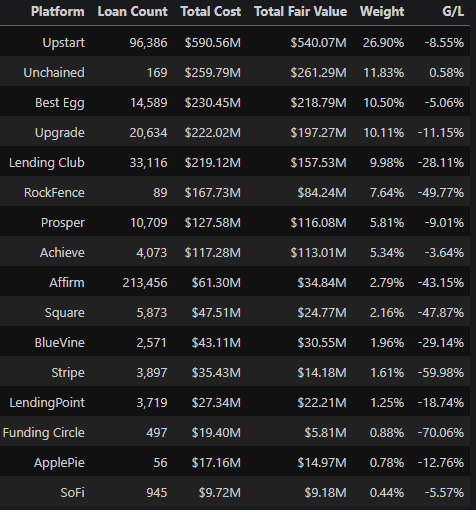

The Stone Ridge Alternative Lending Risk Premium Fund (LENDX) is the latest to face liquidity pressure amid growing concerns about private credit. As an interval fund, LENDX’s shares aren’t publicly traded, so investors who want out must tender their shares for repurchase by the fund quarterly. Last Thursday, the $2.4 billion fund told clients that redemption requests for the quarter were so high that LENDX would repurchase only 11% of the tendered shares. Given that interval funds are required to offer to repurchase at least 5% of outstanding shares quarterly, we can deduce that investors tendered at least 45% of the fund’s shares for redemption.

The panic signals that investors’ worries about private credit are growing. The story so far has focused on loans to software companies and other sectors threatened by AI progress. However, LENDX purchases consumer and small-business loans from fintech lenders. Examples include buy-now-pay-later debt from Affirm and personal loans from Upstart and LendingClub.

So why are investors suddenly rushing to withdraw from funds holding consumer and small-business loans? The table below summarizes the Schedule of Investments released by LENDX on January 29th, two weeks before the latest redemption window opened. The data show that the fund is being forced to write down the value of its loan assets. Overall, the fund’s loan portfolio has been written down by 15%.

What To Watch Today

Earnings

- No earnings releases today

Economy

Market Trading Update

The S&P 500 closed Friday at 6,506.48, down 1.5% on the session and now 7.1% below January’s all-time high of 7,002. This marks the fourth consecutive weekly loss and the lowest close since mid-September 2025. The Russell 2000 slipped into official correction territory, and the Dow and Nasdaq sit on the doorstep. The week was defined by a classic bull trap. A Monday/Tuesday reflex rally, fueled by Nvidia’s GTC conference and a brief retreat in oil below $100, sucked in late buyers before Wednesday’s Fed meeting violently reversed the tape. Friday’s selling accelerated after Iraq declared force majeure on all foreign-operated oil fields, confirming the Hormuz disruption is broadening.

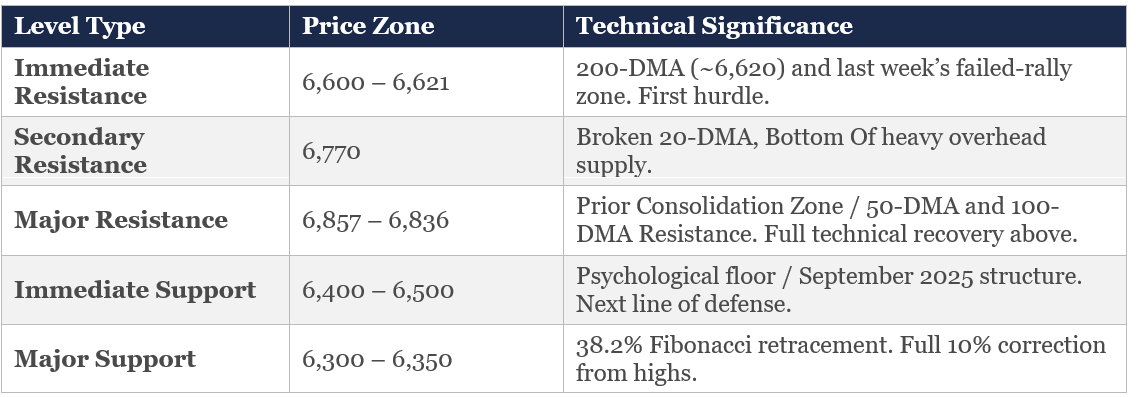

The index is now firmly below its 200-DMA (~6,620), which was decisively broken last Thursday and has failed every subsequent attempt to reclaim it. As we discussed last week, breaking the 200-DMA ended a 214-session streak above that trendline. The historical data on such breaks, however, should temper the panic: over the past decade, the S&P 500 was higher 87% of the time six months later (avg. +9%) and 85% of the time twelve months later (avg. +14%). But the path matters. The average maximum drawdown across those episodes was roughly −16.5%—meaning from current levels, a full washout could take us into the 5,800–6,000 range before a durable bottom forms. We aren’t forecasting that, but it’s the risk you need to size for.

The fundamental overlay worsened this week. The Fed’s “hawkish hold” at 3.5–3.75% came with upwardly revised inflation forecasts and lower growth projections, the textbook stagflation signal we flagged two weeks ago. Macquarie now expects the Fed’s next move to be a hike, not a cut, pushed to 1H27. However, oil remains the transmission mechanism: Brent closed above $108, and the Iraq force majeure escalation on Friday threatens to widen the supply disruption. Selling has broadened beyond mega-cap tech, and Friday saw 21 S&P 500 stocks hit 52-week lows, including Home Depot, Domino’s, and McCormick, a sign the damage is spreading into consumer names.

Bottom line: The failed mid-week rally was the “buyer’s remorse” moment that confirms this tape has changed character. History says we’re more likely higher in 12 months than lower, but the next durable bottom requires either a sustained decline in oil or a credible de-escalation in the Middle East. Neither is imminent. HSBC notes markets are “pricing a recessionary outcome” and sees dislocations worth watching. I agree, this is a shopping list market, not a buy-everything market. Accumulate quality at pre-defined levels (6,400, then 6,300), keep cash reserves, and treat every bounce as suspect until the VIX sustains below 20 and oil finds a ceiling. Defense over offense.

Trade accordingly.

The Week Ahead

It will be a quiet week with the FOMC meeting out of the way and little noteworthy economic data. Tomorrow, the S&P Global PMI flash report for March will offer a preliminary look at activity in both the manufacturing and services sectors of the economy. The services PMI, shown below, remains in a consistent downward trend that began late last summer. While it remains safely in expansionary territory, a continuation of the trend lower would be concerning.

This week will host several Fed speakers, as their blackout period is over. Appearances will include the Fed’s Daly, Miran, Cook, Barr, and Jefferson.

The Dollar’s Plumbing: Conspiracy Vs. Data

Every few months, a headline appears declaring that the U.S. dollar’s reign as the world’s reserve currency is over. China is dumping Treasuries. Central banks are hoarding gold. The BRICS are building a new monetary order. The sanctions that froze $300 billion of Russia’s reserves in 2022 proved, the argument goes, that dollar-denominated assets are no longer safe. The “risk-free” asset has become a weapon.

The data tells a more nuanced, and arguably more important, story. One that investors ignore in favor of the simpler narrative is the risk of getting it badly wrong.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post The LENDX Liquidity Trap appeared first on RIA.

Full story here Are you the author?You Might Also Like

2026-02-20

Money – everybody wants it, but few actually have it. As shown in recent financial statistics, the “wealth gap” in America continues to grow between the “haves” and the “have-nots.” That gap has led to a bombardment of narratives explaining why younger generations are financially oppressed. As shown, the top 10% of income earners own …

Software Or Staples?

Software Or Staples?

2026-02-09

As we wrote in yesterday’s Commentary, efficiently rotating between overbought and oversold sectors, factors, or stocks is a well-established method for outperforming markets. Like any strategy, the hard part is timing, or properly estimating when a pair of sectors, factors, or stocks is about to reverse their respective trends. Currently, there is a massive divergence …

Minerals, Russia, China & Iran: More On Venezuela

Minerals, Russia, China & Iran: More On Venezuela

2026-01-07

Yesterday’s Commentary discussed the potential impact of regime change in Venezuela on the energy sector. Today, we extend the analysis and examine other reasons for the invasion. The following theories are based on a Substack commentary from Tracy Shucart, an economist and resources trader. For starters, Tracy makes it clear that oil is not the …

Tags: Featured,newsletter