Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Key Chart Points Hold and the Dollar’s Rally Stalls Ahead of the Weekend

Key Chart Points Hold and the Dollar’s Rally Stalls Ahead of the Weekend19 May 2023

FX Daily, August 24: Markets Prove Resilient to Start New Week24 Aug 2020

Speculative Positioning in Selected Currency Futures10 Aug 2020

COT Black: No Love For Super-Secret Models

COT Black: No Love For Super-Secret Models1 May 2020

Great Graphic: Euro Bulls Stir but Hardly Shaken2 Jun 2018

Great Graphic: Has Position Adjustment Begun in Treasury Futures?28 Feb 2018

Great Graphic: Bears Very Short US 10-Year Ahead of CPI16 Feb 2018

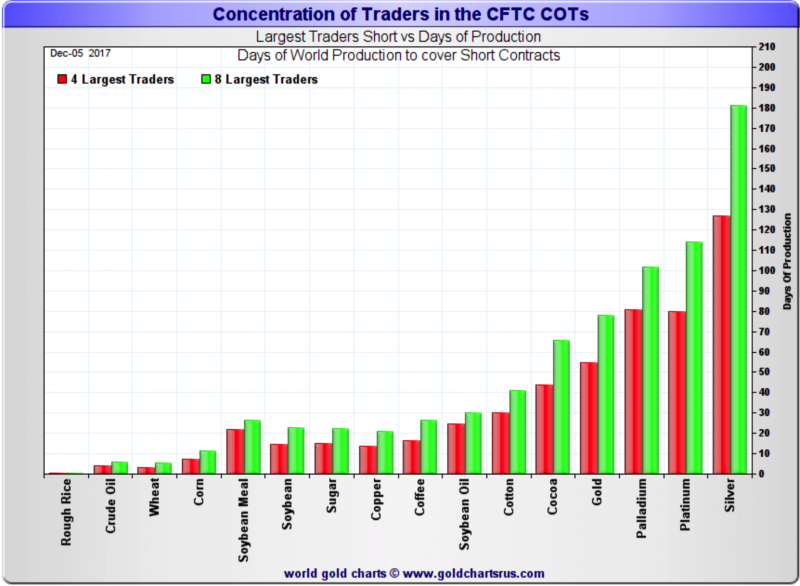

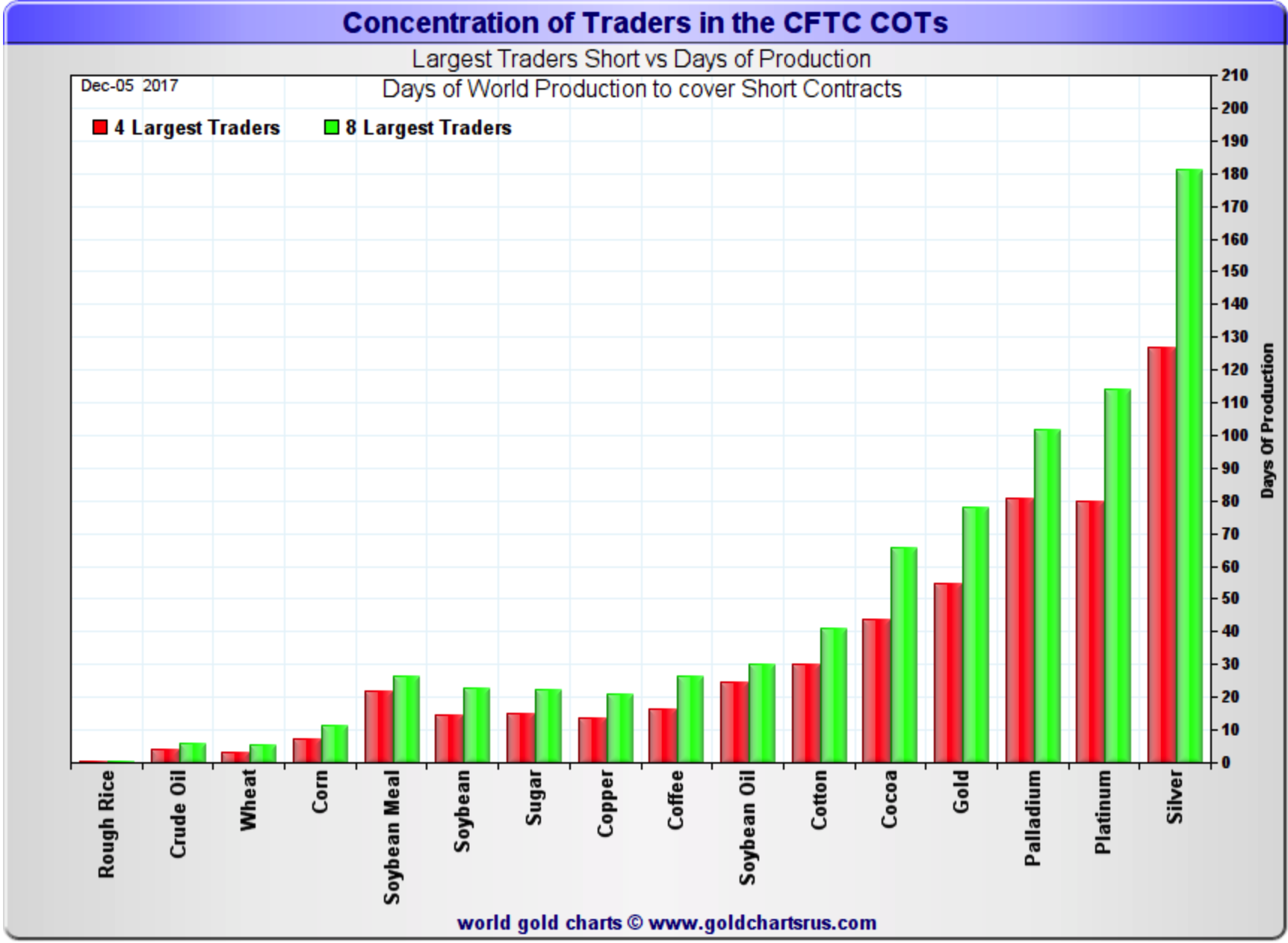

Buy Gold, Silver Time After Speculators Reduce Longs and Banks Reduce Shorts

Buy Gold, Silver Time After Speculators Reduce Longs and Banks Reduce Shorts17 Dec 2017

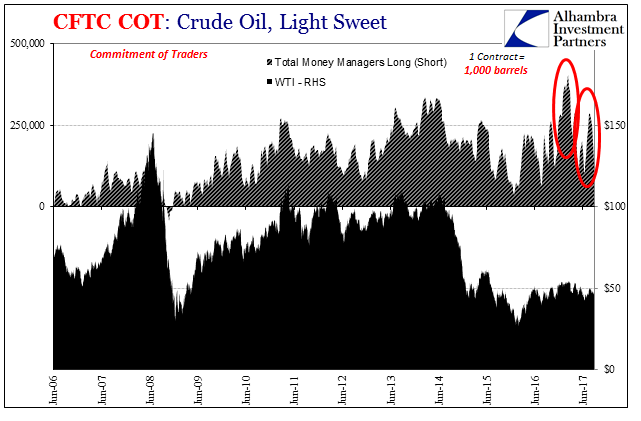

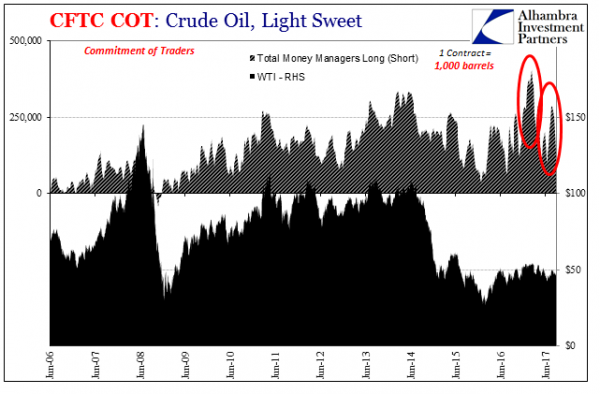

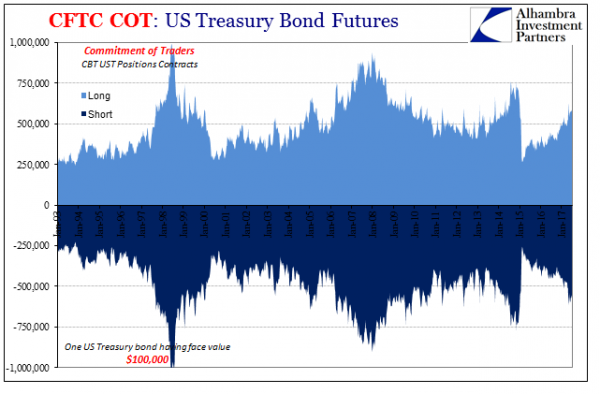

COT Report: Black (Crude) and Blue (UST’s)

COT Report: Black (Crude) and Blue (UST’s)15 Sep 2017

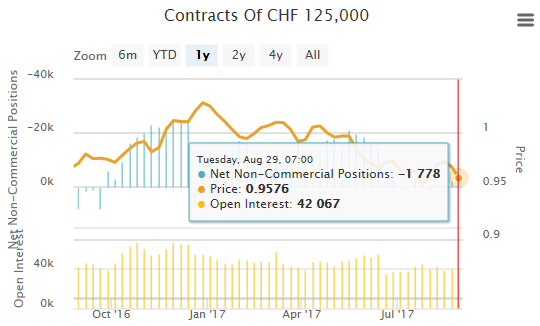

Weekly Speculative Positions (as of August 29): Speculators Make Minor Position Adjustments, but Like that Aussie4 Sep 2017

Weekly Speculative Positions (as of August 22): Sterling Bears Press, but Too Much?28 Aug 2017

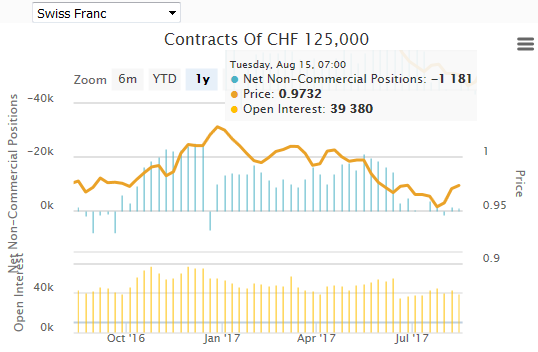

Weekly Speculative Positions (as of August 15): Speculators Add to Sterling and Peso Shorts, While Cutting Euro and Canadian Dollar Longs21 Aug 2017

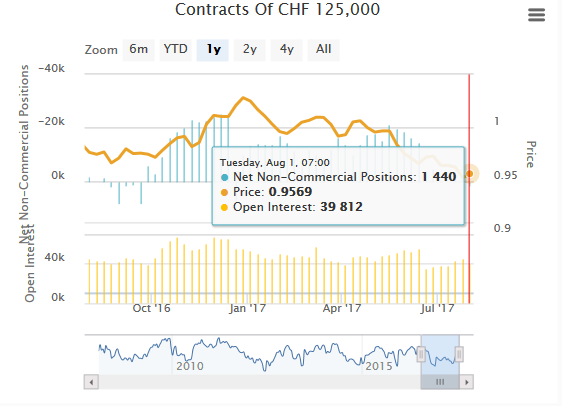

Weekly Speculative Positions (as of August 01): Speculators Press Ahead with Dollar-Bloc Currencies, but Hesitate with Euro and Yen7 Aug 2017

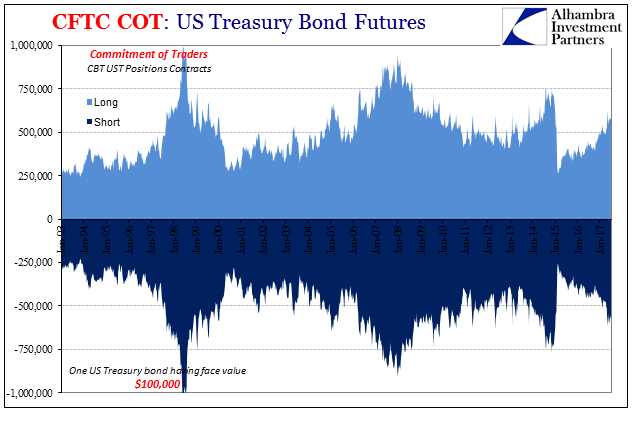

U.S. Treasuries: Not Really Wrong On Bonds

U.S. Treasuries: Not Really Wrong On Bonds6 Aug 2017

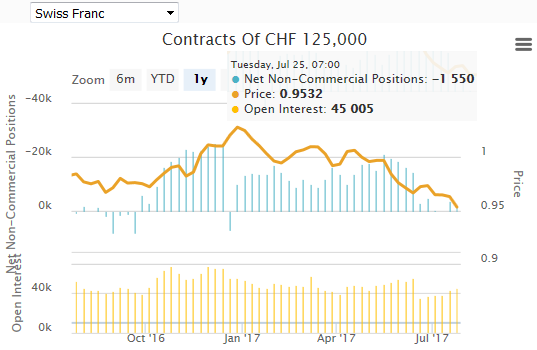

Weekly Speculative Positions (as of July 25): Speculators Continue to Pour into Australian and Canadian Dollar Futures31 Jul 2017

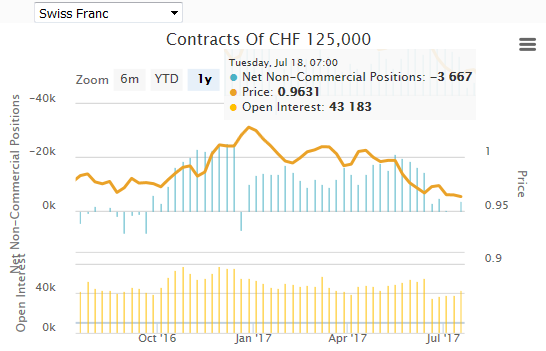

Weekly Speculative Positions (as of July 18): Speculators short CHF against USD again24 Jul 2017

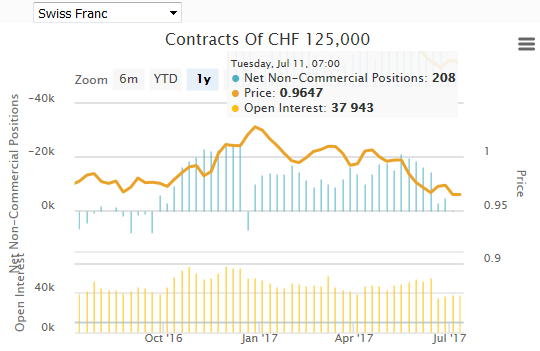

Weekly Speculative Positions (as of July 11): Speculators Switch to CHF Long against USD17 Jul 2017

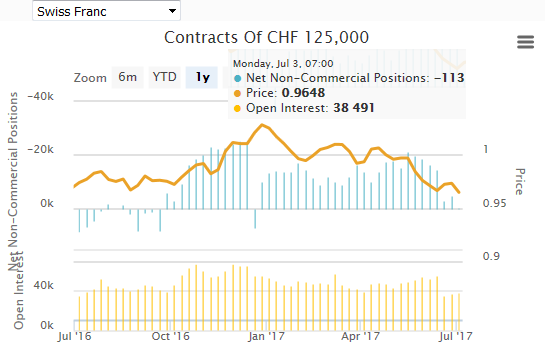

Weekly Speculative Positions (as of July 04): Speculators Still Dollar Negative10 Jul 2017

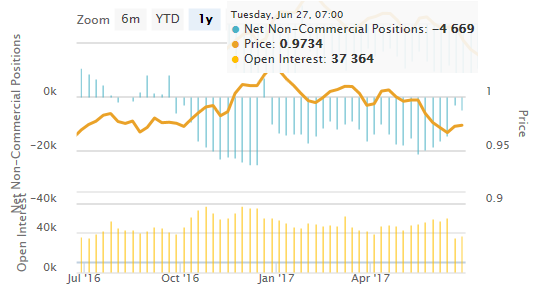

Weekly Speculative Positions (as of June 27): Speculators Scramble to Cover Short Canadian Dollar and Mexican Peso Futures3 Jul 2017

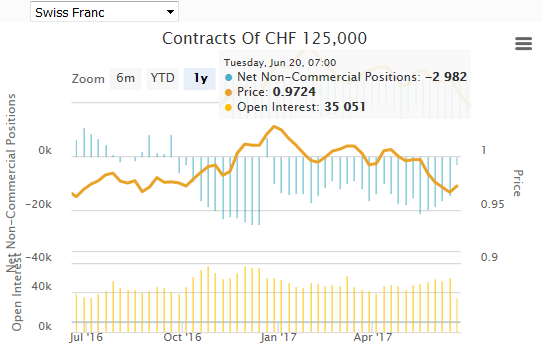

Weekly Speculative Positions (as of June 20): Surge in Positioning amid Currency Contract Roll26 Jun 2017