Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

Weekly Market Pulse: Good News, Bad News

Weekly Market Pulse: Good News, Bad News14 Nov 2022

Weekly Market Pulse: Just A Little Volatility

Weekly Market Pulse: Just A Little Volatility17 Oct 2022

Inflation Protection Strategies You Need to Implement Now

Inflation Protection Strategies You Need to Implement Now13 Apr 2022

The Black Friday Stock Market Crash – Gareth Soloway

The Black Friday Stock Market Crash – Gareth Soloway30 Nov 2021

The Real Tantrum Should Be Over The Disturbing Lack of Celebration (higher yields)3 Nov 2021

The Enormously Important Reasons To Revisit The Revisions Already Several Times Revisited29 Oct 2021

They’ve Gone Too Far (or have they?)10 Jan 2021

Re-recession Not Required12 Sep 2020

Macro Housing: Bargains and Discounts Appear24 Oct 2019

Head Faking In The Empty Zoo: Powell Expands The Balance Sheet (Again)9 Oct 2019

The Consequences Of ‘Transitory’8 Oct 2019

ISM Spoils The Bond Rout!!! Again5 Oct 2019

ISM Spoils The Bond Rout!!!3 Oct 2019

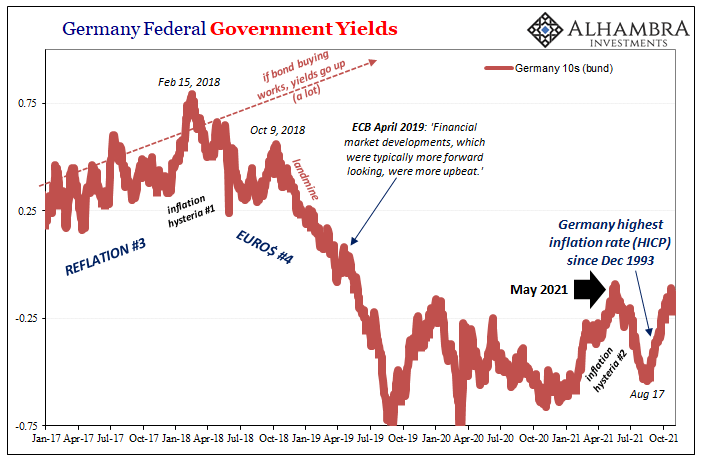

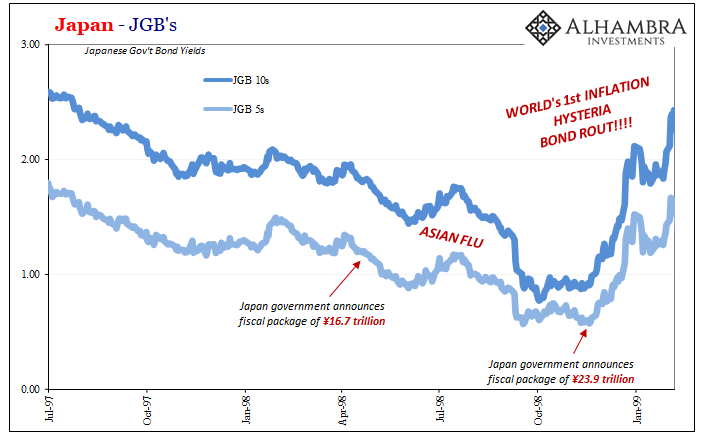

Japan: Fall Like Germany, Or Give Hope To The Rest of the World?29 Aug 2019

Germany’s Superstimulus; Or, The Familiar (Dollar) Disorder of Bumbling Failure24 Aug 2019

Why You Should Care Germany More and More Looks Like 200914 Aug 2019

Irredeemable Currency Is a Roach Motel, Report 9 June

Irredeemable Currency Is a Roach Motel, Report 9 June10 Jun 2019

Europe Comes Apart, And That’s Before #430 May 2019

China’s Nuclear Option to Sell US Treasurys, Report 19 May

China’s Nuclear Option to Sell US Treasurys, Report 19 May21 May 2019

Not Buying The New Stimulus8 Mar 2019

Inflation Protection Strategies You Need to Implement Now

2022-04-13

by Stephen Flood

2022-04-13

Read More »