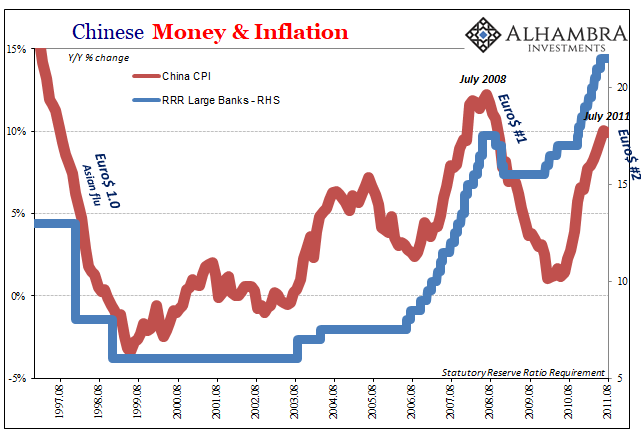

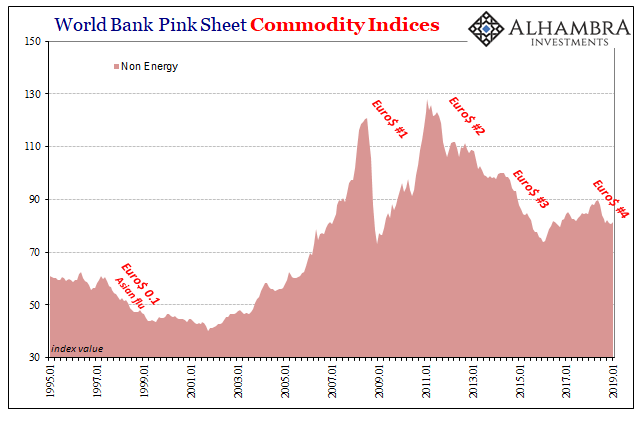

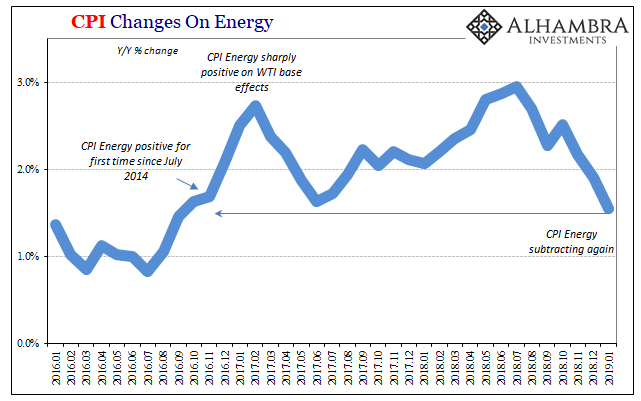

Inflation Falls Again, Dot-com-like16 Feb 2019

Rate of Change13 Jan 2019

More Unmixed Signals6 Jan 2019

Noose Or Ratchet11 May 2017

This Is Not Expansion6 May 2017

‘Dollar’ ‘Improvement’29 Apr 2017

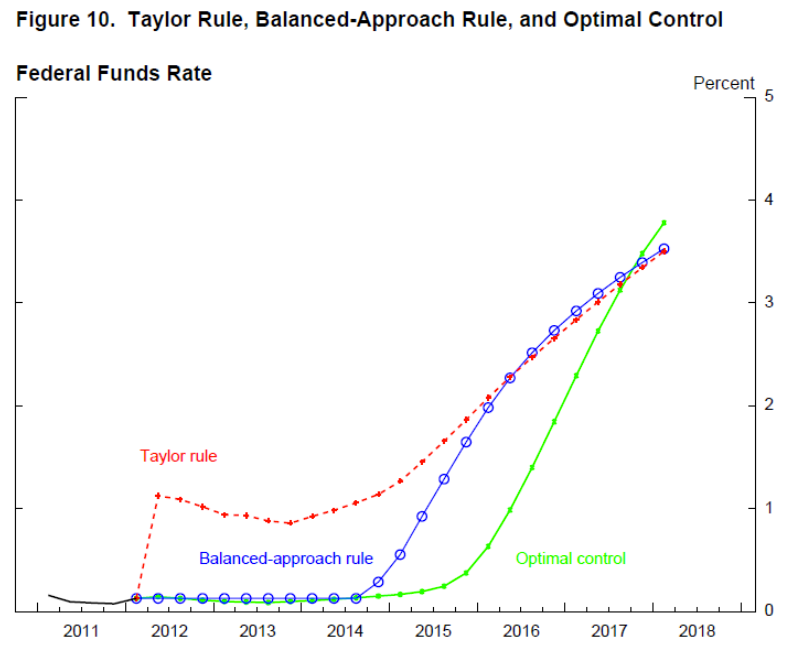

Optimal Lunacy15 Apr 2017