Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

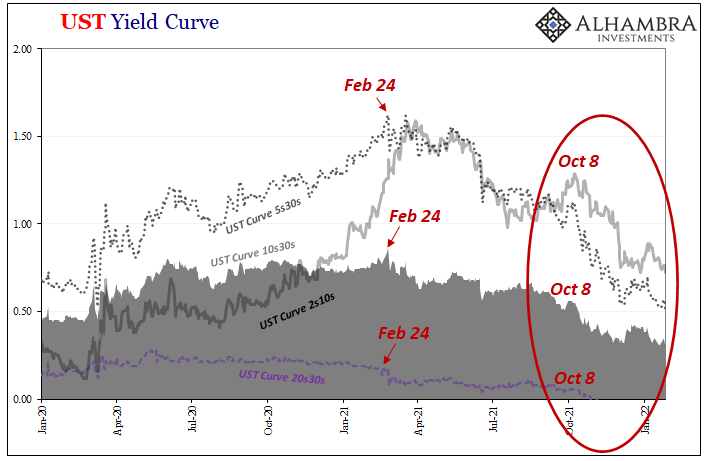

After Today’s FOMC, Yield Curve Is Already As Flat As It Was In Mar ’18 **Without A Single Rate Hike Yet**

After Today’s FOMC, Yield Curve Is Already As Flat As It Was In Mar ’18 **Without A Single Rate Hike Yet**28 Jan 2022

The Hawks Circle Here, The Doves Win There26 Jan 2022

Weekly Market Pulse: Discounting The Future7 Dec 2021

What Does Taper Look Like From The Inside? Not At All What You’d Think5 Nov 2021

Weekly Market Pulse: Inflation Scare!

Weekly Market Pulse: Inflation Scare!25 Oct 2021

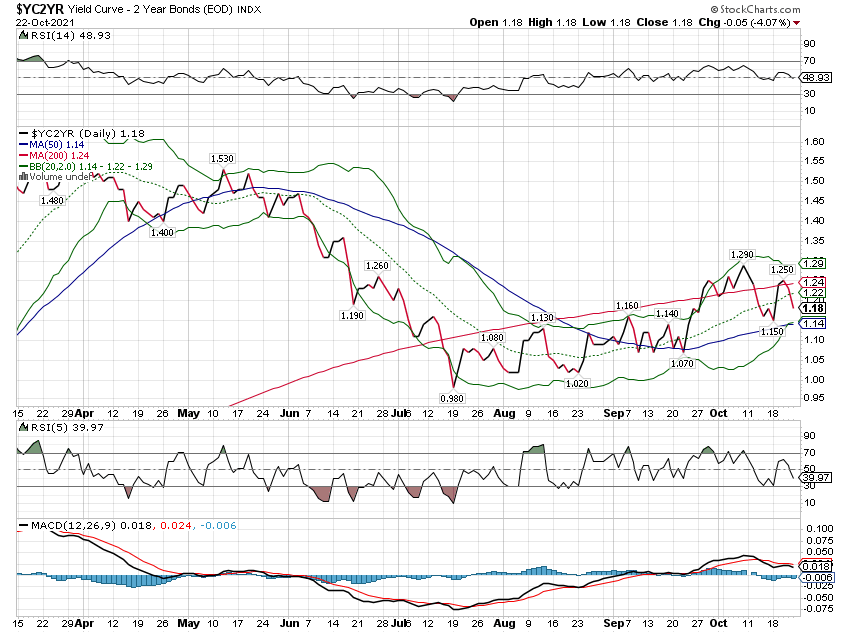

Lower Yields And (fewer) Bills21 Jul 2021

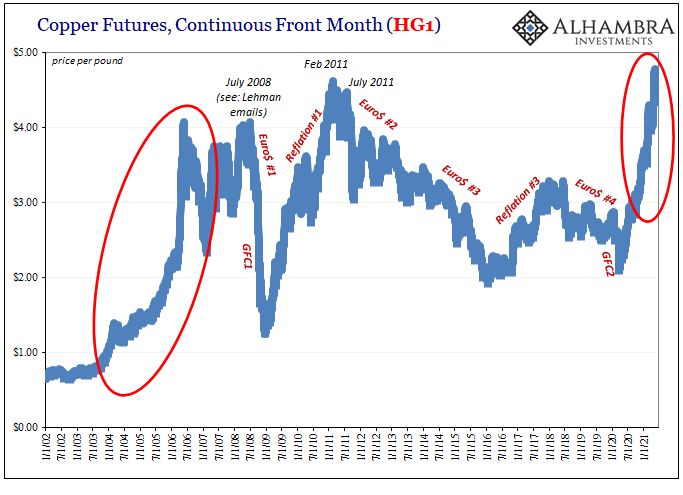

Copper Corroding PPI17 Jun 2021

Weekly Market Pulse: Buy The Rumor, Sell The News

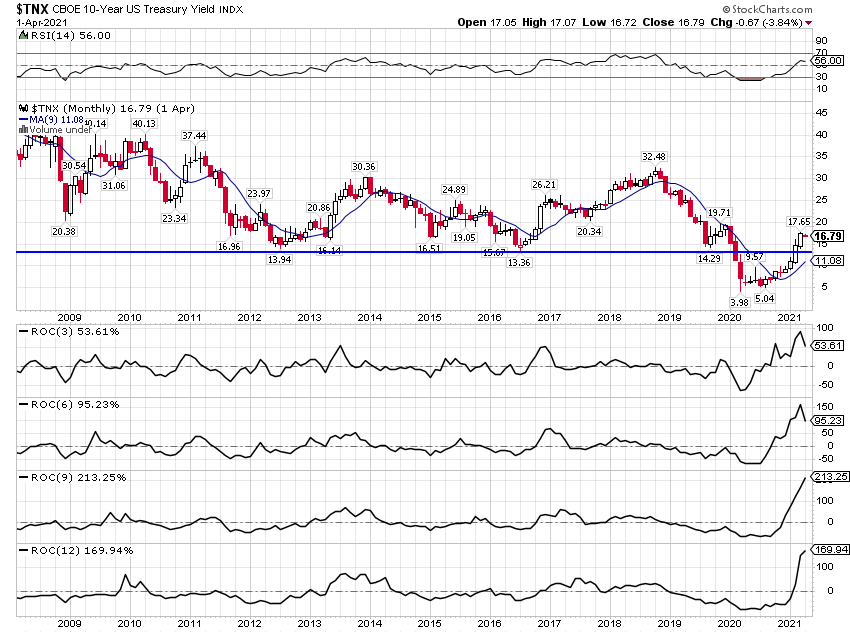

Weekly Market Pulse: Buy The Rumor, Sell The News5 Apr 2021

They’ve Gone Too Far (or have they?)10 Jan 2021

Meanwhile, Outside Today’s DC5 Nov 2020

Powell Would Ask For His Money Back, If The Fed Did Money5 Sep 2020

So Much Bond Bull21 May 2020

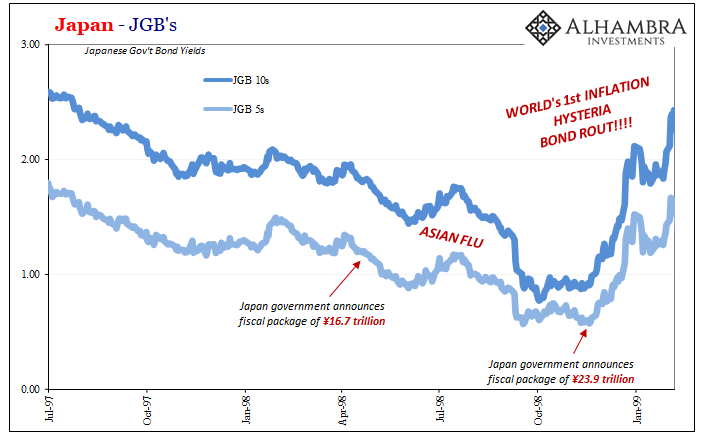

There Was Never A Need To Translate ‘Weimar’ Into Japanese

There Was Never A Need To Translate ‘Weimar’ Into Japanese17 May 2020

Everyone Knows The Gov’t Wants A ‘Controlled’ Weimar9 May 2020

(Almost) Everything Sold Off Today12 Mar 2020

The Greenspan Moon Cult5 Mar 2020

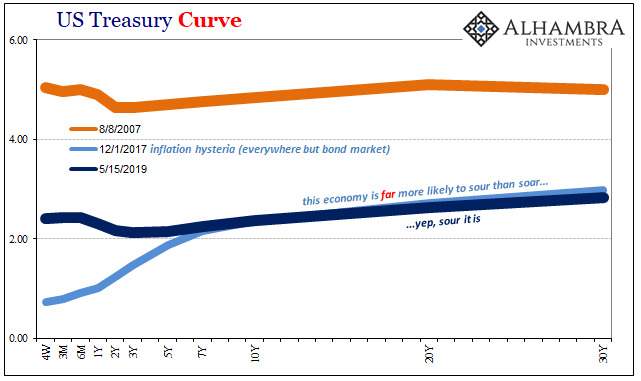

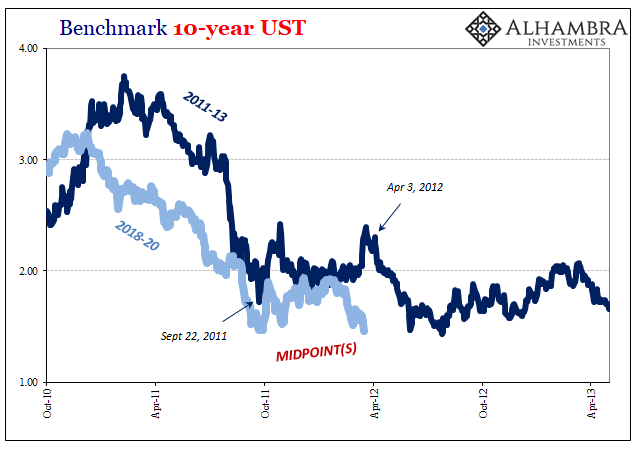

Was It A Midpoint And Did We Already Pass Through It?25 Feb 2020

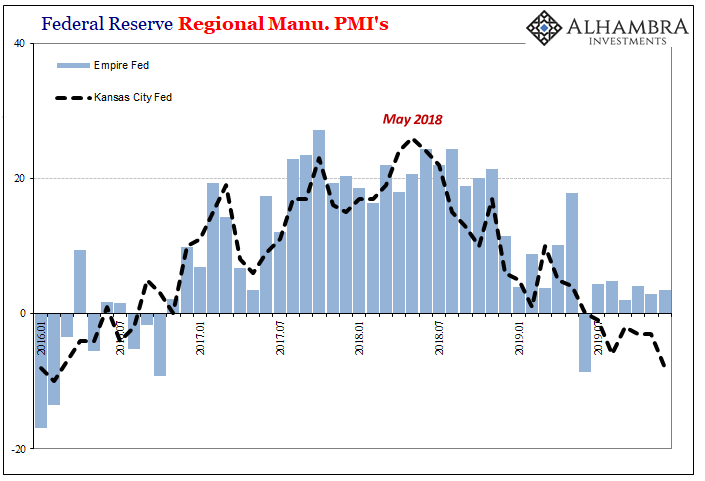

Manufacturing Clears Up Bond Yields7 Jan 2020

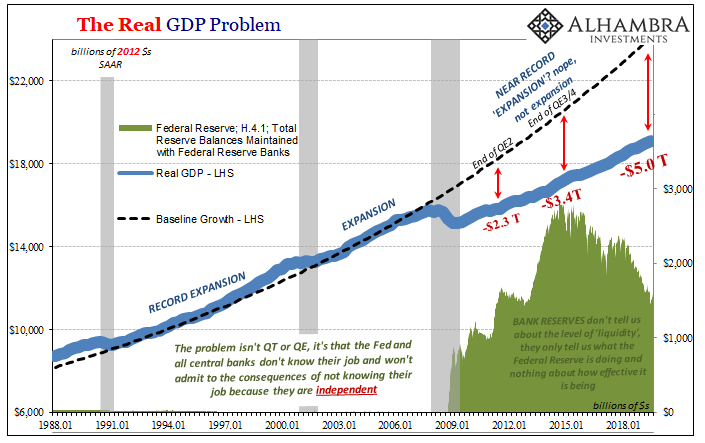

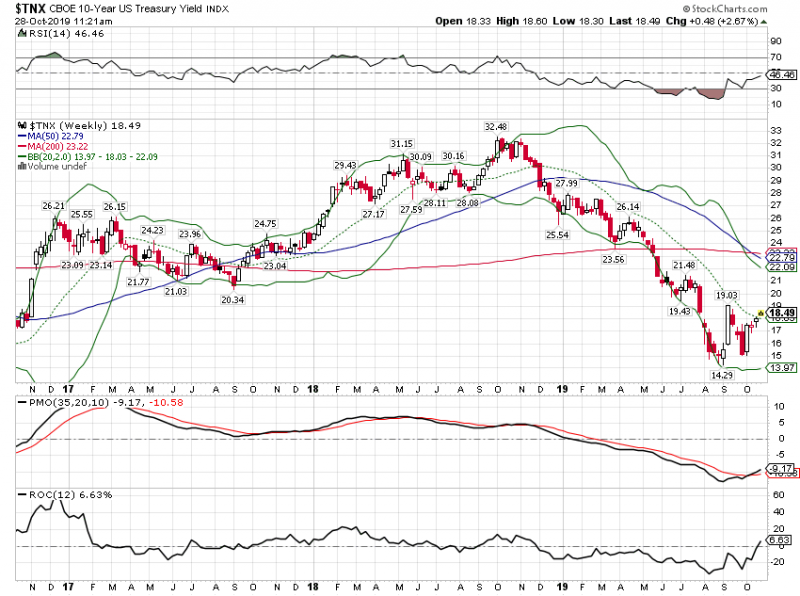

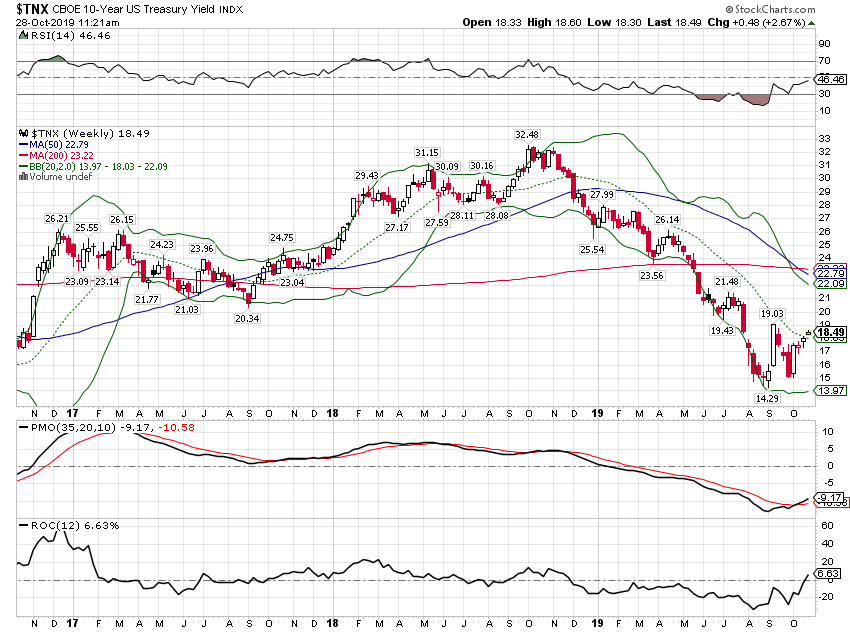

Three (Rate Cuts) And GDP, Where (How) Does It End?1 Nov 2019

Monthly Macro Monitor: Market Indicators Review

Monthly Macro Monitor: Market Indicators Review30 Oct 2019