Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

The FOMC Channels China’s Xi As To Japan Going Global

The FOMC Channels China’s Xi As To Japan Going Global13 Dec 2019

The Big One, The Smoking Gun29 Nov 2019

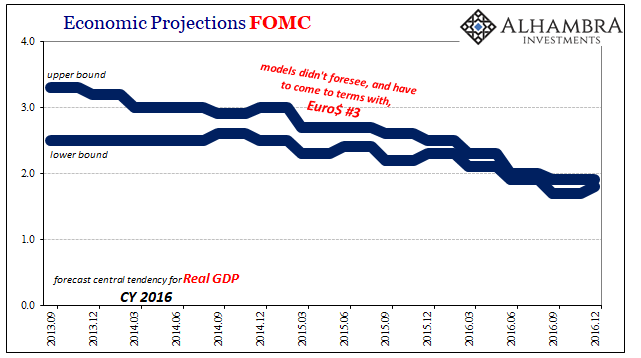

Expectations and Acceptance of Potential

Expectations and Acceptance of Potential23 Sep 2017

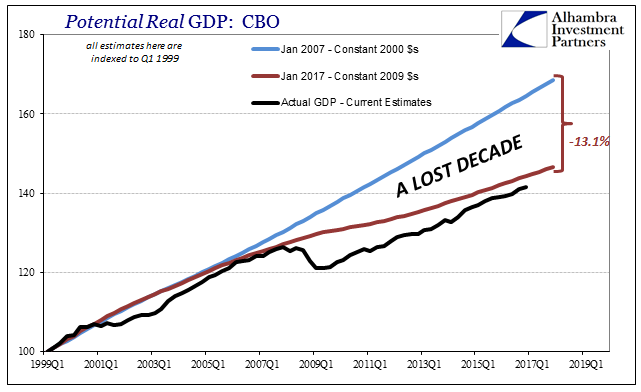

Real GDP: The Staggering Costs12 Aug 2017

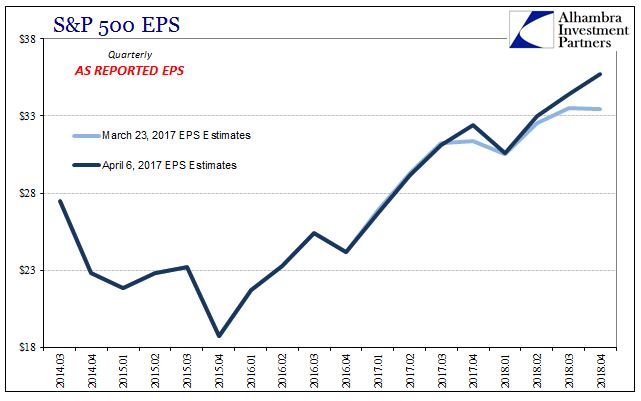

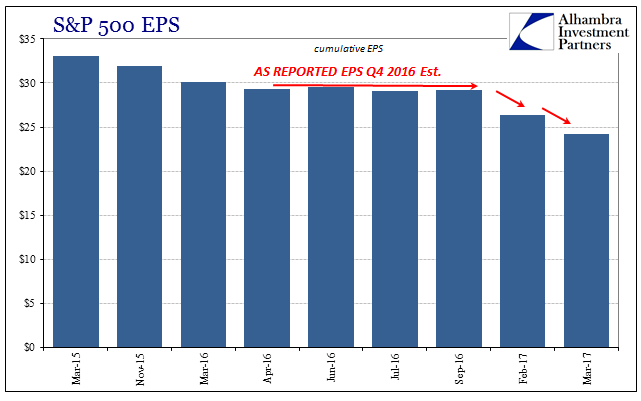

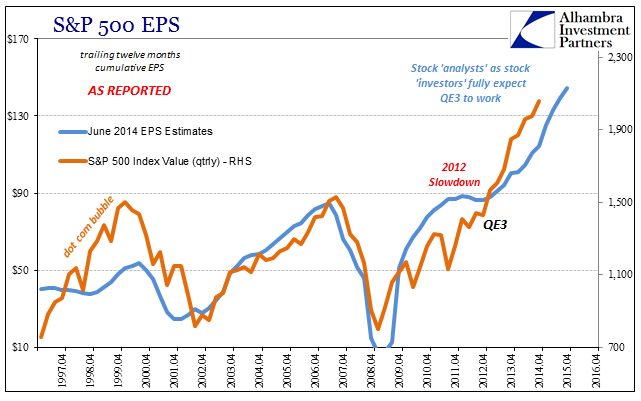

Earnings per Share: Is It Other Than Madness?16 Apr 2017

The Inverse of Keynes26 Mar 2017

Mugged By Reality; Many Still Yet To Be14 Mar 2017

The Market Is Not The Economy, But Earnings Are (Closer)23 Feb 2017

The Stinking Politics of It All22 Feb 2017

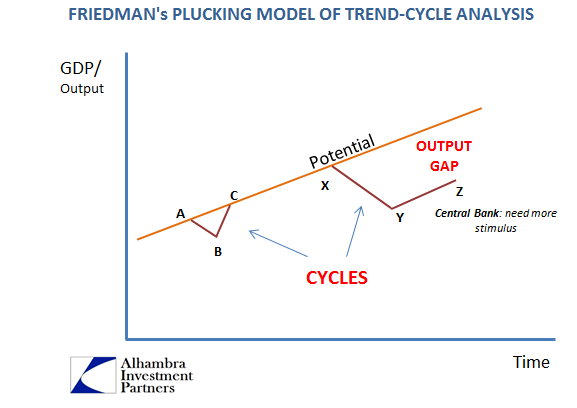

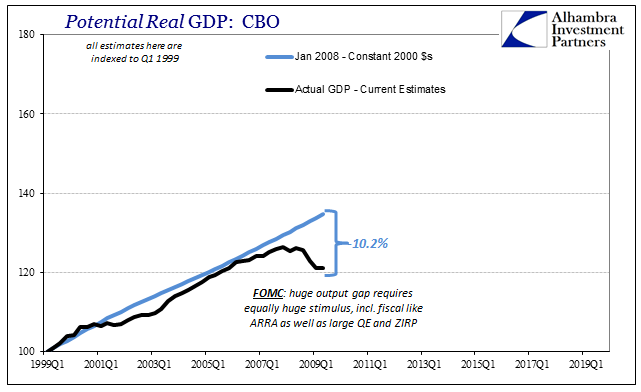

Their Gap Is Closed, Ours Still Needs To Be19 Feb 2017