The heatmap below, courtesy of FinViz, shows the one-month performance of the S&P 500 financial sector stocks. As shown, Berkshire Hathaway and the insurance companies are higher over the period, while the large majority of the remaining financial sector stocks struggle. For context, the S&P 500 was down 2.80% over the same period. There appear to be three primary factors driving weakness in financial sector stocks:

Yield Curve: Via deposits and CDs, banks tend to borrow for shorter periods of time than the longer-term loans they make. Accordingly, the shape of the yield curve impacts net interest margins. Recently, the yield curve has flattened by about 25 bps, thereby shrinking net interest margins.

Credit Concerns: Monday's Commentary noted that the private credit loan market is coming under increased pressure due to loan losses and possible fraud. Banks and brokers (GS/MS) are major players in this asset class. Thus, the concerns roiling the private credit market are spreading to the banks and brokers. Compounding the issue for the financial sector, banks are seeing rising consumer delinquencies.

Credit Card Competition: Payment giants Visa and Mastercard, which were long considered to have strong moats, are facing competition from cheaper payment alternatives. Real-time payment systems, account-to-account transfers, and fintech platforms are increasingly bypassing traditional card networks and their significant interchange fees. Investors are starting to question whether their long-standing pricing power can persist.

Combined with margin pressure, emerging credit concerns, and evolving payment competition, the financial sector lacks a clear catalyst for sustained outperformance.

What To Watch Today

Earnings

Economy

- No notable economic reports

Market Trading Update

Yesterday, we touched on the market's technical backdrop with the index working to hold onto support at the 100-day moving average. I wanted to shift focus today to the situation in Iraq and the numerous claims on the internet about its initial impact. Here was my favorite:

That obviously did not happen, and these types of individuals who post exaggerated nonsense do not provide any helpful context for investors. In reality, the market opened down just 1% yesterday morning before immediately finding buyers. Such has always been the case. This was the subject we touched on two weeks ago in the #BullBearReport:

"The crucial takeaway for investors is that uncertainty creates short-term market volatility. However, a fundamental distinction exists between events that produce short-term market fluctuations and those that modify economic expansion patterns or corporate earnings. Most geopolitical events in most historical situations fall into the first category. The market responds with immediate price movements, but the effects disappear quickly unless the event damages consumer demand, capital expenditures, or earnings potential.

The current situation between the US and Iran likely falls into the first category. That isn’t just speculation. It’s data. The market’s behavior during military conflicts since World War II, including the Cuban Missile Crisis, the first Gulf War, and the Russian invasion of Ukraine, demonstrates a recurring pattern of sharp equity market declines followed by quick recoveries, sometimes within weeks. The market responds to news events by overreacting until investors gain clarity, leading to a market correction."

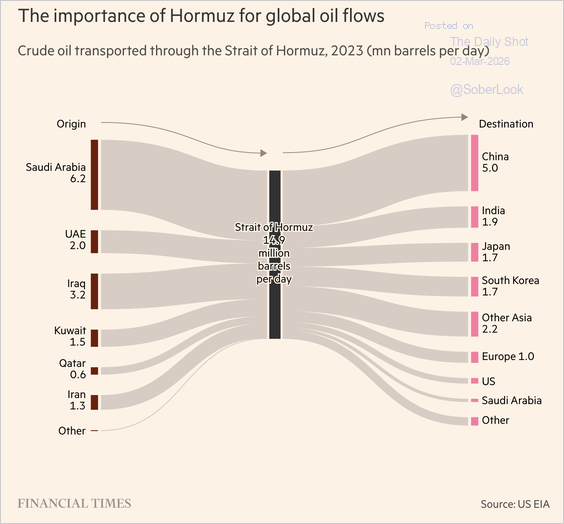

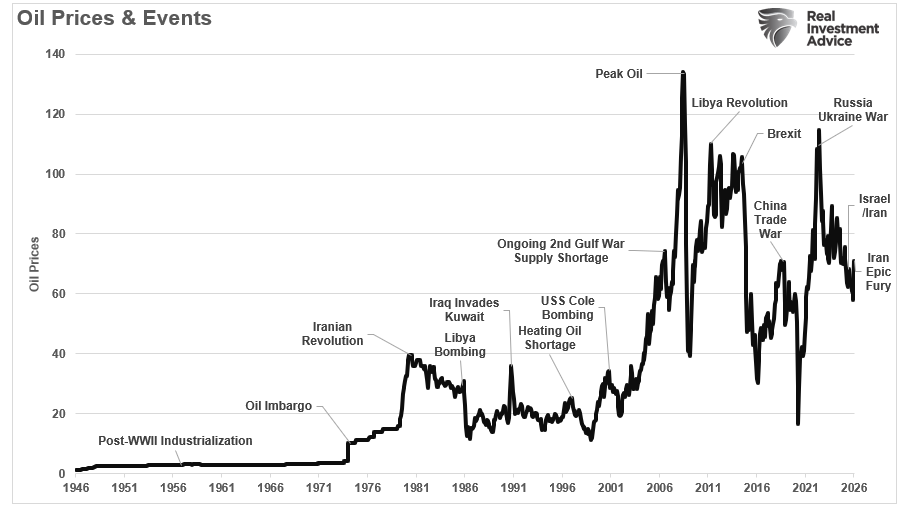

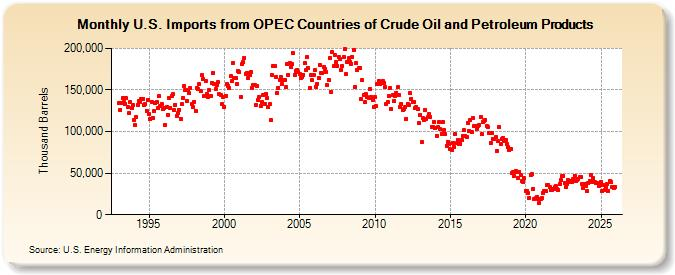

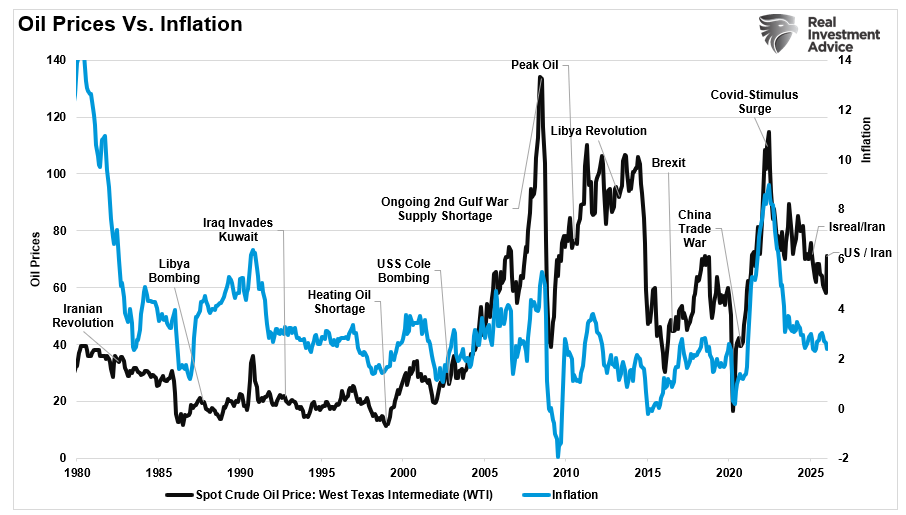

The one area with an immediate impact is oil prices, which initially surged nearly 8% at the open yesterday. However, the claims that oil will go to $150/barrel or more are also as misguided as the market 20% in a single day. While there were many comparisons to the 1970s oil embargo, today's situation is vastly different. The US is now an oil exporter and, by all measures, the largest producer of petroleum on the planet. Secondly, the amount of oil that comes to the US through the Strait of Hormuz is very small.

Secondly, military operations tend to be very short. As such, the price shock of such events on oil, likewise, tends to be shorter-term in nature. The chart below shows oil prices with relevant events.

You will notice that since Russia invaded Ukraine, oil prices have been lower and less volatile. This is because the US is much less dependent on foreign oil imports for its economy. That reduced dependence lowers the "conflict risk" that would have previously been factored into oil prices.

Nonetheless, there is a risk of higher oil prices for the US stock and bond markets. If oil prices do shift higher on a sustained basis, it will translate into higher near-term inflation rates. However, even substantially higher oil prices, as seen after the financial crisis, did not translate into surging inflation but into modestly higher inflation rates. That should likely be expected, which could temporarily weigh on stock and bond prices.

The bottom line is that the military operation against Iran certainly induces volatility risk in the markets. As such, investors should consider reducing portfolio risk, taking profits, and raising cash levels slightly to get a better grasp of potential outcomes.

Most importantly, I would avoid the "doom" crowd and dismiss the more outrageous headlines, as those outcomes never materialize because the market is looking forward, not backward.

Remain patient and prudent, and let the market dictate our next moves.

Financials Are Fading

Adding to the opening section, the financial sector was the worst-performing over the last five days, as shown courtesy of SimpleVisor below. The first graphic shows it has underperformed the S&P 500 by 3.00% over the last five days and an additional 2.84% over the 20 days prior. The second graphic shows that XLF has been churning in the lower-left quadrant, meaning its absolute technical score and relative (vs. the S&P 500) have remained in oversold territory. As we led, there are three primary factors weighing on the financial sector, and no immediate fundamental catalyst on the horizon to improve the situation.

SaaS: Is There Opportunity In The Destruction?

A specter is haunting Wall Street—the specter of the “SaaSpocalypse.” Since the iShares Expanded Tech-Software Sector ETF (IGV) peaked on September 19, 2025, it has fallen roughly 30%. For context, the broad technology indexes like XLK and QQQ are essentially flat over the same period, and the semiconductor ETF (SMH) is up 30%. Between mid-January and mid-February 2026 alone, approximately one trillion dollars was wiped from the collective value of software stocks, with the S&P North American Software Index posting its worst monthly decline since the 2008 financial crisis.

The catalyst was a series of AI product launches, most notably Anthropic’s Claude Cowork tool and OpenAI’s enterprise agent, Frontier, demonstrating that AI agents can now handle complex knowledge work autonomously. The market’s interpretation was simple. If AI agents can replicate what enterprise software does, then enterprise software is finished. That is the narrative that has taken hold in recent weeks. The consequence has been brutal. Workday is down 35% year-to-date. Adobe has shed 26%. Salesforce, 25%. Atlassian plunged 35% in a single week. Even Microsoft, the ultimate blue chip, fell by more than 10%.

The thesis is straightforward enough. Generative AI can now write code, automate workflows, and rapidly and cheaply create customized applications. Therefore, if enterprises can build their own “disposable software,” micro-apps tailored to specific workflows, instead of paying bloated subscription fees, then the traditional per-seat SaaS pricing model is dead. Potentially worse is that AI lowers barriers to entry, enabling more competitors to quickly replicate existing software. Such would compress margins and weaken the moats that once protected large software firms.

It is a compelling narrative. The question investors must answer is whether it is true. READ MORE...

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post The Financial Sector Is Under Pressure appeared first on RIA.

Full story here Are you the author?You Might Also Like

The Passive Aggressive Market: Bogle’s Warning Came True

The Passive Aggressive Market: Bogle’s Warning Came True

2026-03-04

Since the pandemic, the line between passive investing and aggressive speculation has blurred. The current bout of speculative fervor extends beyond financial markets. For instance, we see the same impulse in the explosion of sports betting and the surge in event-betting sites like Kalshi and Polymarket. In the investment arena, margin debt is at record …

Our Take On Tariffs

Our Take On Tariffs

2026-02-24

To address the many emails we received, we present our take on the Supreme Court’s tariff ruling. First, President Trump has multiple ways he can implement trade restrictions beyond what the Supreme Court ruled against. In fact, he implemented a 150-day 15% global tariff after the court’s ruling. As we share below, the effective tariff …

The Silver Surge: Micro Bubble Or Reasonable Valuation?

The Silver Surge: Micro Bubble Or Reasonable Valuation?

2026-01-14

Silver has been on a tear, rising fourfold in the last few years. The price is driven by the narrative of dollar debasement. Furthermore, there are indications that limited supply, along with growing industrial demand for silver, warrants higher prices. As we have stated in recent articles (Debasement, What It Is And Isn’t & Dollar …

Fed Challenges: Bill Dudley’s Take On 2026

Fed Challenges: Bill Dudley’s Take On 2026

2026-01-08

Bill Dudley, a respected economist and President of the New York Fed during the Financial Crisis, penned a Bloomberg editorial outlining six challenges facing the Fed in 2026. Given his deep background in economics and intimate knowledge of the Fed, it’s worth providing a brief summary of his views. Independence is at the top of …

YTD Returns Highlight a Narrow Market

YTD Returns Highlight a Narrow Market

2025-12-31

YTD returns across major U.S. asset classes continue to reflect a highly concentrated market. The Finviz chart below does a nice job illustrating YTD returns across a wide array of futures contracts. Large-caps dominate YTD equity returns, while small- and mid-cap stocks lag amid tighter financial conditions and slower earnings growth. Outside of equities, YTD …

Tags: Featured,newsletter