Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

FOMC Goes With Unemployment Rate While This Huge Number Happens To Far More Relevant Economic Data

FOMC Goes With Unemployment Rate While This Huge Number Happens To Far More Relevant Economic Data29 Jan 2022

White-Hot Cycles of Silence28 Dec 2021

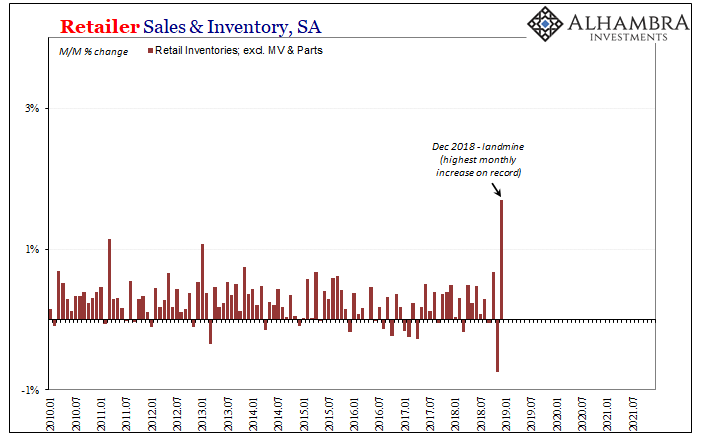

An Economy Dividing By Inventory And Labor30 Sep 2021

Revisiting The Last Overhang29 Sep 2021

FX Daily, July 20: Doom and Gloom Takes Toll20 Jul 2021

Consumers, Too; (Un)Confident To Re-engage19 Dec 2020

US Sales and Production Remain Virus-Free, But Still Aren’t Headwind-Free

US Sales and Production Remain Virus-Free, But Still Aren’t Headwind-Free18 Feb 2020

You Will Never Bring It Back Up If You Have No Idea Why It Falls Down And Stays Down10 Dec 2019

Focus Is On The Pre-recession Condition18 Sep 2019

Green Shoot or Domestic Stall?17 Apr 2019

The Death of a Business Cycle

The Death of a Business Cycle17 Jan 2019

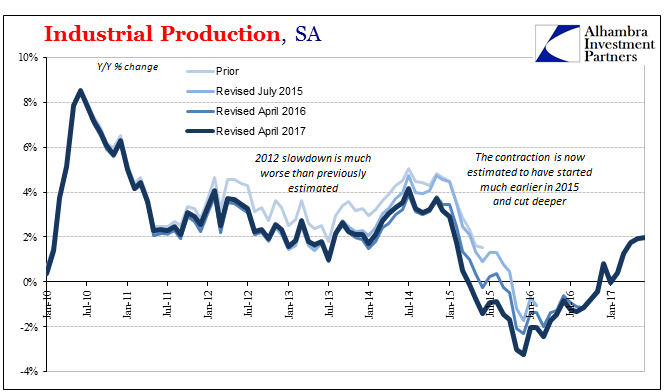

Why The Last One Still Matters (IP Revisions)26 Apr 2018

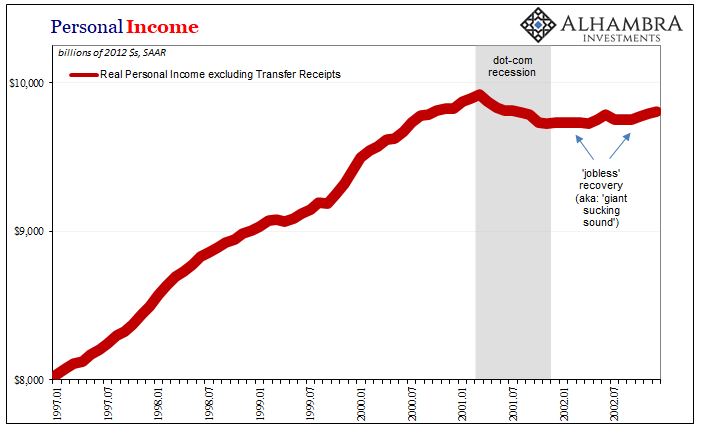

Giant Sucking Sound Sucks (Far) More Than US Industry Now11 Dec 2017

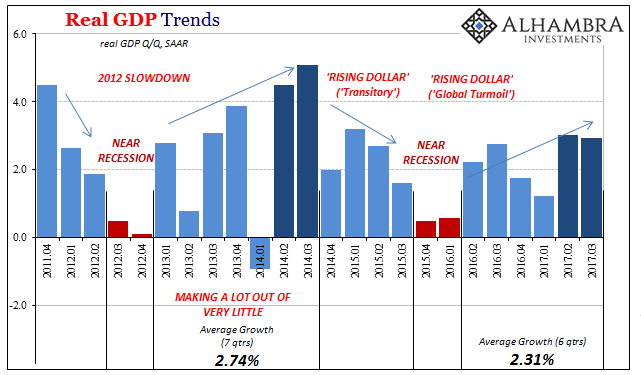

Strong Growth? Q3 GDP Only Shows How Weak 2017 Has Been3 Nov 2017

More Noise Than Signal

More Noise Than Signal27 Aug 2017

United States: Still No Up19 Aug 2017

U.S. Industrial Production: Industrial Drag21 Jul 2017

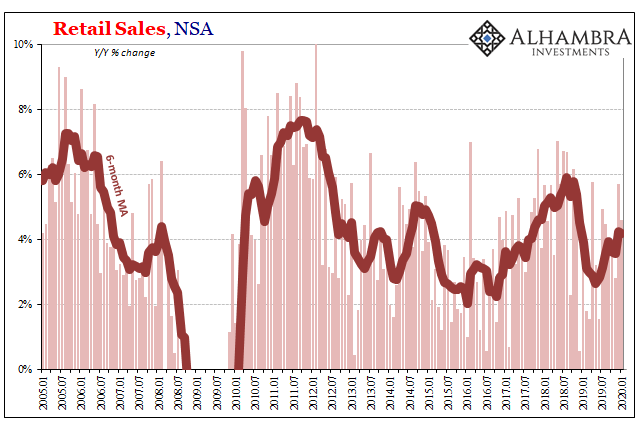

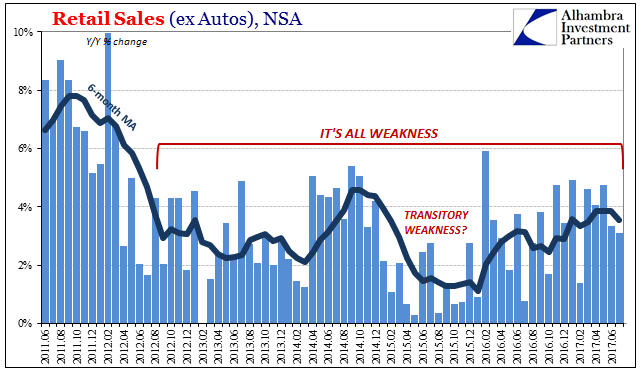

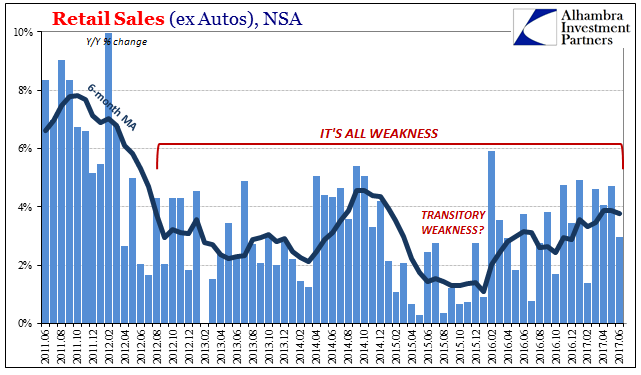

Retail Sales Conundrum20 Jul 2017

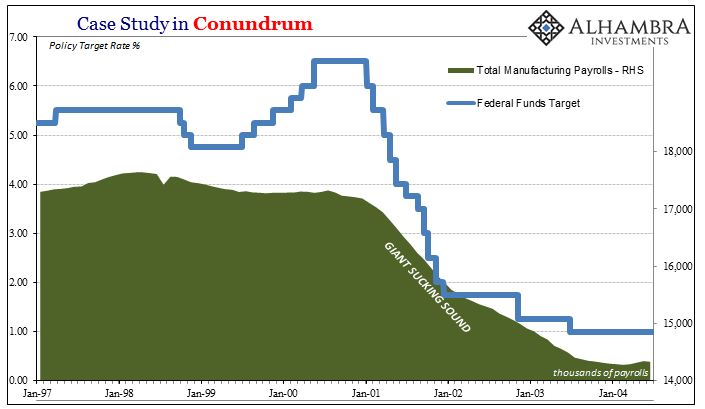

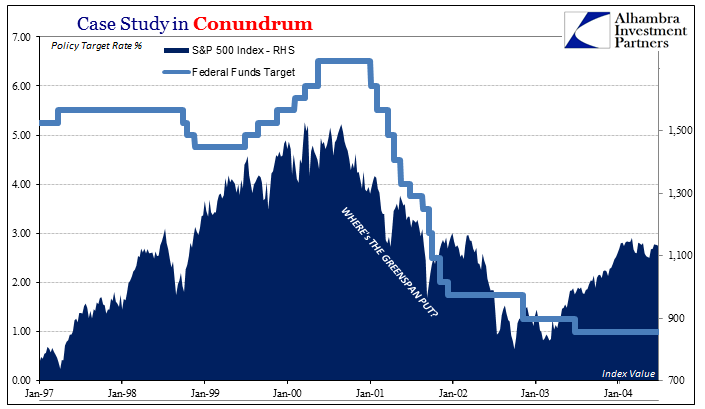

US S&P 500 Index, Federal Funds Target, Manufacturing Payrolls, US Imports and US Banking Data: All Conundrums Matter19 Jul 2017

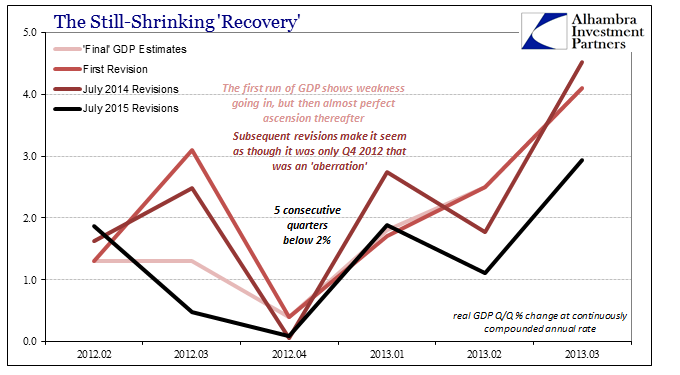

Hopefully Not Another Three Years19 May 2017