Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Equity markets are seeing this week's gains trimmed after the S&P 500 fell 0.5% yesterday, recording its biggest loss in two weeks. Disappointing earnings in some tech leaders spurred profit-taking, The US 10-year Treasuries are consolidating the week's nine basis point increase in yields after nearing 1.90% yesterday. Asian bonds yields tracked US Treasury yields higher while European bonds are narrowly mixed as they consolidate yesterday's increase.

The US dollar recovered from early weakness yesterday and is mostly trading narrowly mixed today. The yen's weakness is the main development in the foreign exchange market. After a quiet start to the Tokyo session, the dollar rallied in Japan's afternoon amid reports that the BOJ may compliment its negative deposit rates with negative lending rates as early as next week's meeting. The dollar reached JPY110.75, its best level since April 5.

In the futures markets, speculators had amassed a record gross and net long yen position. The yen's momentum had stalled, with the dollar testing the JPY107.75 area three times. The interest rate differential makes it expensive to hold a long yen position with it trending higher. Without momentum, the late yen longs were in weak hands.

What we suspect is mostly short-covering lifted the greenback above its 20-day moving average against the yen for the first time this month. It is found near JPY110.10 now. The intra-day technical indicators warn that some backing and filling is likely in the North American session. The JPY110 area may offer support. We anticipate better dollar dip buying than we have seen over the last few weeks.

We have noted that the US 10-year premium over Japan had been widening, and this often gives the dollar some traction. The spread has widened from about 174 bp on April 5 to almost 200 bp yesterday. The Nikkei gained 1.2% to new four-month highs while the MSCI Asia-Pacific Index slipped 0.4% trimming this week's gains to 1%. Japanese banks led the market, rising almost 5% ostensibly on the prospect of being paid to take funds from the central bank.

Under former BOJ Governor Shirakawa, a lending facility was introduced that provided no interest rate loans to banks in late-2012. Banks have borrowed JPY24.4 trillion (~$223 bln) from the facility. The prospect of borrowing at negative rates helped offset the idea that the BOJ may cut deposit rates further next week. A Bloomberg survey found 23 of 41 respondents expect the BOJ to take fresh action. Nearly half of those survey (46%) expect the BOJ to buy more ETFs. Almost 20% expect the BOJ to buy more bonds, and the same percentage expect a cut in rate, according to a survey that was conducted.

The Japanese economy continues to struggle to sustain positive growth momentum. Earlier today, the preliminary April manufacturing PMI slumped to a new record low of 48.0 from 49.1. The median forecast was for a small increase. The tertiary index for February fell 0.1% while the January series was halved from 1.5% to 0.7%. Next week Japan is expected to report weak household spending, a negative CPI print, and a fall in housing starts. The labor market remains firm, and industrial output may recover around half of February's 5.2% decline.

The eurozone reported the flash PMI. Manufacturing slipped marginally to 51.5 from 51.6. The median expected a rise to 51.9. Services ticked up to 53.2 from 53.1. The median expected a slightly smaller increase. The composite reading stands at 53.0 from 53.1, which points to broadly steady growth at the start of Q2.

Germany's composite reading fell to 53.8, its lowest reading since last July, from 55.0 in March. This was driven by the pullback in services to 54.6 from 55.1. Manufacturing rose to 51.9 from 50.7 and is the second monthly increase. The German details may be more encouraging than the headline, with output, employment, and new orders increasing.

France's manufacturing sector remains under pressure. The April PMI fell to 48.3 from 49.9. It matches last August's lows. The sector reported the largest drop in new orders since February 2015. The service sector performed better, rising to 50.8 from 49.9. It is the highest since last November. The composite rose to 50.5 from 50.0 and is above the 49.8 average from Q1.

The euro reversed yesterday. After nearing $1.14, it was sold down to $1.1275 before closing the North American session a little below $1.1290. The losses have been marginally extended today. Key technical support is seen in the $1.1220-$1.1235 area. Initial resistance is pegged around $1.13. The dollar's recovery is being aided by a 10 bp widening in the US two-year premium over Germany since April 7, and at nearly 130 bp it is the largest premium since late-March.

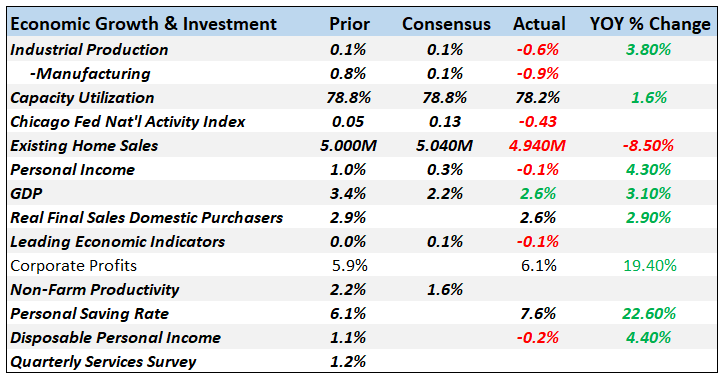

The April Philadelphia Fed outlook disappointed by falling back into negative territory. However, news that weekly initial jobless claims fell to a new cyclical low of 247k was understood as more important. The weekly jobless claims are now at a level not seen since 1973. The latest results coincide with the survey for the national figures due out in early May. Weekly jobless claims have fallen for three consecutive weeks. Continuing claims fell to 2.14 mln, which is the lowest since November 2000.

Given the significance of household consumption to the US economy, strength in the labor market is key and overshadows other lingering pockets of weakness. The performance of the labor market also underpins expectations that the economy will recover from the soft patch hit in Q4 15 and Q1 16. Separately, the St. Louis Fed’s measure of financial stress is at its lowest level since last December.

Although three-quarters of economist in a Wall Street Journal survey from earlier this month expected the FOMC to hike rates in June, the June Fed funds futures contract has almost a 20% chance of a 25 bp rise discounted. One of the reasons that Fed officials have been particularly cautious is due to global considerations. The global situation continues to improve.

Volatility has subsided. Emerging markets have stabilized, and many equity markets and currencies have staged impressive recoveries. While the Chinese economy appears to be gaining some traction (though seemingly purchases with more debt), and the yuan has a firmer tone, poor equity market performance has had little contagion.

A trade-weighted measure of the US dollar has fallen about 7.5% since the end of January. These considerations suggest a less dovish FOMC statement next week. In this context, being data dependent may mean that provided that economic entrails confirm the US economy is strengthening again. The market appears to be under-pricing the risk of a June rate hike.

Canada reports February retail sales and March CPI today. The risk seems to be on the downside for retail sales where the median forecast is for a 08% decline after a 2.1% surge in January. Consumer prices are expected to have moderated, with the headline slipping to 1.2% from 1.4% and the core rate easing to 1.7% from 1.9%. Both reports are likely to be taken in stride by policymakers and investors.

The US dollar recorded a multi-month low just below CAD1.26 at midweek. It has edged higher, reaching CAD1.2760 earlier today. Its performance in North America may be more dependent on the greenback’s overall tone than the Canadian data per se. Initial resistance is seen near CAD1.2800, with support around CAD1.2680.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: Canadian Dollar,Japanese yen,newslettersent,U.S. Housing Starts,U.S. Initial Jobless Claims