Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Double Whammy: US CPI and Federal Reserve

Double Whammy: US CPI and Federal Reserve12 Jun 2024

Consolidative Tuesday21 May 2024

Dollar Trades Above JPY150 and Truss Gets No Reprieve20 Oct 2022

Riksbank Hikes 100 bp but the Krona gets No Love

Riksbank Hikes 100 bp but the Krona gets No Love20 Sep 2022

Brent’s Back In A Big Way, Still ‘Something’ Missing12 Jun 2018

16 Jun 2017

Will the Dollar Appreciate on higher U.S. Savings and a Smaller Trade Deficit?12 Jul 2014

Last Week’s Sell-Off: More on the Discrepancy between Developed and Emerging Markets

Last Week’s Sell-Off: More on the Discrepancy between Developed and Emerging Markets27 Jan 2014

Strong Dollar: the Parallels Between Now, the 1980s and 1998-2002, Part 1: Austerity

Strong Dollar: the Parallels Between Now, the 1980s and 1998-2002, Part 1: Austerity9 Jul 2013

Danthine’s Latest Statements Imply that SNB Might Remove Cap in 2014

Danthine’s Latest Statements Imply that SNB Might Remove Cap in 201411 Jun 2013

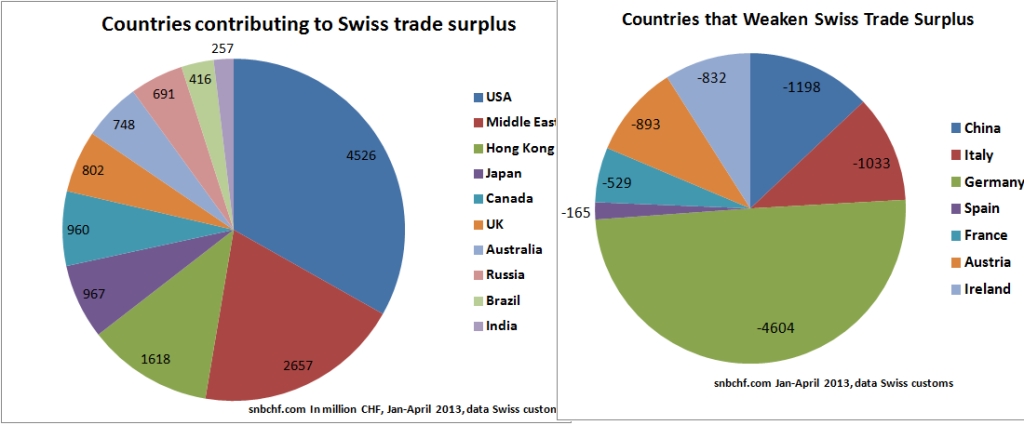

The Swiss Trade Surplus: A Really Global Economy

The Swiss Trade Surplus: A Really Global Economy28 May 2013

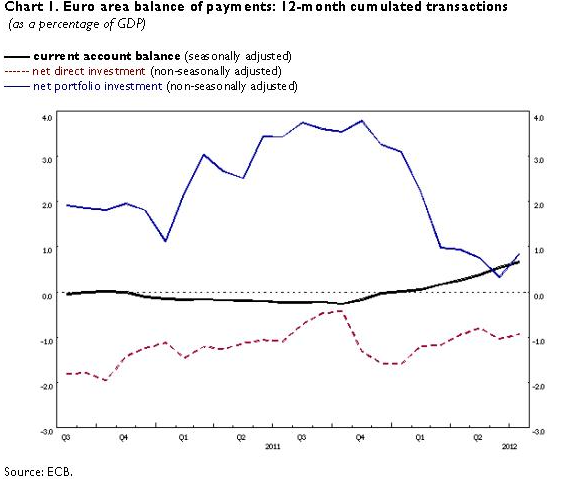

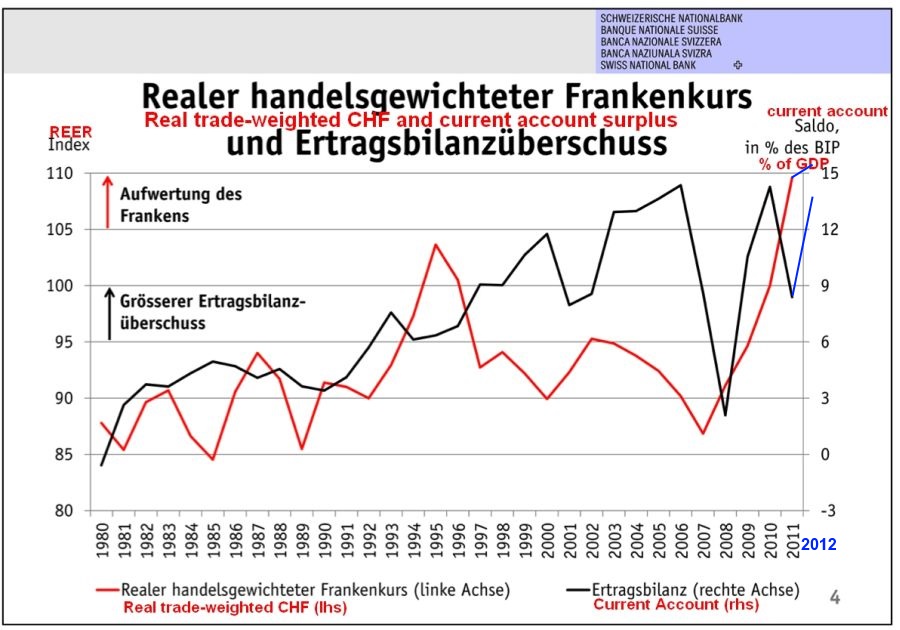

Swiss Current Account Surplus Rises from 8.5 percent to 13.5 percent of GDP

Swiss Current Account Surplus Rises from 8.5 percent to 13.5 percent of GDP28 Mar 2013

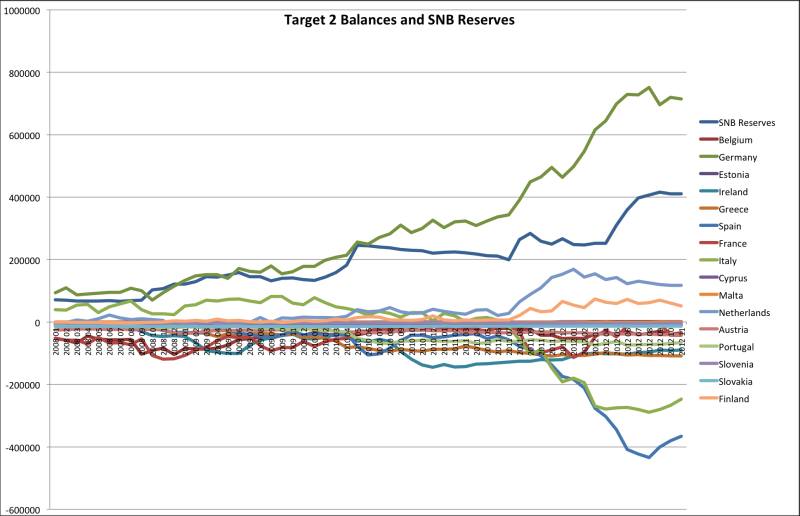

Target2 Balances and SNB Currency Reserves: Same Concept, Update February 2013

Target2 Balances and SNB Currency Reserves: Same Concept, Update February 20139 Feb 2013

Japanese Currency Debasement, Part 1: Current Account and Japanese Bond Bears

Japanese Currency Debasement, Part 1: Current Account and Japanese Bond Bears30 Jan 2013

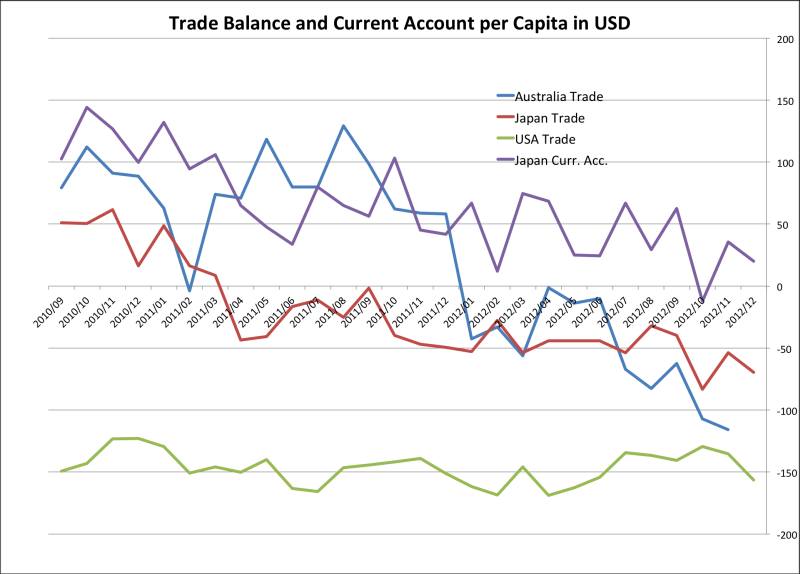

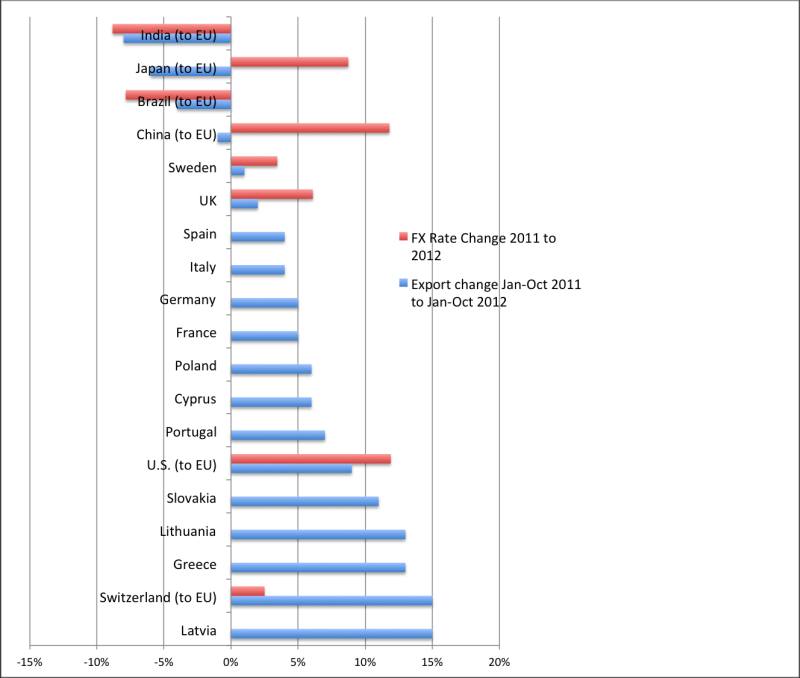

Comparing Trade Balances with FX Rates: Will the European Miracle End?

Comparing Trade Balances with FX Rates: Will the European Miracle End?27 Jan 2013

Roubini and Deutsche Bank’s Sanjeev Sanyal: Still Waiting for the Chinese Consumer

Roubini and Deutsche Bank’s Sanjeev Sanyal: Still Waiting for the Chinese Consumer24 Jan 2013

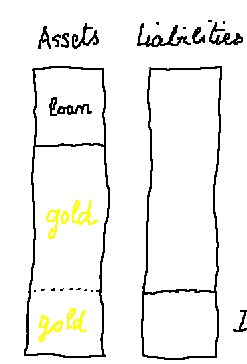

German Currency and Gold Reserves and the German Trade Surplus

German Currency and Gold Reserves and the German Trade Surplus17 Jan 2013

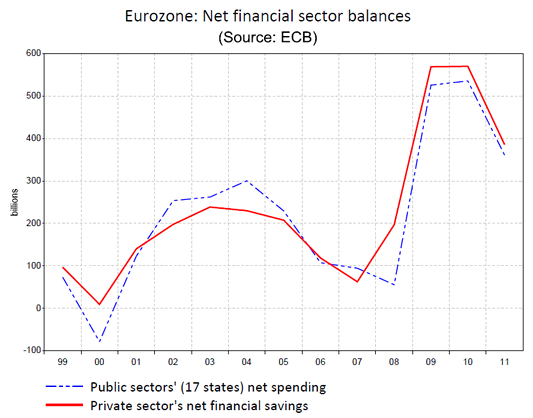

Same Procedure as Every Year: Analysts Shouting “The Great Recession is Over!” But It Is Not!

Same Procedure as Every Year: Analysts Shouting “The Great Recession is Over!” But It Is Not!6 Jan 2013

FX Theory: The Balance of Payments Model Explained in 400 Words

FX Theory: The Balance of Payments Model Explained in 400 Words30 Dec 2012

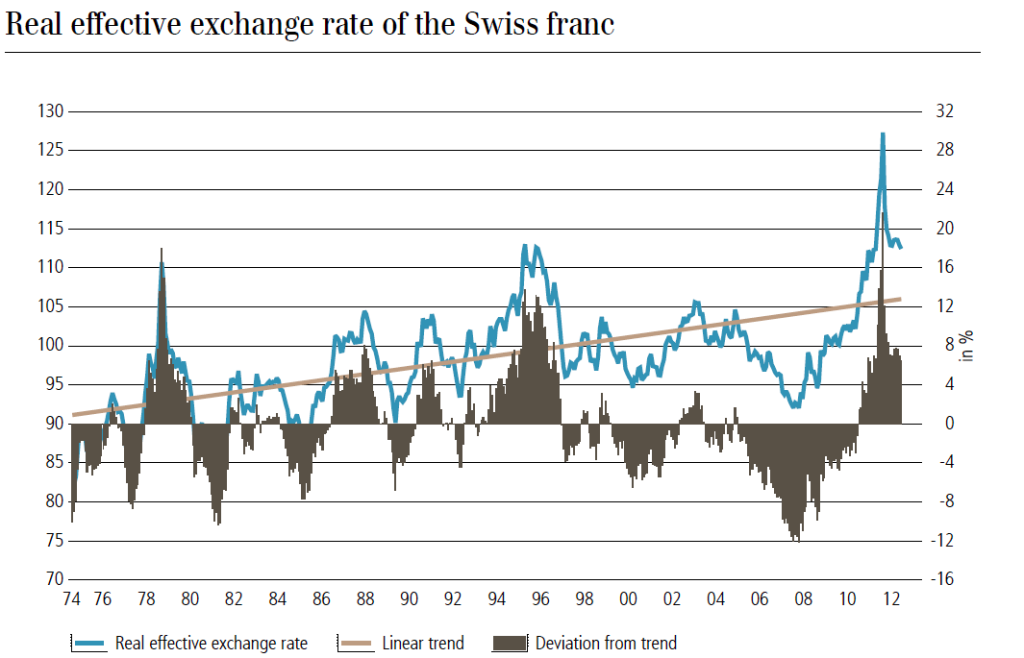

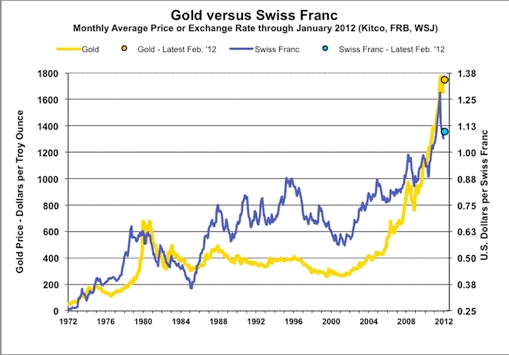

Correlations Between the Swiss Franc, Gold and the German Economy

Correlations Between the Swiss Franc, Gold and the German Economy21 Dec 2012