George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Pictet calls for negative interest rates in Switzerland in order to maintain rate differentials between the euro zone and Switzerland. Maintaining rate differentials would be useful for FX speculators and for money market funds that still invest in the euro zone.

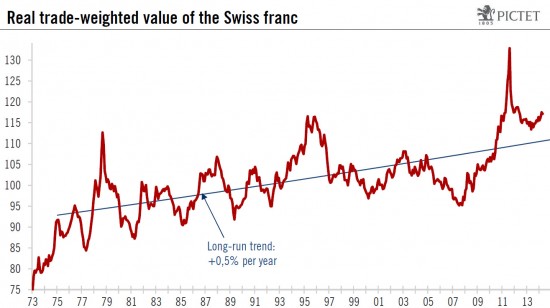

According to newest SNB data, the real effective exchange rate for the Swiss franc has recently risen again and is at 112.5, when it is compared to 100 in 1999. The last part of the sentence is actually quite important, because in 1999 the Swiss franc was in an undervalued phase – see Pictet’s long-term graph below and our “Is CHF overvalued?“.

The ECB could move into negative deposit rates. Pictet calls for negative interest rates in Switzerland in order to maintain rate differentials between the euro zone and Switzerland. This difference could be useful for “risk-driven” FX speculators against CHF and for “yield-driven” money market funds that – despite near zero rates – still invest in the euro zone. Some FX pundits see the need for the SNB to go negative even before the ECB meeting.

The recent turn of CFTC traders position to long USD and short CHF has weakened the Swiss franc as much as the euro. But we explained here, that in times of zero interest rates, the longer-term CHF drivers are not FX speculators or bond/money market funds that bet on rate differentials. The long-term drivers are the huge Swiss current account surplus, consequently higher profits of Swiss companies in international comparison and the strong home-bias of Swiss investors due to weak international growth and returns compared to global risks. Negative rates, however, could be even counter-productive.

Global growth is currently driven more by the United States. Emerging markets (EM) are quite weak, after years of strong pay rises and higher wage costs. In addition to Fed “tapering fears”, EM central banks were forced to hike rates and made investments expensive. CHF is related more to EM, as “alternative currency” to the dollar and as safe proxy for global growth. See more in CHF Is No Safe-Haven, but a Safe Proxy for Global Economic Growth.

Due to US strength and EM weakness, we do not see any risks for the EUR/CHF floor, no matter the ECB does, and no need for negative Swiss rates or for FX interventions. On the other side, global and European growth is too weak for EUR/CHF to appreciate.

Hence the euro should remain mostly stable against CHF, no matter what the ECB decides.

One should also remember that in the past the euro often appreciated after rate cuts – against both CHF and USD -, investors were probably buying European stocks. With low peripheral bond yields, relatively high US inflation and the end of tapering, this seems to be different now.

Here Pictet’s paper (source):

PICTET& CIE: SWISS MONETARY POLICY: TOWARD NEGATIVE INTEREST RATES?

At its next monetary meeting, the ECB may well cut its deposit rate into negative territory. How will the SNB response?

We believe the Swiss National Bank will remain pragmatic and wait to see if the franc rises markedly against the euro – which is far from sure – before reacting. Then, the answer may be to follow suit and also push rates into negative territory, or the SNB may choose to start purchasing foreign currencies once again. Both responses are certainly possible, but we believe the second is more likely, at least in a first stage.

ECB likely to take fresh monetary stimulus measures

Over the past few days, it has become more and more likely that the ECB will take fresh monetary stimulus measures at its next policy meeting on 6 June. On this occasion, a decision to cut the deposit rate into negative territory seems quite possible. If that is the case, what would be the Swiss National Bank’s own policy response? Will the ECB’s action trigger a reaction from the SNB?

At the end of March, Thomas Jordan – SNB president – said the SNB would rule out no options to defend the floor on the euro-franc rate but wouldn’t “automatically react” to policy changes at the ECB.

An ECB rate cut will not necessarily push the franc higher

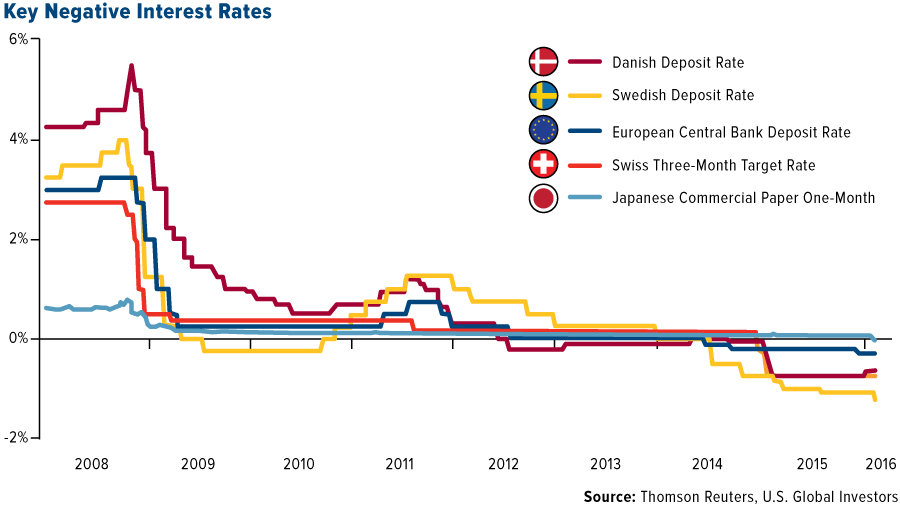

There is no doubt that the SNB will try to avoid upward pressures on the Swiss franc and that it will do its own “whatever it takes” for the 1.20 floor to hold. However, it is far from certain that the franc will register substantial upward pressure following an ECB rate cut. Swiss franc investors are often more risk-driven than yield-driven. And a more relaxed ECB monetary policy may well lead to improved eurozone economic prospects and a lift in risk appetite. Moreover, historically, when the euro is falling against the dollar, the Swiss franc is quite often falling by an even larger extent. And this is exactly what happened over the past few days. Anticipations of a significant ECB relaxation move on 6 June have built, but they were accompanied by a modest weakening of the franc against the euro, not a rise. It is therefore quite possible that when the ECB loosens its monetary stance, the Swiss franc won’t rise against the euro – or at least won’t rise by much.This is not to say that interest rates differentials don’t matter for the EUR/CHF exchange rate. The fact that the 3-month rate differential went down from some 140bp on average in Q4 2011 to barely 15bp by the summer of 2012 (see chart below) certainly contributed to generate upward pressure on the franc in H1 2012. However, an interest rate spread reduction of 125bp in a context of high fears of a euro implosion is not the same as a 10 or 20bp reduction in a less risky world. What will happen in Ukraine, China and to risk aversion in general is probably more important for the franc than a modest ECB rate cut, especially when this cut is probably already largely priced in.

What happened last year is also instructive. The ECB cut its main refinancing rate by 25bp twice, the first time at the beginning of May and the second time at the beginning of November. In both cases, the SNB didn’t followed suit and didn’t intervene in the exchange rate market. However, in both cases, the franc didn’t rise. It actually depreciated, particularly in May, when it fell from EUR/CHF 1.22 at the beginning of the month to 1.26 three weeks later.

FX interventions more likely than negative official rates.

Nevertheless, it is still possible that following ECB rate cuts, the euro starts falling against the Swiss franc. If that is the case, what will the SNB do?

Basically, there are two main possible reactions:

(1) The SNB may follow suit (most probably at its scheduled quarterly meeting on 19 June), and assign a negative interest rate to bank sight deposits.

(2) The SNB could choose once again to proceed with interventions in the exchange rate market to defend the floor.This second choice doesn’t necessarily exclude the implementation of negative interest rates at a later stage, if interventions have to become too massive. We believe this second option is the most likely. Although the SNB stressed on different occasions that negative interest rates are among steps the central bank could take, it seems actually to be quite reluctant to use that tool. It is not all clear exactly why, but the main reasons are probably the following.

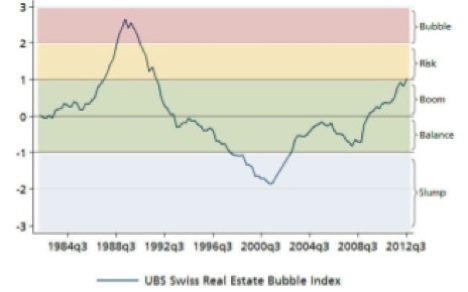

First, the SNB still considers that “developments on the Swiss mortgage and real estate markets represent a risk for financial stability”. In this context, lowering interest rates further is probably a move the central bank would like to avoid.

Second, negative interest rates could impair the functioning of financial markets and make life more difficult for money market funds and pension funds. Third, with negative rates, there are some risks of a flight to cash. This is particularly true for Switzerland where high denomination banknotes exist. Demand for 1,000-franc banknotes has already increased quite significantly over the past few years. The introduction of negative interest rates on bank sight deposits at the SNB is far from excluded, but we believe the SNB would prefer to avoid it. It is worth remembering that in H1 2012 when the ECB was cutting rates and the SNB had to massively purchase foreign currencies to protect the floor, Swiss monetary authorities refrained from pushing official rates below zero.

In any case, negative interest rates are not a panacea to protect the 1.20 floor. In Switzerland, some interest rates are already in negative territory, notably the call money rate and the 3-month rate on Confederation bills (see chart below). In June 2012, at the high of the phase of upward pressures on the franc, money inflow pushed down interest rates on 3-month Confederation bills as far as -0.8% (see chart below). And it didn’t help much…

Another point is worth mentioning. As some of our readers probably also have heard, some pundits were speculating that the SNB might lift the floor to 1.25 franc in response to an ECB stimulus move. We were very surprised to hear that kind of prediction. So far this year, while the trade-weighted Swiss franc was rising together with its European counterpart and the euro was relatively stable around 1.22 franc, the SNB didn’t lift the floor. Why would they do that when the euro may at last start moving down and when the franc may once again be confronted with upward risks? In short, we consider this scenario as extremely unlikely.

EUR/CHF: no changes in our scenario

The ECB may well soon push rates into negative territory, but it does not imply changes in our scenario for the EUR/CHF exchange rate. Whatever the ECB does, the SNB won’t abandon the 1.20 ceiling. And unless ECB measures are drastic, which seems unlikely, the most likely scenario in our view is that the Swiss franc will continue to hover around its current level, before weakening towards EUR/CHF 1.25 on a one-year horizon.

As we have mentioned above, if the ECB sets a negative interest rate and the SNB does not follow suit, it might trigger upward pressures on the Swiss franc. If these upward pressures become too important, the SNB will intervene as much as necessary, as it has done before. If the SNB follows suit, interest rate differentials will likely remain unchanged, whilst ECB monetary stimulation will improve eurozone growth prospects and probably stimulate risk appetite. In such a context, the risk-averse Swiss currency might experience downside pressures. This will be welcomed by the SNB. If this scenario materialises, the one-year target of EUR/CHF 1.25 will be reached sooner than expected.

Tags: money-market funds,Swiss Franc Overvaluation