Read More »

Category Archive: 1) SNB and CHF

The IMF Assessment for Switzerland 2014 and our critique

Read More »

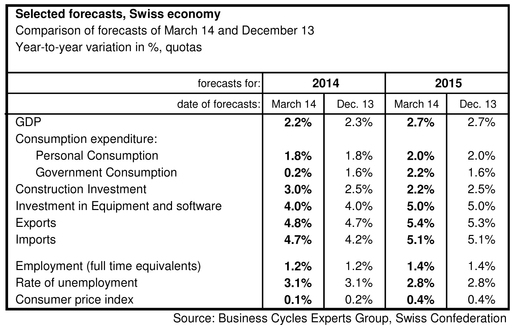

SECO expects 2.2% Swiss growth, further CHF strength ahead, understand why

Read More »

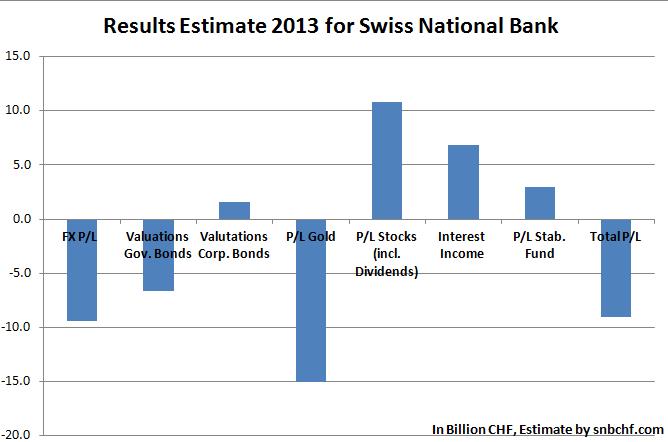

2013 SNB’s Valuation Gains 14 billion CHF on Stocks, but Losses of 35 bln. on Gold, FX and Bonds

Read More »

SNB Q1/2014 Results: 1.7% annualized Yield on Seigniorage, 2% annualized Loss on FX Rate Change

Read More »

15 Billion SNB Losses on Gold in 2013, But 40 Billion SNB Profit on Gold between 2000 and 2012

Read More »

George Dorgan bei den Jungfreisinnigen Zürich, Teil 1: CHF und Schweizer Wirtschaft

Read More »

George Dorgan at Swiss Young Liberals: Slides

On Friday the 7th of February at 19.00, George Dorgan is presenting his outlook on the Swiss Franc. He explains if and when the Swiss National Bank is able to generate profits again. Moreover he discusses the influence of the two referendums “Save Our Swiss Gold” and “Against Mass Immigration” on the Swiss Franc and …

Read More »

Read More »

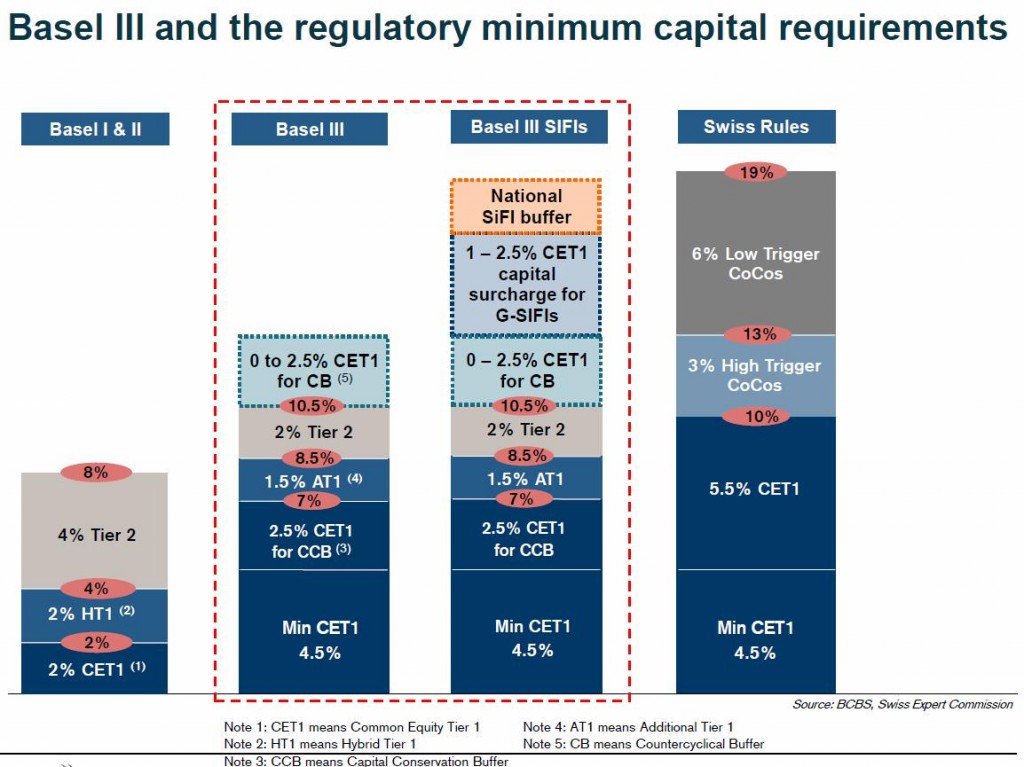

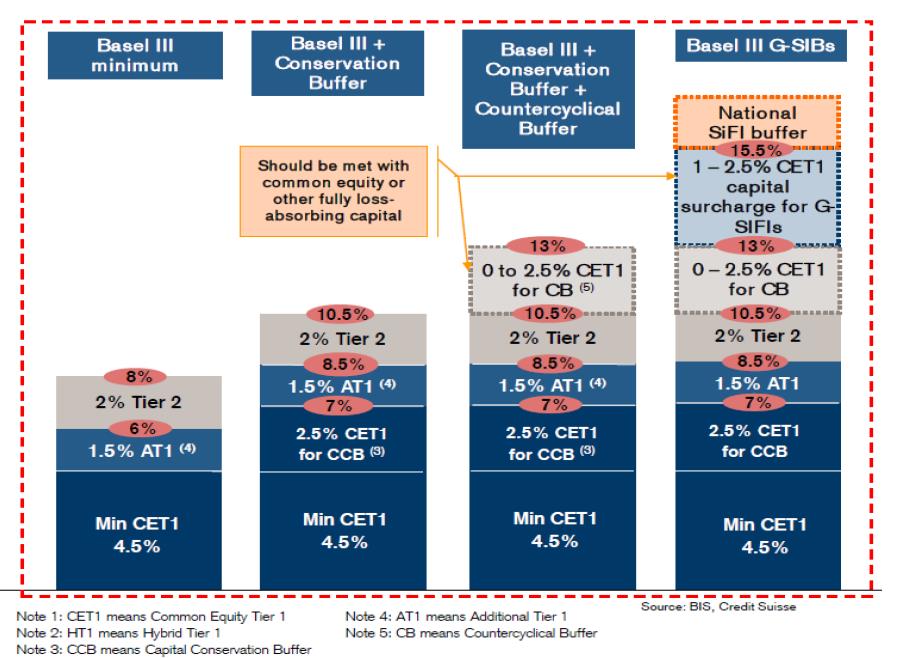

SNB Increases Weight of Countercyclical Capital Buffer for Banks

Read More »

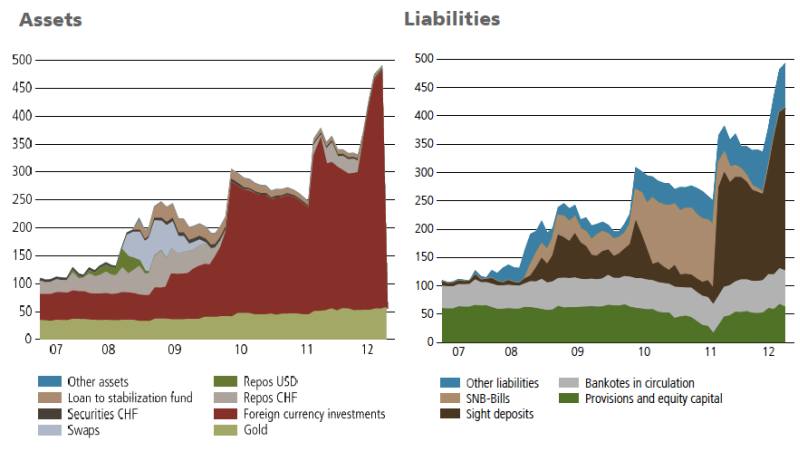

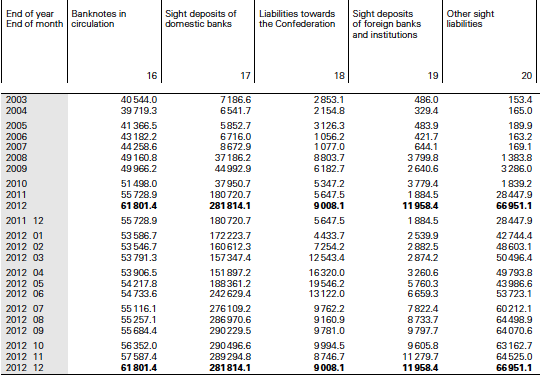

SNB Balance Sheet Expansion

Read More »

Swiss National Bank Monetary Policy Mandate – 2007 version vs. today

The mandate of the Swiss National Bank is concentrated on price stability, i.e. less than 2% inflation and to avoid deflation.

Read More »

Read More »

ECB rate cut creates complex situation for SNB

Read More »

Weekly Newspaper on Swiss National Bank and Swiss Franc

Feel free to click into the other categories “politics”, “business”, #chf, #snb in order to see more articles.

Read More »

Read More »

Fast CHF and Gold Price Movements

Read More »

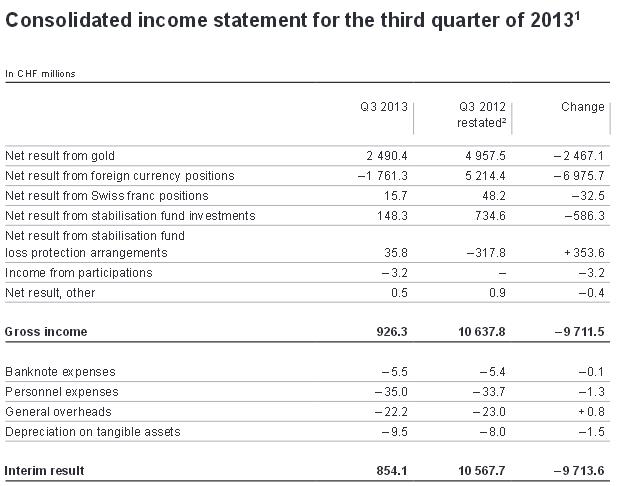

In Which Positions Does the SNB Win and Where Does it Lose Money: Details on the Q3 Results

Read More »

On Swiss National Bank

-

SNB’s Chairman Schlegel: A few months of negative inflation wouldn’t be a problem

-

2025-07-31 – Interim results of the Swiss National Bank as at 30 June 2025

-

SNB Brings Back Zero Percent Interest Rates

-

Hold-up sur l’eau potable (2/2) : la supercherie de « l’hydrogène vert ». Par Vincent Held

-

2025-06-25 – Quarterly Bulletin 2/2025

Main SNB Background Info

Featured and recent

-

Volatilität verstehen & Optionsprämien nutzen

Volatilität verstehen & Optionsprämien nutzen -

2026 Niue Star Wars Darth Vader Silver Coin

2026 Niue Star Wars Darth Vader Silver Coin -

Iran vs. USA – Ist Trump kein Friedenspräsident?! #thorstenwittmann #trump #trumpnews #irankonflikt

Iran vs. USA – Ist Trump kein Friedenspräsident?! #thorstenwittmann #trump #trumpnews #irankonflikt -

Spritpreise steigen – und der Staat verdient mit

Spritpreise steigen – und der Staat verdient mit -

3-31-26 Are Markets Becoming Gambling?

3-31-26 Are Markets Becoming Gambling? -

Zweite Inflationswelle: Wie du dich jetzt vorbereiten kannst!

Zweite Inflationswelle: Wie du dich jetzt vorbereiten kannst! -

Why Gold Is Failing As A Safe Haven

-

Collien Fernandes: Brutale Wahrheit! Spanische Staatsanwälte wollen NICHT ermitteln!

Collien Fernandes: Brutale Wahrheit! Spanische Staatsanwälte wollen NICHT ermitteln! -

Wichtige Morning News mit Oliver Klemm #558

-

Advice I Would Give My Younger Self

Advice I Would Give My Younger Self

More from this category

- 12) Switzerland Information

2 Jul 2025

Swiss Post Prices 2025 in One Table

Swiss Post Prices 2025 in One Table28 May 2025

- REIT Return and Dividend Yield

11 May 2020

- Gewinnerzielung 2019

28 Feb 2019

- Cookie policy

24 May 2018

- Privacy Policy

18 May 2018

- Repo and Repo Markets

23 Mar 2018

- Investor Relations

28 Feb 2018

The Secret History Of The Banking Crisis

The Secret History Of The Banking Crisis14 Aug 2017

- 100 Years Ago, Russian Stocks Had A Very Bad Day

28 Mar 2017

If It Didn’t Abandon The Gold Standard, U.S. Empire Would Have Collapsed…

If It Didn’t Abandon The Gold Standard, U.S. Empire Would Have Collapsed…19 Feb 2017

Sound Money and Your Personal Finances

Sound Money and Your Personal Finances24 Jan 2017

Pension Funds Need Gold before It’s Too Late

Pension Funds Need Gold before It’s Too Late19 Jan 2017

Rich Middle Class, Poor Middle Class

Rich Middle Class, Poor Middle Class15 Dec 2016

200 Russian Propaganda Sites, or simply alternative media?

200 Russian Propaganda Sites, or simply alternative media?10 Dec 2016

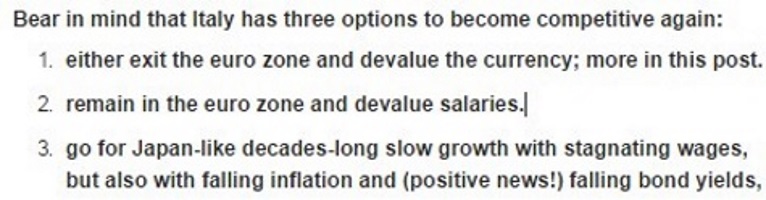

Italian Euro Exit: Why it Might Come in some Years and Why it Will Help the Euro Zone and Italy

Italian Euro Exit: Why it Might Come in some Years and Why it Will Help the Euro Zone and Italy5 Dec 2016

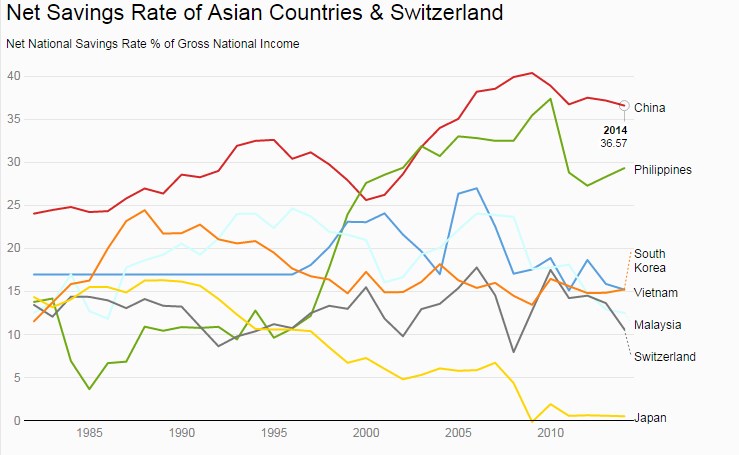

Net National Savings Rate, the Best Alternative Indicator to GDP Growth

Net National Savings Rate, the Best Alternative Indicator to GDP Growth4 Dec 2016

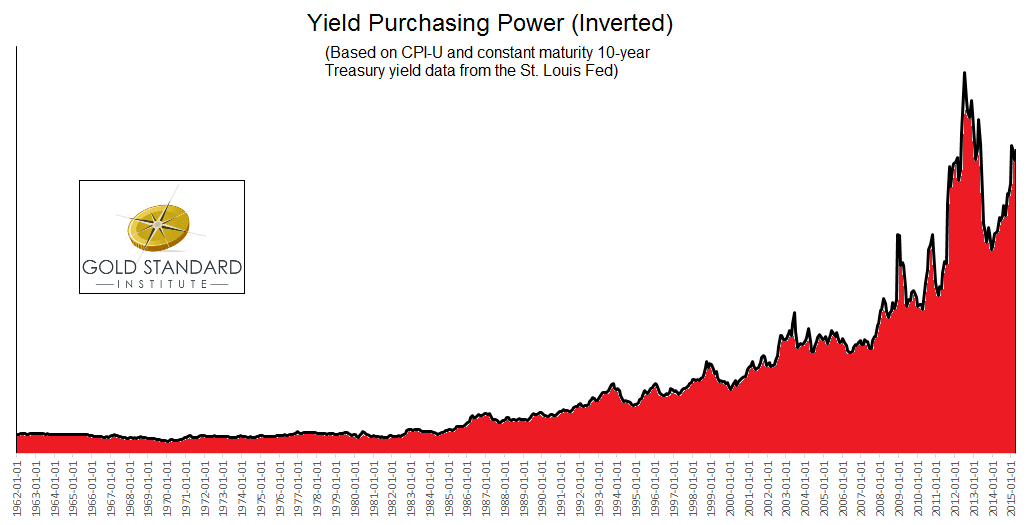

Introducing Yield Purchasing Power, the Video

Introducing Yield Purchasing Power, the Video26 Oct 2016

50 Slides for Gold Bulls – The Full Chart Book

50 Slides for Gold Bulls – The Full Chart Book25 Oct 2016

- Fragenkatalog für Privathaftpflichtversicherungen

8 Oct 2016