The standard line among most economists is that deflation is as bad or even worse than inflation. In reality, the economy needs deflation now more than ever.

Read More »2026-05-19

2026-05-19

The standard line among most economists is that deflation is as bad or even worse than inflation. In reality, the economy needs deflation now more than ever.

Read More »2026-05-18

The standard line among most economists is that deflation is as bad or even worse than inflation. In reality, the economy needs deflation now more than ever.

Read More »2026-05-11

From Monetarists to advocates of modern monetary theory, government edicts give money its value. Austrian economists from Menger to Mises to Rothbard know better.

Read More »2026-05-04

Politicians love to claim they are cutting taxes all the while running up ruinous debts and deficits. If they wish to get serious about cutting taxes, they first need to cut spending.

Read More »

Politicians love to claim they are cutting taxes all the while running up ruinous debts and deficits. If they wish to get serious about cutting taxes, they first need to cut spending.

Read More »2026-04-27

Some economists have claimed that “transparent” monetary policy in which the Fed operates predictably will lessen the chances of the boom and bust cycles happening. It isn’t the lack of transparency that creates business cycles; it is Fed-caused malinvestments.

Read More »2026-04-20

Whenever there is an economic problem, politicians in knee-jerk response blame private monopolies. The problem isn’t monopolies; the problem is government.

Read More »2026-04-13

When inflation heats up because central banks hold interest rates to artificially low levels, the standard approach is for central banks to increase interest rates. The better policy is not to artificially manipulate interest rates at all.

Read More »2026-04-06

Are rising oil prices responsible for inflation? While some economists and many in the media make that connection, the reality is much different. Inflation occurs because of expansion of the money supply.

Read More »2026-03-30

People claim to support economic intervention because the market cannot be trusted to be “stable” enough to keep the economy out of recessions. However, it is government itself, not the free market, which creates the instability in the first place.

Read More »2026-03-23

The so-called money multiplier that exists through fractional reserve banking is propped up by central banking and inflation. It is not a good thing for the economy.

Read More »2026-03-16

Milton Friedman and others tried to explain interest rates using liquidity, economic activity, and inflation expectations. These things, however, only describe interest but do not explain it. Only the Austrian theory of time preference correctly explains interest.

Read More »

Milton Friedman and others tried to explain interest rates using liquidity, economic activity, and inflation expectations. These things, however, only describe interest but do not explain it. Only the Austrian theory of time preference correctly explains interest.

Read More »2026-03-09

Although Federal Reserve policies are claimed to try to target the neutral rate of interest, it is not possible for that to be accomplished through monetary central planning.

Read More »2026-03-02

The yield curve is not easily understood, but it is important in giving us a good look at what is happening in the economy. Not surprisingly, Austrian economists are way ahead of the others in explaining the how and why of the curve.

Read More »2026-02-24

Keynesians claimed that stagflation—rising price levels and increasing rates of unemployment—couldn’t happen. Then it happened time and again, something predicted and coherently explained by Austrian economists.

Read More »2026-02-16

Mainstream economics and finance theories hold that markets immediately adjust to new information. While market prices do reflect available information, the Efficient Market Hypothesis (EMH) fails to explain the boom-bust cycle as well as Austrian analysis.

Read More »2026-02-09

Critics of the Austrian Business Cycle Theory claim that capital investors over time will no longer be fooled by artificially-low interest rates triggered by central banks. However, when central banks push easy money policies, the inflation itself sets the ABCT pattern in motion.

Read More »2026-02-02

One of the Austrian arguments against using mathematics to model economic phenomena is that there are no constants in economics, as things always are changing.

Read More »2026-01-26

Historical data is not enough for economists to make sense of it. Instead, that data must be viewed through a theoretical framework that explains what has happened.

Read More »2026-01-19

Economists consider probability to be central to economic analysis, but, as Ludwig von Mises wrote, economic action involves unique and purposeful events, not random ones.

Read More »2026-01-12

Most economists subscribe to a belief in “positive economics,” which means that economic theory flows from economic data. Thus, all theory can be tested for falsification at any time. Austrian economics, however, begins with economic theory, which is used to interpret the real world.

Read More »2026-01-05

While most economists believe that central banks set interest rates, in reality, they are set by time preferences of individual actors in the economy. Central bank influences on interest rates ultimately result in setting off boom-and-bust cycles.

Read More »2025-12-29

The Austrian economics framework shows that subjective valuation is not shown to be arbitrary, but rather purposeful, as people place values on things via a means-end framework.

Read More »2025-12-22

Financial bubbles, which used to be rare, have become a way of life, thanks to a quarter century of easy money policies from the Federal Reserve System. We need to better understand how bubbles form and why they are so harmful.

Read More »

Financial bubbles, which used to be rare, have become a way of life, thanks to a quarter century of easy money policies from the Federal Reserve System. We need to better understand how bubbles form and why they are so harmful.

Read More »2025-12-15

While Modern Portfolio Theory (MPT) is popular in academic economics and finance, it fails to properly explain profits, mistakenly confusing entrepreneurial profit seeking with risk management.

Read More »

While Modern Portfolio Theory (MPT) is popular in academic economics and finance, it fails to properly explain profits, mistakenly confusing entrepreneurial profit seeking with risk management.

Read More »2025-12-08

Modern economists attempt to define money by correlating it with economic activity. As Austrian economists know, money is defined by its function as a medium of exchange.

Read More »2025-11-24

It is an article of faith in mainstream economics that an economy cannot grow without a growing money supply. Yet, that is a false narrative, as increasing the supply of money over time ultimately sparks inflation and triggers business cycles.

Read More »

While the NBER collects economic data ostensibly to aid policymakers, the data it acquires is useless without proper economic theory to correctly interpret the numbers.

Read More »2025-11-17

Keynesian orthodoxy claims that the cause of recessions is a decline in so-called aggregate demand. Besides confusing cause-and-effect, Keynesians don’t understand that downturns are the result of malinvestments made during the boom because of central bank interference in the economy.

Read More »2025-11-10

Contra the recent winners of the Nobel Memorial Prize in economics, free markets, private savings, and entrepreneurship not so-called innovation, is what drives a market economy.

Read More »2025-11-03

The “greedflation” commentators are at it again, claiming that corporate profits are driving inflation. That is a logical impossibility.

Read More »2025-10-27

When economists try to analyze the economy, one procedure is to remove the “seasonal” component from the data in order to account for trends and fluctuations. That collides with the thinking behind praxeology in which human beings engage in purposeful behavior.

Read More »2025-10-20

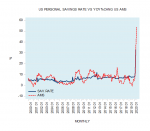

Ever since the Great Depression, most economists have claimed that the key to increasing economic growth is to lower unemployment. However, increasing the savings rate and building a capital structure are the keys to growth—and lower unemployment.

Read More »2025-10-13

After central bank expansionary efforts have unleashed inflation, officials then seek to contract the money supply in an attempt to undo the inflationary damage. No contractionary policy, however, can fix the problems caused by monetary manipulation.

Read More »2025-10-06

Milton Friedman and the Monetarists believed that fluctuations in the money supply caused the boom-and-bust business cycles. Their solution—keeping money growth slow and steady—would still lead to business cycles.

Read More »2025-10-03

According to mainstream economists, inflation aids economic growth while deflation impairs growth. Austrian economists, however, point out that in much of US history, economic growth was accompanied by deflation.

Read More »2025-09-29

According to mainstream economists, inflation aids economic growth while deflation impairs growth. Austrian economists, however, point out that in much of US history, economic growth was accompanied by deflation.

Read More »2025-09-22

Lower interest rates can help promote economic growth—as long as those rates are determined by the market and not by political edict.

Read More »2025-09-15

Inflation isn’t just about higher prices. It is how unwarranted increases in the money supply touches off wealth transfers from those who are less-well off to people who are close to the new injections of money into the economy.

Read More »2025-09-08

Austrian economists differ with the economic mainstream in many ways, but the break on utility theory is especially critical in understanding the split between the two schools of economic thought.

Read More »2025-09-01

In an attempt to explain business cycles, Milton Friedman came up with a plucked-string analogy. Like all Monetarist theories, however, this also had fatal flaws.

Read More »2025-08-25

Keynesian economists claim government budget surpluses are national savings, but real savings drive capital development. A surplus just means more revenue to the government, not the private economy.

Read More »2025-08-11

Mainstream economists claim that they can use econometric models to emulate human action and, thus, create an economic laboratory. These models, however, cannot tell us about cause-and-effect, which is vital to understanding praxeology and economic behavior.

Read More »

Mainstream economists claim that they can use econometric models to emulate human action and, thus, create an economic laboratory. These models, however, cannot tell us about cause-and-effect, which is vital to understanding praxeology and economic behavior.

Read More »2025-08-04

Thanks for modern Keynesian economics, most people believe money gains its value from the government that issues it. Money’s value, however, is historically tied to the value of the commodity from which money was derived.

Read More »

Thanks for modern Keynesian economics, most people believe money gains its value from the government that issues it. Money’s value, however, is historically tied to the value of the commodity from which money was derived.

Read More »2025-07-28

Surveys used to gauge optimism or pessimism about the economy may be interesting to read, but unless they are the product of sound and realistic economic theory, they are not economically useful.

Read More »

Surveys used to gauge optimism or pessimism about the economy may be interesting to read, but unless they are the product of sound and realistic economic theory, they are not economically useful.

Read More »

Instead, what matters is not whether expectations are stable, but whether expectations correspond to reality. Stable expectations cannot undo the damage caused by loose monetary and fiscal policies.

Read More »2025-07-21

Austrian economics veers sharply from the economic mainstream over the use of mathematics and quantitative measures. Instead, Austrians build upon irrefutable premises based upon human action.

Read More »

Austrian economics veers sharply from the economic mainstream over the use of mathematics and quantitative measures. Instead, Austrians build upon irrefutable premises based upon human action.

Read More »2025-07-14

The Efficient Market Hypothesis claims that financial markets process information immediately and correctly. However, since the EMH is based upon unrealistic assumptions, we also have to question the efficacy of this hypothesis, especially when central banks intervene in the markets.

Read More »

The Efficient Market Hypothesis claims that financial markets process information immediately and correctly. However, since the EMH is based upon unrealistic assumptions, we also have to question the efficacy of this hypothesis, especially when central banks intervene in the markets.

Read More »2025-07-07

Monetarists have long believed that the Fed should pursue policies of low inflation in order to counter the effects of lower prices through enhanced productivity. Thus, they reason, overall prices will remain stable. Such policies actually promote economic instability.

Read More »

Monetarists have long believed that the Fed should pursue policies of low inflation in order to counter the effects of lower prices through enhanced productivity. Thus, they reason, overall prices will remain stable. Such policies actually promote economic instability.

Read More »2025-06-30

A recession is defined by negative economic activity over several months with an accompanying decline in GDP. However, given the actual makeup of GDP, it is inaccurate to directly tie recessions to GDP at all.

Read More »

A recession is defined by negative economic activity over several months with an accompanying decline in GDP. However, given the actual makeup of GDP, it is inaccurate to directly tie recessions to GDP at all.

Read More »2025-06-23

Monetarists and rational expectations economists believe that if monetary policy is transparent, then increases in the money supply will not have negative effects. The actual results say otherwise, as introducing new money into the economy leads to economic instability.

Read More »2025-06-16

We speak of the “economy” as though it produces goods. Yet, the term really is a fiction, as purposeful individuals working in cooperation with each other are the real producers.

Read More »2025-06-09

Modern macroeconomic theory claims that government spending, taxation, and monetary creation is essential for economic growth. Austrian Economists, however, note that government stifles the economy.

Read More »2025-06-02

The mainstream economic belief is that a growing economy needs a growing money supply to ensure “price stability.” Austrian economists, however, believe that there is no “optimum” money supply, which means government should not engage in monetary expansion.

Read More »2025-05-27

A free market economy does not generate jobs or money. Instead, it creates wealth through exchange and production. Government intervention, contrary to what mainstream economists believe, does not enhance wealth, but instead destroys it.

Read More »2025-05-26

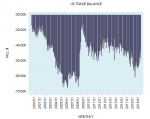

What if US trade deficits don’t matter?

Read More »

The Trump administration has pursued a high tariff policy, reversing the movement to lower trade barriers around the world. The justification for this policy is the presence of trade deficits with other nations. However, what if US trade deficits don’t matter?

Read More »2025-05-19

People often confuse economic growth with growth in the stock market, but while these two things can be related, that is not always the case, especially during inflationary times.

Read More »2025-05-13

A free market economy does not generate jobs or money. Instead, it creates wealth through exchange and production. Government intervention, contrary to what mainstream economists believe, does not enhance wealth, but instead destroys it.

Read More »2025-05-12

A free market economy does not generate jobs or money. Instead, it creates wealth through exchange and production. Government intervention, contrary to what mainstream economists believe, does not enhance wealth, but instead destroys it.

Read More »2025-03-31

Many believe the key cause to a general increase in prices are so-called “inflationary expectations.” For instance, if there is a large increase in the prices of oil, individuals will start forming expectations for higher inflation ahead. Consequently, individuals will speed up their purchases of goods and services at present, thereby raising the demand for goods and services, all other things being equal. This is supposed to set in motion general price increases. According to the former Fed Chairman Ben Bernanke, “Undoubtedly, the state of inflation expectations greatly influences actual inflation and thus the central bank’s ability to achieve price stability.”It is believed that, if inflationary expectations could be made less responsive to various shocks, then, over time, this would

Read More »2025-02-25

According to the Modern Monetary Theory (MMT), money is something decided by the state. The MMT regards money as a token. For instance, when an individual places a coat in the cloakroom of a theater, he receives a tin disc or a paper receipt. This receipt or a disc is a proof that the individual is entitled to demand the return of his coat.According to the MMT, the material used to manufacture the tokens is irrelevant—it can be gold, silver, or any other metal or it can even be paper. Hence, the definition of money, according to the MMT, is what the state decides it is going to be. MMT posits that the value of money is the outcome of the state that forces people to pay taxes with the money tokens that the state has decided upon. The state taxes have to be paid with the money tokens issued

Read More »2025-02-17

Often various factors are perceived to be important in determining a currency rate of exchange. For instance, for some commentators an increase in the government foreign debt is regarded as pointing to a likely deterioration in economic fundamentals ahead. This provides the rationale for the selling of the currency of concern.For many economists, the state of the balance of trade is a key factor in the currency exchange rate determination. On this way of thinking, all other things being equal, an increase in imports, which leads to a trade deficit, causes an increase in the demand for foreign currency. To obtain the foreign currency, importers sell the domestic currency for it. As a result, this causes a strengthening in the exchange rate of the foreign currency against the domestic

Read More »2024-12-23

Could an increase in the demand for money counteract the effect of an increase in the money supply? For example, if there were an increase in the supply of apples by ten and, simultaneously, an increase in the demand for ten apples, this would be completely absorbed. In other words, after individuals have satisfied their demand for ten apples, zero apples would be left.Following this logic, it would appear that the increase in the supply of money could be nullified by an equivalent increase in the demand for money. Henceforth, for the economy to stay in stable condition, it is important that the increase in the demand for money is matched by the similar increase in the supply. Consequently, if the increase in the demand for money is not met by the increase in the corresponding supply, this

Read More »2024-12-18

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-12-15

Many assume an individual’s valuation scale, which is in his head, determines his choices. The decision to buy or not to buy a particular good is subjective valuation. Since the buying of goods is not linked to any particular goal, this buying is of a random nature. From this it may appear that subjective valuations are of an arbitrary nature. But is this the case?According to Murray Rothbard, valuations do not exist independently. Valuations are not even primarily about the “things” valued. Valuation is the outcome of the mind valuing things. It is a relation between the mind and things. According to Carl Menger, an individual ranks goods in accordance to the importance of serving a given subjective goal. Various ends that an individual finds important in a moment are valued in a

Read More »

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-12-09

Many economists wrongly assume economic activity is accurately presented as a circular flow of money. Spending by one individual becomes part of the earnings of another individual; spending by another individual becomes part of the first individual’s earnings.

Read More »2024-12-03

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-12-02

For most commentators, a “stable price level” is the key for economic stability. For instance, let us say that there is a relative increase in consumer demand for potatoes versus tomatoes. This relative increase is depicted, all things being equal, by the relative increase in the price of potatoes. To be successful, businesses must pay attention to consumer demand. Failing to do so is likely to lead to losses. Hence, by paying attention to relative changes in prices, producers are likely to increase the production of potatoes versus tomatoes.According to many economists, if the “price level” is not “stable,” then the visibility of the relative price changes becomes blurred and, consequently, businesses cannot ascertain the relative changes in the demand for goods and services and make

Read More »

For most commentators, a “stable price level” is the key for economic stability. For instance, let us say that there is a relative increase in consumer demand for potatoes versus tomatoes. This relative increase is depicted, all things being equal, by the relative increase in the price of potatoes. To be successful, businesses must pay attention to consumer demand. Failing to do so is likely to lead to losses. Hence, by paying attention to relative changes in prices, producers are likely to increase the production of potatoes versus tomatoes.According to many economists, if the “price level” is not “stable,” then the visibility of the relative price changes becomes blurred and, consequently, businesses cannot ascertain the relative changes in the demand for goods and services and make

Read More »2024-12-01

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-11-25

According to the Austrian Business Cycle Theory (ABCT), the artificial increase in the money supply via central bank expansionary monetary policy lowers the market interest rate. This, in turn, causes the market interest rate to deviate from the natural rate, determined by the market. Consequently, this leads to the boom-bust cycle. Understanding this, on the gold standard, where money is gold and—assuming that there is no central bank—an increase in the supply of gold will also result in the lowering of the market interest rates.This would cause a deviation of the market interest rates from the previous interest rate. Consequently, this is going to set in motion a boom-bust cycle. This means that even on the gold standard, without the central bank, we could still have boom-bust cycles.

Read More »2024-11-19

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-11-18

Popular understandings of economics often attempt to incorporate the methodology of natural sciences as the supposed key to economics. Some economic experts are of the view that the methods employed by the natural sciences, such as advanced mathematics, are important tools for the assessments of historical data to establish the state of an economy.

Read More »2024-11-11

Assumptions that some economists are employing in their theories appear to be detached from the real world. For example, in order to explain the economic crisis in Japan, Paul Krugman employed a theory based on the assumptions that people are identical and live forever. Whilst admitting that these assumptions are not realistic, Krugman nonetheless is of the view that somehow his theory could be useful in offering solutions to the economic crisis in Japan. Thus, Krugman wrote,The purpose of this paper is to demonstrate possibilities and clarify thinking, rather than to be realistic…. In this model individuals are identical and live forever, so that there are no realistic complications involving distribution within or between generations; output is simply given.If Krugman’s theory is not

Read More »

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-11-04

On September 18, 2024 the Federal Reserve (“Fed”) lowered its policy interest rate target by 0.5 percent to 5 percent. Most commentators, including the Fed chairman Jerome Powell, hold that the lowering of the policy rate is going to strengthen the economy. This way of thinking is based on the view that the lowering of interest rates is going to strengthen the demand for goods and services. As a result, this would strengthen the production of goods and services (i.e., generate economic growth). Supposedly, an increase in the demand precedes an increase in the supply—sets in motion economic production.But is this the case?Why supply precedes demand? In the market economy, producers do not produce everything for their own consumption. Part of their production is used to exchange for the

Read More »2024-10-27

Individuals are often presented as if a value scale is hard-wired in their heads. Allegedly, this value scale remains the same all the time. As a result, this value scale supposedly instructs individuals in the selection of goods. Were that the case, then it makes sense to attempt to extract this value scale either by means of questionnaires or various psychological tests. Once the value scale is extracted, social scientists could establish how to allocate scarce resources in the most efficient way.According to Murray Rothbard, there can be no valuation without things to be valued. Value is established once an individual’s mind has interacted with a particular entity. The evaluation process then establishes for what end, or purpose, a particular entity could be of use. On this Carl Menger

Read More »2024-10-21

Why are individuals willing to pay higher prices for some goods relative to other goods? The common reply to this appeals to the laws of supply and demand. But what is behind these laws? To provide a further answer to this question economists refer to the law of diminishing marginal utility. Mainstream economics explains this law in terms of the satisfaction that one derives from consuming a particular good. For instance, an individual may derive vast satisfaction from consuming one cone of ice cream. The satisfaction he will derive from consuming a second cone might also be large but not as large as the satisfaction derived from the first cone. The satisfaction from the consumption of a third cone is likely to diminish further, and so on.From this, mainstream economics concludes that the

Read More »2024-10-18

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-10-14

Most experts agree that, through the manipulation of the short-term interest rates, the central bank can also determine the direction of the long-term interest rates. Some popular thinking alleges that the long-term interest rates are the average of the present and the expected short-term interest rates. Hence, it would appear that the central bank is the key in determining the interest rates. But is this valid?Individual time preferences and interest ratesAccording to thinkers such as Carl Menger and Ludwig von Mises, interest is the outcome of the fact that individuals assign a premium to present goods against identical goods in the future (i.e., time preference). The preference is not the result of capricious behavior but because life in the future is not possible without sustaining it

Read More »2024-10-11

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-10-07

Many incorrectly assume that the overall economy’s output increases by a multiple of the increase in expenditure by government, consumers, and businesses. For instance, if out of an additional dollar received individuals spend $0.90 and save $0.10, then if consumers spending were to increase by $100 million, it is held that the overall output in the economy is going to increase by the tenfold of the increase in consumers’ expenditure (i.e. by $1 billion). The following example provides the reasoning behind this way of thinking.Because of the increase in consumers’ expenditure by $100 million, retailers’ income increases by $100 million. Retailers, in response to the increase in their income, likewise spend 90% of the $100 million (i.e., they raise expenditure on goods by $90 million). The

Read More »2024-09-30

Many economists incorrectly assume a growing economy also requires a growing money stock, assuming that economic growth gives rise to a greater demand for money. It is held that failing to increase money to facilitate increased trade will lead to a decline in prices of goods and services, destabilizing the economy and leading to an economic downturn.Some commentators believe that the lack of a flexible mechanism coordinating demand versus the money supply is the major reason why the gold standard leads to instability. The idea is that, relative to the growing demand for money because of growing economies, the supply of gold does not grow fast enough. Thus, to prevent economic shocks from imbalances between the demand and the supply of money, the Fed must make sure that supply and demand

Read More »2024-09-26

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-09-24

Some have argued that new technological ideas, unlike material inputs and labor, are not in themselves scarce. Consequently, it is further argued that new ideas for more efficient processes and new products can make continuous economic growth possible. So-called experts, however, are of the view that in a fully competitive environment, firms are likely to be concerned that competitors are going to copy any innovations they introduce. Therefore, it is alleged that firms are likely to become reluctant to make costly investments in research and development.To deal with this problem, “experts” believe that it is necessary to introduce policies, such as subsidies, for research and development. Hence, it is concluded that government policies play a critical role in promoting technological

Read More »2024-09-19

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-09-16

It is widely held that financial asset markets always fully reflect all available and relevant information, and that adjustment to new information is virtually instantaneous. This way of thinking is also known as the Efficient Market Hypothesis (EMH), and is closely linked with the Rational Expectations Hypothesis (REH), which postulates that market participants are at least as good at price forecasting as is any model that a financial market scholar can come up with, given the available information.

Read More »2024-09-12

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-09-09

To gain insight into the state of an economy, most economists rely on a common statistic named the Gross Domestic Product (GDP). The GDP looks at the value of final goods and services produced during a particular period, usually a quarter or a year.Using this measurement statistic assumes that what drives the economy is not the production of goods and services, but rather consumption. In GDP, what matters is the demand for final goods and services. Since consumer outlays are the largest part of the overall demand, it is commonly held that consumer demand is the key productive factor in the economy. Because the supply of goods is taken for granted, this framework ignores the various stages of production that precede the emergence of final goods.Usage of GDP assumes goods emerge because of

Read More »2024-09-04

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-09-03

According to some “experts,” there is an urgent need to remove cash from the economy. It is held that cash provides support to the “shadow economy” and permits tax evasion. Another justification for its removal is that, in times of economic shocks, which push the economy into a recession, the run for cash exacerbates the downturn—it becomes a factor contributing to economic instability. Moreover, it is argued that, in the modern world, most transactions can be settled by means of electronic funds transfer. Money in the modern world is allegedly an abstraction.The emergence of moneyMoney emerged because barter could not support the market economy. A butcher, who wanted to exchange his meat for fruit, might not be able to find a fruit farmer who wanted his meat, while the fruit farmer who

Read More »2024-08-26

According to some commentators, to counter inflation interest rates in the US must increase to a level that effectively restrains the economy. It is held that this increase in interest rates does not have to cause a recession if Fed’s policy makers could orchestrate a “soft landing.” The economy is portrayed as a spaceship that occasionally deviates from a path of “stable” economic growth and “stable” prices. All that is required to fix the problem is for the central bank to give a suitable “push” to the economy (i.e., the spaceship) to bring it back to the right growth path.Thus, if the economy falls into a recession, the central bank is expected to bring it onto the “stable” growth path by artificially lowering interest rates. Conversely, if the economy appears to be “overheated,” the

Read More »2024-08-20

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-08-09

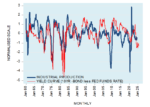

Many commentators consider the spread between the long-term interest rate and the short-term interest rate as an important indicator to establish the future course of economic activity. An increase in the spread is seen as pointing toward good economic times ahead. Conversely, a declining spread raises the likelihood of an economic recession.Historically, in the U.S., the differential between the yield on the 10-year T-bill and the federal funds rate was leading the yearly growth rate of industrial production by 12 months (see Figure 1).Figure 1: Year-over-year U.S. industrial production versus 12-month yield curve lag (%)Source: Federal Reserve Bank of St. Louis (FRED)A popular explanation for the determination of the shape of the yield spread is provided by expectations theory. According

Read More »2024-07-28

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-07-19

Monopolies are believed to undermine individuals’ well-being, including being the cause of large increases in the prices of goods and services. According to Jean Tirole, the 2014 Nobel winner in economics, monopolies undermine the efficient functioning of the market economy by influencing the prices and the quantity of products, making consumers worse off.

Thus, monopolies supposedly cause market conditions to deviate from the ideal state of “perfect competition.” Effective enforcement of government regulations, then, is needed to control monopolies. Tirole has devised methods to strengthen the regulation of industries dominated by a few large firms.

The ‘perfect competition’ model

In the world of perfect competition, the following features characterize a market:

There are many buyers and

2024-07-12

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-06-27

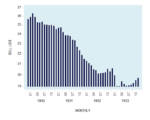

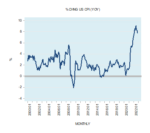

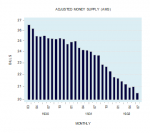

The leading monetarist, Milton Friedman, blamed the Federal Reserve System’s policies for causing the Great Depression of the 1930s. According to Friedman, the Fed failed to pump enough reserves into the banking system to prevent a collapse of the money stock. Because of this, Friedman held that M1, which stood at $26.34 billion on March 1930, fell to $19.00 billion by April 1933—a decline of 27.9 percent.Figure 1: US M1 money supply, 1930–33Source: Data from FRED.According to Friedman, as a result of the collapse in the money stock, economic growth followed suit. Year-over-year industrial production by July 1932 fell by over 31 percent (see chart). Also, year over year, the consumer price index plunged. By October 1932, the Consumer Price Index had declined by 10.7 percent.Figure 2:

Read More »2024-06-18

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-06-13

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-06-10

In the late 1960s Edmund Phelps and Milton Friedman challenged the popular view that there can be a sustainable trade-off between inflation and unemployment. In fact, over time, according to PF, loose central bank policies set the platform for lower economic growth and a higher rate of inflation, or stagflation.PF’s Explanation of StagflationStarting from a situation of equality between the current and the expected rate of inflation, the central bank decides to boost the rate of economic growth by raising the growth rate of money supply. As a result, a greater supply of money enters the economy and each individual now has more money at his disposal.Because of this increase, every individual believes he has become wealthier. This raises the demand for goods and services, which in turn sets

Read More »2024-06-03

Many economic commentators believe increasing the quantity of money can revive an economy. This is based on the view that with more money in their pockets, people will spend more and others follow suit, as they hold that money is a mere means of payments.Money, however, is not the means of payments but rather a medium of exchange. It only enables one producer to exchange his product for the product of another producer. According to Murray Rothbard, “Money, per se, cannot be consumed and cannot be used directly as a producers’ good in the productive process. Money per se is therefore unproductive; it is dead stock and produces nothing.” The means of payments are always goods and services, which pay for other goods and services. Money simply facilitates these payments as a medium of

Read More »2024-05-27

In order to make the data “talk,” economists utilize a range of statistical methods that vary from highly complex models to a simple display of historical data. It is generally believed that one can organize historical data through quantitative methods into a useful body of information, which in turn can serve as the basis for assessing the economy.Now, it has been observed that declines in the unemployment rate are associated with a general rise in the prices of goods and services. Should we then conclude that decreases in the unemployment rate trigger price inflation? To confuse the issue further, it has also been observed that price inflation is well-correlated with changes in money supply.What are we to make out of all this? How are we to decide which is the right theory? According to

Read More »2024-05-23

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-05-17

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-05-14

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »

Why does the dollar bill in our pocket have value? The value of money is established, according to some experts, because the government in power says so. For other commentators, the value of money is on account of social convention.The Difference between Money and Other GoodsDemand for a good arises from its perceived benefit. For instance, individuals demand food because of the nourishment it offers them. With regard to money, individuals demand it not for direct use in consumption but in order to exchange it for other goods and services. Money is not useful in itself, but because it has an exchange value, it is exchangeable in terms of other goods and services. Money is demanded because the benefit it offers is its purchasing power.Consequently, for something to be accepted as money it

Read More »2024-05-13

Popular thinking says that lending is banking activity. Banks are believed to be responsible for the expansion of credit. However, is this the case?The Meaning of CreditFor instance, take a farmer, Joe, who produced two kilograms of potatoes. For his own consumption, he requires one kilogram, and the rest he decides to lend for one year to a farmer named Bob. The unconsumed one kilogram of potatoes that he agrees to lend is his real savings.Note that the precondition of lending is that there must be real savings first. Lending must be fully backed up by real savings.By lending one kilogram of potatoes to Bob, Joe agrees to give up for one year his ownership over these potatoes. In return, Bob provides Joe with a written promise that after one year he will repay 1.1 kilograms of potatoes.

Read More »

Popular thinking says that lending is banking activity. Banks are believed to be responsible for the expansion of credit. However, is this the case?The Meaning of CreditFor instance, take a farmer, Joe, who produced two kilograms of potatoes. For his own consumption, he requires one kilogram, and the rest he decides to lend for one year to a farmer named Bob. The unconsumed one kilogram of potatoes that he agrees to lend is his real savings.Note that the precondition of lending is that there must be real savings first. Lending must be fully backed up by real savings.By lending one kilogram of potatoes to Bob, Joe agrees to give up for one year his ownership over these potatoes. In return, Bob provides Joe with a written promise that after one year he will repay 1.1 kilograms of potatoes.

Read More »2024-05-07

What is the Mises Institute?

The Mises Institute is a non-profit organization that exists to promote teaching and research in the Austrian School of economics, individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. Non-political, non-partisan, and non-PC, we advocate a radical shift in the intellectual climate, away from statism and toward a private property order. We believe that our foundational ideas are of permanent value, and oppose all efforts at compromise, sellout, and amalgamation of these ideas with fashionable political, cultural, and social doctrines inimical to their spirit.

Read More »2024-05-02

In our modern political culture, many people claim that profits are the outcome of some individuals exploiting other individuals. Hence, anyone who is seen trying to make profits is regarded as an enemy of society and must be stopped before inflicting damage. According to Henry Hazlitt, “The indignation shown by many people today at the mention of the very word profits indicates how little understanding there is of the vital function that profits play in our economy.”Furthermore, Hazlitt held,In a free economy, in which wages, costs and prices are left to the free play of the competitive market, the prospect of profits decides what articles will be made, and in what quantities—and what articles will not be made at all. If there is no profit in making an article, it is a sign that the labor

Read More »2024-04-26

Mainstream economists believe our knowledge of the world of economics is elusive, so the criteria for choosing a theory should be its predictive power. If the theory “predicts,” it is regarded as a valid framework to assess the economy. Once a theory fails in that role, the search for a new theory begins.For instance, an economist believes that consumer outlays on goods and services are determined by disposable income. Once this view is validated by statistical methods, it is used to assess the future direction of consumer spending. If the theory fails to produce accurate forecasts, it is either replaced or modified by adding some other explanatory variables. This way of thinking implies that our knowledge of the world of economics is elusive.Since we cannot establish “how things really

Read More »2024-04-04

The price or the rate of exchange of one good in terms of another is the amount of the other good divided by the amount of the first good. In the money economy, price will be the amount of money divided by the amount of the first good.Suppose two transactions were conducted. In the first transaction, one TV set is exchanged for $1,000. In the second transaction one shirt is exchanged for $40. The price or the rate of exchange in the first transaction is $1,000 per TV set. The price in the second transaction is $40 per shirt. Could we then establish the average price paid in these two transactions?In order to calculate the average price, we must add these two ratios and divide them by two. However, $1,000 per TV set cannot be added to $40 per shirt, implying that it is not possible to

Read More »2024-03-30

Some economists believe that the increase in the minimum wage will boost unemployment, while other economists think otherwise. Hence, they believe that raising the minimum wage would raise the living standards of workers.For example, in a study conducted in the 1990s, economists David Card and Alan Krueger examined a minimum-wage rise in New Jersey by comparing fast-food restaurants there and in an adjacent part of Pennsylvania, finding no impact on employment. Other economists, however, found that the increase in minimum wages increased employment. Given the contradictory results, is there an alternative approach to decide whether an increase in the minimum wage will result in an increase or reduction in employment?Can Historical Data Inform Us on How the Economy Works?Note that the

Read More »2024-03-14

Tu ne cede malis, sed contra audentior ito

Website powered by Mises Institute donors

Mises Institute is a tax-exempt 501(c)(3) nonprofit organization. Contributions are tax-deductible to the full extent the law allows. Tax ID# 52-1263436

Read More »2024-03-05

In an article in the New York Times on March 27, 2018, Paul Krugman argues that economists who believe increases in money supply cause inflation are wrong. According to Krugman, the key factor that sets inflation in motion is unemployment. While a decline in the unemployment rate is associated with an increase in the rate of inflation, an upsurge in the unemployment rate is associated with a decline in the rate of inflation.Krugman believes inflation is about general increases in the prices of goods and services, which we suggest is a flawed definition. To ascertain what inflation really is, we must establish how this phenomenon emerged, tracing it back to its historical origin.The Essence of InflationInflation is an act of embezzlement. Historically, inflation originated when a country’s

Read More »2024-02-26

Tu ne cede malis, sed contra audentior ito

Website powered by Mises Institute donors

Mises Institute is a tax-exempt 501(c)(3) nonprofit organization. Contributions are tax-deductible to the full extent the law allows. Tax ID# 52-1263436

Read More »

Some economists believe that the balance of payments is what determines currency exchange rates. In fact, exchange rates are always about the purchasing power of some currencies relative to others.

Original Article: Does the Balance of Payments Determine Exchange Rates?

2024-02-22

According to behavioral economics (BE), emotions play an important role in an individual’s decision-making process. For example, if consumers become more optimistic regarding the future, then this is going to send a message to businesses regarding investment decisions. According to BE followers, whether consumers are generally patient or impatient determines whether or not they are inclined to spend or save today.

Behavioral economists emphasize the importance of personality. An emphatic person is regarded more likely to make altruistic choices. Impulsive people are more likely to be impatient and not so good at saving up for their retirement. Venturesome people are more likely to take risks—they will be more likely to gamble.

If emotions are an important factor in the decision-making

2024-02-14

It is a common belief that a key factor in determining the currency exchange rate is the balance of payments. An increase in imports increases the demand for foreign currency. To obtain the foreign currency, importers buy it using domestic currency, which strengthens the exchange rate of the foreign currency against domestic money. Conversely, an increase in exports, in which exporters exchange their foreign currency earnings for domestic currency, increases the value of the domestic currency exchange rate against the foreign currency.

In this way of thinking, exporters determine the supply of foreign currency while importers determine the demand for it. Hence, the interaction between supply and demand establishes a foreign currency exchange rate.

Following this logic, one can conclude

2024-02-05

Most mainstream economists believe the application of quantitative methods on historical data can explain the state of the economy. Others such as Ludwig von Mises held that the data utilized by economists is a historical display, which by itself cannot provide the facts of economics. Ludwig von Mises wrote, “Experience of economic history is always the experience of complex phenomena. It can never convey knowledge of the kind the experimenter abstracts from a laboratory experiment.”

To make sense of historical data, economists must have a theory that stands on its own and does not originate from the data itself. Even economists who call themselves “practical” must employ a theory to make sense of historical data. Even seeking correlations between the various pieces of historical data is

2024-01-30

Government efforts to expand “aggregate demand” involve new spending and money creation. In reality, these activities destroy wealth in the name of expanding it.

Original Article: Does Government Spending and Money Expansion Create New Wealth or Destroy It?

When the economy goes into a recession, most economic commentators believe that the government and the central bank should take steps to counter the rise in unemployment. Some economists believe that lowering unemployment can be achieved without any cost, given that the unemployed workers are idle. According to Paul Krugman, “If you put 100,000 Americans to work right now digging ditches, it is not as if you are taking those 100,000 workers away from other good things they might be doing. You are putting them to work when they would have been doing nothing.”

But how will such a policy be funded? Who pays the unemployed for digging ditches? It seems that Krugman believes that funding can be easily generated by the central bank via money printing.

Now, funding is not about money as such but

2024-01-22

When an economy suffers a recession, some factors of production, such as labor, become unemployed. Keynesians believe that expanding credit and fiat money will bring back full employment. That’s not how an economy works.

Original Article: Can an Easy Money Policy Increase Employment of "Idle Resources"?

2024-01-19

Many economists claim that economic growth is driven by increases in the total demand for goods and services, additionally claiming that overall output increases by a multiple of the increase in expenditures by government, consumers, and businesses. Thus, it is not surprising that most economic commentators believe that a fiscal and monetary stimulus will strengthen total demand, preventing the US economy from falling into a recession.

These economists believe that increasing government spending and central bank monetary pumping will increase production of goods and services and strengthen total demand. This means that demand creates supply. However, is this the case?

Why Supply Precedes Demand

In the market economy, producers do not produce solely for their own consumption. Some of their

2024-01-12

While the creator of modern portfolio theory was awarded a Nobel Prize, that doesn’t mean the theory isn’t flawed. In fact, it explains very little about investments.

Original Article: Modern Portfolio Theory Is Mistaken: Diversification Is Not Investment

2024-01-11

Whenever an economy falls into a recession, many economists point out that the economic slump means there will be idle capital and labor. Resources that could be employed are now unemployed because the economic slump has softened aggregate demand for goods and services.

So-called experts believe the government must increase the overall demand in the economy since stronger demand will permit idle resources to be employed again. Hence, many economists recommend that the central bank adopt an easy monetary stance to strengthen aggregate demand.

It appears to be quite simple: boost expenditure on goods and services and this, in turn, will strengthen the overall output in the economy by the multiple of the expenditure, thanks to the Keynesian multiplier. According to Ludwig von Mises,

Here,

2023-12-27

According to modern portfolio theory (MPT), financial asset prices always fully reflect all available and relevant information, and any adjustment to new information is virtually instantaneous. Thus, asset prices respond only to the unexpected part of information since the expected portion is already embedded in prices.

For example, if the central bank raises interest rates by 0.5 percent, and if market participants anticipated this action, asset prices will reflect this expected increase prior to the central bank’s raising interest rates. Note that once the central bank lifts the interest rate by 0.5 percent, this increase will have no effect on asset prices since stock prices have already adjusted. However, should the central bank raise interest rates by 1 percent, rather than the 0.5

2023-12-20

According to the post-Keynesian School of Economics economist Hyman Minsky, the capitalist economy has an inherent tendency to develop instability that culminates in a severe economic crisis. The key mechanism that pushes the economy toward a crisis is the accumulation of debt.

According to Minsky, during “good” times businesses in profitable sectors of the economy are rewarded for increasing their debt levels. The more one borrows, the more profit one seems to make. The rising profit attracts other entrepreneurs and encourages them to raise their debt levels.

Since the economy is doing well and borrowers show visible improvements in their financial health, lenders are more eager to lend. Over time, however, the pace of debt accumulation starts to rise much faster than the borrower’s

2023-12-14

According to mainstream economists, the expectation of inflation leads to higher prices. That is impossible, however, because actual inflation involves real increases in the money supply.

Original Article: Inflationary Expectations Do Not Cause Inflation

2023-12-07

Econometric models are constructed with the idea that they can be substituted for authentic human action. Not surprisingly, they fail badly.

Original Article: Can Econometric Models Provide a Laboratory Setting for Economic Analysis?

Many people believe that a general increase in stock prices is an important factor in economic growth. However, this is a questionable observation.

The view that the stock market drives economic growth originates from the observation that changes in stock prices precede changes in economic data. We suggest that various economic indicators are heavily influenced by money supply, which also drives stock prices.

The price of something is the amount of money asked for per unit. When an increased money supply enters a market, more money is being paid for those goods, which means the prices of those goods have increased. Furthermore, when money is increasing in supply, it does not move instantly to all markets. Instead, it moves from one market to another with time lags. Furthermore, the time

2023-11-30

Many economists believe that inflationary expectations cause general increases in prices. For instance, if there is a sharp increase in oil prices, people will form higher inflationary expectations that set in motion general increases in the prices of other goods and services. According to the former Federal Reserve chairman Ben Bernanke, “Undoubtedly, the state of inflation expectations greatly influences actual inflation and thus the central bank’s ability to achieve price stability.”

Economists believe that if expectations could be made less responsive to various shocks, then over time this would mitigate the effects of these shocks on the momentum of the prices of goods and services. Many economic commentators think that central bank policies can bring inflationary expectations to a

2023-11-29

Forget the other mainstream explanations for interest. Time preference explains this phenomenon and gives a true picture of why interest exists in the first place.

Original Article: Time Preference Is the Key Driver of Interest Rates

2023-11-21

Econometric model building attempts to produce a laboratory with controlled variables. By means of mathematical and statistical methods, an economist establishes functional relationships between various economic variables.

For example, personal consumer outlays are related to personal disposable income and interest rates, while fixed capital investments are explained by the past stock of capital, interest rates, and economic activity. A group of such estimated relations constitutes an econometric model.

A comparison of the goodness of fit of the dynamic simulation versus the actual data is an important criterion in assessing the reliability of a model. (In a static simulation, the model is solved using actual lagged variables. In a dynamic simulation, the solution is obtained by employing

2023-11-16

Many economists, including Milton Friedman, have claimed that reality is elusive and that one cannot know its true nature. Most mainstream economists also believe that data gives us the state of the economy. By inspecting numbers such as gross domestic product (GDP) or the consumer price index, only then can an economist accurately assess the state of economic conditions.

Ludwig von Mises and the Austrian School of Economics have had a different view. According to Mises, the data is a historical display and, by itself, cannot provide the facts regarding the real world. To make sense of the data, one needs to have a theory beforehand that will allow one to interpret the data, and the theory must originate from something real that cannot be refuted. A theory resting on the foundation that

2023-11-12

The field of behavior economics downplays the role of purposeful praxeology in economics. Austrian economics does not make that error.

Original Article: Reason versus Emotion in Economics: A Praxeological Response

2023-11-09

By popular thinking, whenever the central bank raises the growth rate of the money supply through the buying of financial assets such as Treasuries this pushes the prices of Treasuries higher and their yields lower. This is labeled as the monetary liquidity effect. This effect is inversely correlated with interest rates.

Furthermore, an increase in the money supply after a time lag strengthens economic activity and this pushes interest rates higher. Note that we have here a positive correlation between economic activity and interest rates.

After a much longer time lag, the increase in the growth rate of money supply is starting to exert an upward pressure on the prices of goods and services. Once prices begin to move higher, the inflation expectations effect emerges. Consequently, this is

2023-11-02

The New York Federal Reserve said on Tuesday, September 5, 2023, that the estimate for the neutral rate for Q2 has eased to 0.57 percent from 0.68 percent in Q1. Analysts typically translate that rate into a real-world setting by adding the neutral rate to the Fed’s 2 percent inflation target. The current reading suggests that a federal funds rate of around 2.5 percent would represent a neutral setting. Given that the Fed’s current target rate range is between 5.25 and 5.5 percent, this suggests that the interest rate policy remains very restrictive.

Based on this, it is quite likely that the Fed will loosen its interest rate stance ahead. This view is further reinforced by the massive increase in the ratio of the federal funds rate target to the neutral rate of 9.2 in Q2 this year from

2023-10-28

Popular economic thinking holds that consumer spending is the most important driver of the economy. Actually, demand can’t exist without something first being supplied.

Original Article: Why Must Supply Precede Demand? Understanding Economic Foundations

2023-10-26

According to a relatively new economics field called Behavioral Economics (BE), one’s emotional state rather than reason influences their economic decisions. Vernon Smith, the BE economist who won a Nobel in economics, wrote:

People like to believe that good decision making is a consequence of the use of reason, and that any influence that the emotions might have is antithetical to good decisions. What is not appreciated by Mises and others who similarly rely on the primacy of reason in the theory of choice is the constructive role that the emotions play in human action.

Whether individuals are generally patient or impatient determines whether or not they are inclined to spend or save today, according to BE. If they are more patient, then they disposed to save more.

Furthermore, an

2023-10-21

Much of modern neoclassical economic theory depends upon assumptions that do not reflect real world conditions. Austrian economists, however, know that realistic assumptions matter.

Original Article: Economics and the Real World

2023-10-19

According to popular thinking, the definition of money is flexible. Sometimes the money supply could be M1 (currency and demand deposits); at other times it could be M2 (all of M1, plus savings deposits, time deposits, and money market funds) or some other M. According to popular thinking, what determines whether M1, M2, or some other M is considered the money supply is whether it is well correlated with key economic data such as the gross domestic product (GDP).

However, since the early 1980s, correlations between various definitions of money and the GDP have broken down. The reason for this breakdown, I have suggested, is the financial deregulation that made the demand for money unstable. Consequently, the usefulness of money supply as a predictor of economic activity has significantly

2023-10-18

Keynesians claim that the source of economic growth is consumer spending. Austrians know that net savings are the key to a growing economy.

Original Article: Real Economic Growth Depends on Savings

2023-10-12

While central banks use administered interest rates in hopes of emulating the natural rate, these efforts are always going to fail. Without free markets, there is no natural rate.

Original Article: The Central Bank Policy Interest Rate vs the Natural Rate

Read More »2023-10-11

In the market economy, wealth generators do not produce everything for their own consumption. Part of their production is used in exchange for the produce of other producers. Hence, in the market economy, production precedes consumption.

This means that something is exchanged for something else. This also means that an increase in the production of goods and services sets in motion an increase in the demand for goods and services.

According to David Ricardo,

No man produces, but with a view to consume or sell, and he never sells, but with an intention to purchase some other commodity, which may be immediately useful to him, or which may contribute to future production. By producing, then, he necessarily becomes either the consumer of his own goods, or the purchaser and consumer of the

2023-10-09

In the wake of bad news on inflation, the Federal Reserve is pushing up interest rates. However, a Fed-induced higher rate is not the same as an interest rate decided by the market.

Original Article: Why the Fed’s Tight Rate Stance Damages the Economy

Read More »2023-09-27

The US consumer sentiment index, compiled by the University of Michigan, fell to 69.5 in August from 71.6 in July. A weakening consumer sentiment index is seen as indicating a potential downturn in consumer spending and the economy in general.

Most economic commentators agree that individual consumption rather than saving is the key to economic prosperity. Saving, they believe, hinders economic growth because it coincides with weakening demand for goods. In this theory, economic activity is depicted as a circular flow of money in which one individual’s spending is part of the earnings of another.

If, however, individuals become less confident about the future, they are likely to cut back on their outlays and hoard more money, thereby diminishing the earnings of some other individual, who

2023-09-26

Economists and political elites fondly claim that economic growth is due to increased technological knowledge. That is only partly true.